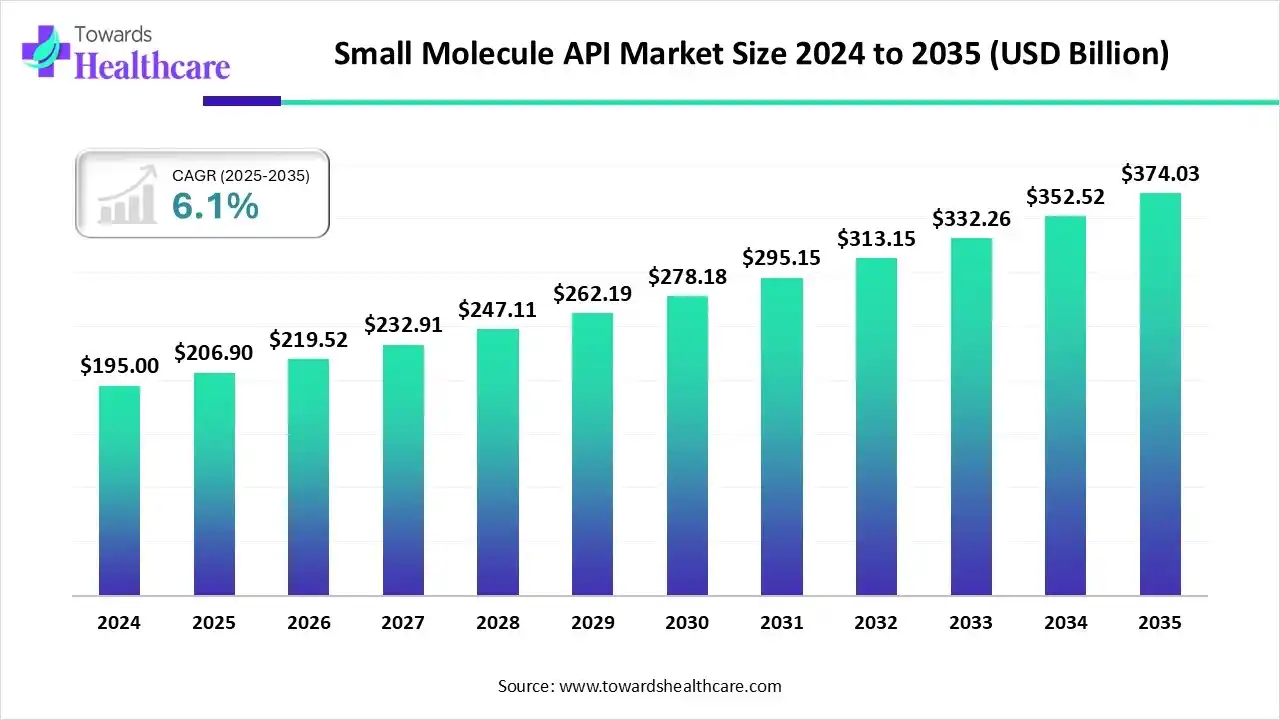

The global small-molecule API market was valued at US$206.9 billion in 2025, grew to US$219.52 billion in 2026, and is projected to reach US$374.03 billion by 2035, a steady expansion driven by a 6.1% CAGR (2026–2035) across innovator, generic, HPAPI and specialty small-molecule segments.

Download Free Sample of Small Molecule API Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/6439

Small Molecule API Market Size

Base and near-term scale (2025–2026)

• 2025 reported market size: US$206.9B.

• 2026 actual/recorded value: US$219.52B — an absolute increase of US$12.62B year-over-year indicating continued near-term demand momentum.

Long-term projection (2035 target)

• Forecast for 2035: ≈US$374.03B, reflecting structural growth in chronic-disease therapies, oncology small molecules, and expanded global manufacturing capacity.

Compound annual growth

• CAGR 2026–2035 = 6.1% — implies the market roughly doubles over ~11 years (consistent with the 2026→2035 projection).

Revenue concentration and leadership

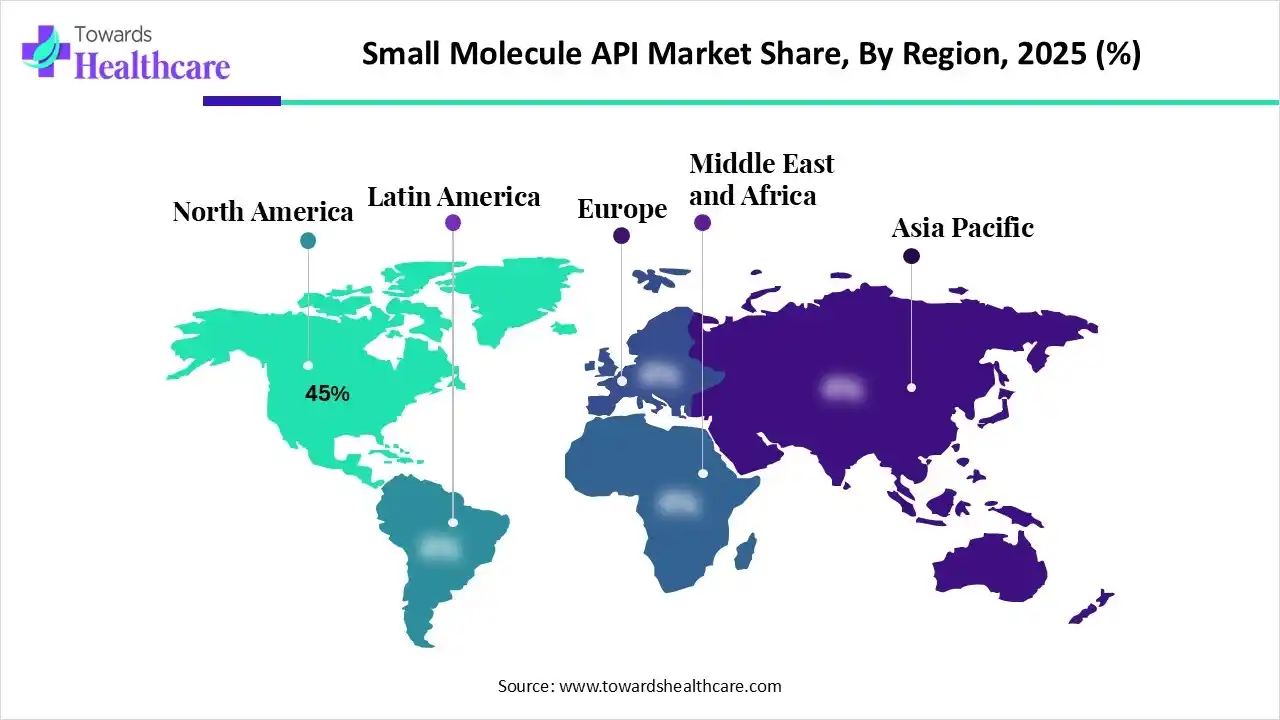

• North America accounted for ~45% of market revenue in 2024 (hence a dominant revenue base into 2025–2026).

Segment revenue drivers (size drivers rather than application breakdown)

• Branded/innovator APIs contributed a majority share (~55% in 2024) — this elevates average ASPs and margins across the market.

• Small-molecule organic APIs dominated volume/value (~82% in 2024), anchoring the market’s bulk revenue.

Growth pockets with outsized impact on size

• Oncology small molecules (32% of 2024 revenue) and generics expansion (fastest growth among product types) together push volume and addressable market size.

Geographic growth skew

• Asia-Pacific expected fastest regional CAGR — a material contributor to the 2035 projection via capacity expansions and cost-competitive production.

Role of CDMOs and contract manufacturing on scale

• Expanding CDMO capacity and reshoring investments (by large pharmas) increase regional production throughput — directly increasing market monetized volumes.

High-value subsegments lift average revenue per unit

• HPAPIs, sterile small-molecule injectables, and peptidomimetics add higher ASPs and regulatory complexity — increasing market value beyond mere volume growth.

Policy & investment effects on size

• National programs (e.g., India PLI for KSMs/DI/API) and country-level incentives accelerate local production capacity and therefore contribute to market size expansion.

Market Trends

Shifting sourcing strategies (insourcing + CDMO mix)

• Large pharma invests in internal capacity to reduce supply risk, while simultaneously outsourcing specialized or overflow work to CDMOs — creating a two-tier manufacturing demand.

Oncology focus and targeted small molecules

• Oncology led with ~32% revenue (2024) — trend: continued R&D and approvals for small-molecule inhibitors raise long-term demand.

Generic/merchant API ramp

• Generic/merchant APIs identified as fastest-growing product type — price competition drives volume and market share gains for low-cost producers.

Rapid growth of HPAPIs & cytotoxics

• High demand and specialized containment needs propel facility investments and higher per-kg revenue.

Regional capacity buildout (APAC, Brazil, GCC, MEA)

• APAC fastest growing; Brazil, GCC, and MEA push to localize manufacturing — diversifying global supply.

Technology adoption (continuous manufacturing, flow chemistry)

• Advanced synth and continuous processing raise yields, reduce cost per kg, and shorten lead times — improving competitiveness.

Regulatory & legislative accelerants

• Examples like Germany’s Medical Research Act (Oct 30, 2024) speed clinical development and can accelerate API demand tied to local trials.

Sustainability and green chemistry

• Increasing emphasis on greener synthetic routes to reduce waste, regulatory risk, and long-term costs.

Vertical integration & M&A

• Larger companies and CDMOs consolidate capacities and capabilities to offer end-to-end services from process R&D → commercial supply.

Digitalization & AI in process optimization

• AI and model-based platforms (e.g., Lonza’s Design2Optimize) accelerate scale-up and reduce time-to-clinic/commercial — see AI section below for deep impacts.

10 ways AI impacts / roles in the small-molecule API market

Route-and-process design optimization

• AI predicts optimal synthetic routes and reaction conditions (solvent, catalyst, temperature), reducing the number of lab experiments and accelerating process R&D timelines.

Model-based scale-up & manufacturability scoring

• Machine models evaluate candidate molecules for manufacturability and scale-up risk, enabling early go/no-go decisions and guiding investments before expensive pilot runs.

Predictive yield and impurity profiling

• AI tools forecast expected yields and impurity profiles for alternate routes, prioritizing pathways that minimize costly purification steps and regulatory burden.

Process control and real-time optimization

• Integration of AI with PAT (process analytical technologies) enables closed-loop control for real-time adjustments (e.g., feed rates, residence time), improving consistency in continuous manufacturing.

Analytical method development and QC acceleration

• AI speeds up method development for HPLC/LC-MS and helps automate peak deconvolution and impurity identification, shortening release times and testing bottlenecks.

Predictive maintenance and capacity utilization

• Machine learning forecasts equipment failures and optimizes maintenance windows, increasing effective throughput for cGMP plants and reducing unplanned downtime.

Regulatory dossier and CMC generation support

• AI assists in collating chemistry, manufacturing and control (CMC) documentation, auto-suggesting standard text/analyses and flagging gaps — reducing time to file.

Supply-chain risk forecasting

• AI models combine supplier, geo-political and logistics data to produce risk scores, enabling dynamic sourcing strategies (e.g., pivot to nearer suppliers, build buffer stocks).

Green-chemistry route discovery

• Generative models propose synthetic pathways that reduce hazardous reagents, solvent volumes, and waste streams — supporting sustainability goals and regulatory acceptability.

Drug candidate prioritization tied to manufacturing economics

• Integrated AI scoring frameworks combine pharmacology and manufacturability (cost per kg, time to clinic) so decision-makers prioritize candidates that balance efficacy with realistic production economics.

Regional insights

North America (dominant; 45% revenue in 2024)

• Market character: High ASPs, strong R&D pipeline, rapid adoption of advanced manufacturing (continuous, HPAPI containment).

• Drivers: Large biotech/pharma R&D spend, regulatory sophistication, clinical trial density.

• Implication: Demand for high-quality, complex APIs and CDMO partnership models — makes NA a profitable, innovation-led market.

Asia-Pacific (fastest-growing region)

• Market character: Rapid capacity additions, cost competitiveness, growing regulatory maturation.

• Drivers: Investments in pharma manufacturing, government schemes (e.g., India’s PLI), strong generic manufacturing base.

• Implication: APAC will drive volume growth and take increasing share in generic and intermediate supply chains.

Europe (established, quality-driven)

• Market character: Strong regulatory standards, advanced manufacturing, emphasis on sustainability and process innovation.

• Drivers: Policy support for R&D (e.g., Germany’s Medical Research Act), existing industrial base.

• Implication: Europe remains a hub for high-end, regulated production and innovation in HPAPIs and continuous processing.

Latin America (emerging; Brazil focal point)

• Market character: Growing local manufacturing capability, supportive policies for GMP upgrades.

• Drivers: Domestic investments, collaborations with global CDMOs.

• Implication: Regional self-sufficiency improves; Brazil can become a regional API export hub.

Middle East & Africa (MEA) and GCC

• Market character: Nascent but rapidly investor-backed; focus on capacity and regulatory reform.

• Drivers: Sovereign investments (Saudi, UAE), healthcare modernization.

• Implication: Long-term diversification of global supply; potential specialized export corridors for niche APIs.

India (special callout due to “Make in India”/PLI)

• Market character: Large generic capabilities, drive to become low-cost global supplier.

• Drivers: PLI funding (₹6,940 crore), domestic pharma ecosystem, strong chemical intermediates base.

• Implication: Accelerated capacity for KSMs/DIs/APIs, greater export competitiveness, and improved resilience for global supply chains.

Market dynamics

Demand dynamics

• Chronic diseases and oncology approvals (50 NMEs example note) sustain long-term API demand; generics keep volume high post-patent cliffs.

Supply dynamics

• Dual trend: reshoring by big pharma + expansion of CDMOs → increases global capacity but shifts where capacity sits (more in APAC plus regional hubs in Brazil/GCC).

Price dynamics

• Branded APIs command higher ASPs; generic competition compresses prices but expands volume — net market value rises because of added higher-value subsegments (HPAPI, sterile injectables).

Regulatory & policy dynamics

• Policy changes (e.g., Germany Medical Research Act) and incentive schemes (India PLI) alter national competitive positions and speed pipeline-to-market timelines.

Technology dynamics

• Adoption of continuous manufacturing, flow chemistry and AI increases productivity and lowers costs per unit, changing unit economics across suppliers.

Competition dynamics

• Legacy large pharmas, global CDMOs, and cost-competitive Asian players form a layered competitive structure — each competes on quality, price, or specialization.

Vertical integration dynamics

• MNCs expanding internal CDMO capabilities (e.g., Pfizer CentreOne model) change the supplier landscape — some capacity becomes captive, some outsourced.

Investment dynamics

• Large CAPEX flows into HPAPI facilities, analytical labs (e.g., SK Pharmteco), and model-based platforms (e.g., Lonza) — this raises structural capacity and capability.

Risk dynamics

• Geopolitical, trade and quality incidents can rapidly shift sourcing — buyers adopt multi-sourcing and risk modelling.

Sustainability & compliance dynamics

• Environmental regulations and green chemistry demands force process re-engineering and capital investments that favor larger, well-capitalized players.

Top 10 companies

Lonza Group

• Product/Offerings: CDMO services for small molecules and biologics, model-based platform (Design2Optimize).

• Overview: Leading Swiss CDMO with global footprint and integrated development→commercial capabilities.

• Strength: Advanced process platforms, end-to-end CDMO scale and early adoption of model-based process acceleration.

Catalent Inc.

• Product/Offerings: Formulation, scale-up, commercial manufacturing (APIs & finished dose solutions).

• Overview: US CDMO specializing in development solutions and drug-delivery technologies.

• Strength: Integrated development + packaging + global supply chain for finished dosage and API needs.

Cambrex Corporation

• Product/Offerings: Process chemistry, API development and manufacturing.

• Overview: Focused API/CDMO specialist with expertise in complex small molecules.

• Strength: Agility in process development and mid-scale commercial supply.

Bachem

• Product/Offerings: Peptide synthesis, GMP peptide APIs and small-molecule manufacturing.

• Overview: Swiss manufacturer with a global reputation for peptide/oligo APIs.

• Strength: Peptide and specialty API manufacturing excellence and GMP compliance.

Siegfried Group

• Product/Offerings: Development, manufacturing and packaging for APIs and finished products.

• Overview: Swiss CDMO offering end-to-end services across regulated markets.

• Strength: Integrated solutions and European regulatory familiarity.

Divi’s Laboratories

• Product/Offerings: Generic APIs, intermediates, KSMs.

• Overview: India-based API manufacturer with broad generic portfolio.

• Strength: Cost-competitive manufacturing and strong supply to generics market.

Aurobindo Pharma

• Product/Offerings: Generic APIs, formulations and global supply to generics markets.

• Overview: Large Indian generics and API producer with global distribution.

• Strength: Scale, cost advantage, and broad product portfolio.

Dr. Reddy’s Laboratories

• Product/Offerings: Innovator + generic APIs, formulations, and CDMO services.

• Overview: Integrated Indian pharma with both domestic and international reach.

• Strength: Balanced innovator/generic capabilities and regulatory experience in multiple markets.

Merck KGaA (MilliporeSigma / Life Science business)

• Product/Offerings: Custom/contract API manufacturing (small molecules & HPAPIs), catalog APIs and lab materials (EMPROVE®).

• Overview: Centuries-old life-science leader with extensive lab consumables → CDMO pipeline.

• Strength: Scale, R&D infrastructure, HPAPI expertise, and integrated supply from lab reagents to commercial API.

Pfizer (Pfizer CentreOne)

• Product/Offerings: Internal API supply plus Pfizer CentreOne CDMO API & intermediates, specialty/complex APIs and sterile injectables.

• Overview: Large innovator pharma with an embedded CDMO arm that services both internal and external demands.

• Strength: Unmatched regulatory trust, complex chemistry capabilities, and secure supply backed by large-cap pharma resources.

Latest announcements

Lonza — Design2Optimize (May 2025)

• What: Launch of a model-based platform aimed at accelerating small-molecule development and manufacturing readiness.

• Why it matters: Model-based tools reduce time from candidate selection to first-in-human by improving predictability of scale-up and process reliability; positions Lonza as a technology leader in CDMO acceleration.

SK Pharmteco — HPAPI analytical lab (Feb 2025)

• What: Opening of an advanced analytical testing laboratory dedicated to HPAPIs.

• Why it matters: Strengthens capabilities for high-potency testing — reduces analytical bottlenecks and supports oncology HPAPI commercialization.

Germany — Medical Research Act (Oct 30, 2024)

• What: Legislation to streamline clinical trial approvals, harmonize ethics committees and incentivize local trials.

• Why it matters: Speeds up clinical development pathways in Germany — increases local API demand for trial supply and shortens time to market for small molecules.

India — PLI Scheme (March 20, 2020, active through 2029–30)

• What: Production Linked Incentive funding (~₹6,940 crore) for KSMs, DIs and APIs.

• Why it matters: Direct capital support to scale manufacturing of intermediates and APIs under “Make in India”, improving global competitiveness and export capability.

Recent developments

Model-driven CDMO acceleration (Lonza) — adoption of AI/model platforms to shorten development timelines and make scale-up more deterministic.

Analytical capacity expansion for HPAPIs (SK Pharmteco) — specialized labs reduce time and regulatory risk for cytotoxic/HPAPI products.

Regulatory liberalization in high-innovation jurisdictions (Germany’s Act) — faster local clinical trial approvals increase regional API demand.

Regional industrial policies (India’s PLI) — large direct funding for KSMs/DIs/APIs that strengthens the global API supply base and lowers costs for generics.

CDMO & pharma strategic shifts — major pharmas formalizing CDMO arms (e.g., Pfizer CentreOne) and broad CDMO capacity expansions to capture market growth.

Segments covered

By Product Type

• Branded/Innovator APIs — high ASPs, patent-protected, require scale for blockbuster volumes; majority revenue contributor (~55% in 2024).

• Generic/Merchant APIs — price competitive, fastest growing; scale and cost structures are decisive.

• HPAPIs & Cytotoxics — specialized containment and analytical needs; high per-unit value.

• Sterile Small-Molecule Injectables — higher technical and regulatory bar; growing due to targeted therapies.

• Controlled Substances & Others — tightly regulated, specialized capabilities.

By Therapeutic Area

• Oncology — largest share (32% in 2024), fast growth due to targeted inhibitors.

• Cardio & Metabolic — chronic disease prevalence drives steady API demand.

• CNS, Anti-infectives, Respiratory & Immunology, Others — represent diversification of demand and influence product mix.

By Molecule/Chemistry Type

• Small-Molecule Organic APIs — bulk of revenue (82% in 2024), easier synthesis/formulation.

• Peptidomimetics & Small Peptides — fastest growth; improved stability and bioavailability expand use.

• Heterocyclic & Specialty Scaffolds — rich source for lead discovery; medicinal chemistry focus.

• Chiral/Enantiomeric APIs — require stereoselective synthesis and specialized analytical control.

By Dosage/Formulation

• Oral Solid Dose APIs — dominant (60% revenue in 2024) due to patient preference and widespread use.

• Injectables — fastest-growing due to rapid therapeutic action and targeted delivery.

• Topicals, Inhalation, Other Delivery Forms — niche but important for specific indications and patient needs.

By End User

• Pharmaceutical Innovator Companies & MNCs — led market (50% in 2024), demand for secure, high-quality supply.

• Generic Drug Manufacturers — fastest growing end user as patents expire and access expands.

• CDMOs/Contract Manufacturers — increasingly central to supply, offering end-to-end capabilities.

• Research Institutes & Emerging Biotech — smaller volumes but high innovation demand.

By Region

• North America, Europe, Asia-Pacific, Latin America, MEA, GCC — each region shows distinct drivers (R&D intensity, cost base, policy incentives).

Top 5 FAQs

-

Q: What is the market size now and where will it be by 2035?

A: The market was US$206.9B in 2025, reached US$219.52B in 2026, and is projected to be about US$374.03B by 2035 (CAGR 6.1% from 2026–2035). -

Q: Which region currently leads the market?

A: North America led with roughly 45% of revenue in 2024, supported by a dense R&D and clinical ecosystem. -

Q: Which segment(s) contributed the largest share in 2024?

A: By product: branded/innovator APIs (~55% of 2024 revenue). By chemistry: small-molecule organic APIs (~82% of 2024 revenue). By therapy: oncology (~32% of 2024 revenue). -

Q: Which segments are expected to grow fastest?

A: Generic/merchant APIs, peptidomimetics & small peptides, injectables, and the oncology therapeutic area are all identified as fastest-growing subsegments during the forecast period. -

Q: How is AI changing the small-molecule API market?

A: AI is accelerating route design, scale-up predictability, PAT-driven process control, analytical method development, supply-chain risk modelling and green-chemistry discovery — collectively reducing time-to-clinic and lowering production costs (see the 10 AI impacts above).

Access our exclusive, data-rich dashboard dedicated to the pharma industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Small Molecule API Market Report Now at: https://www.towardshealthcare.com/checkout/6439

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest