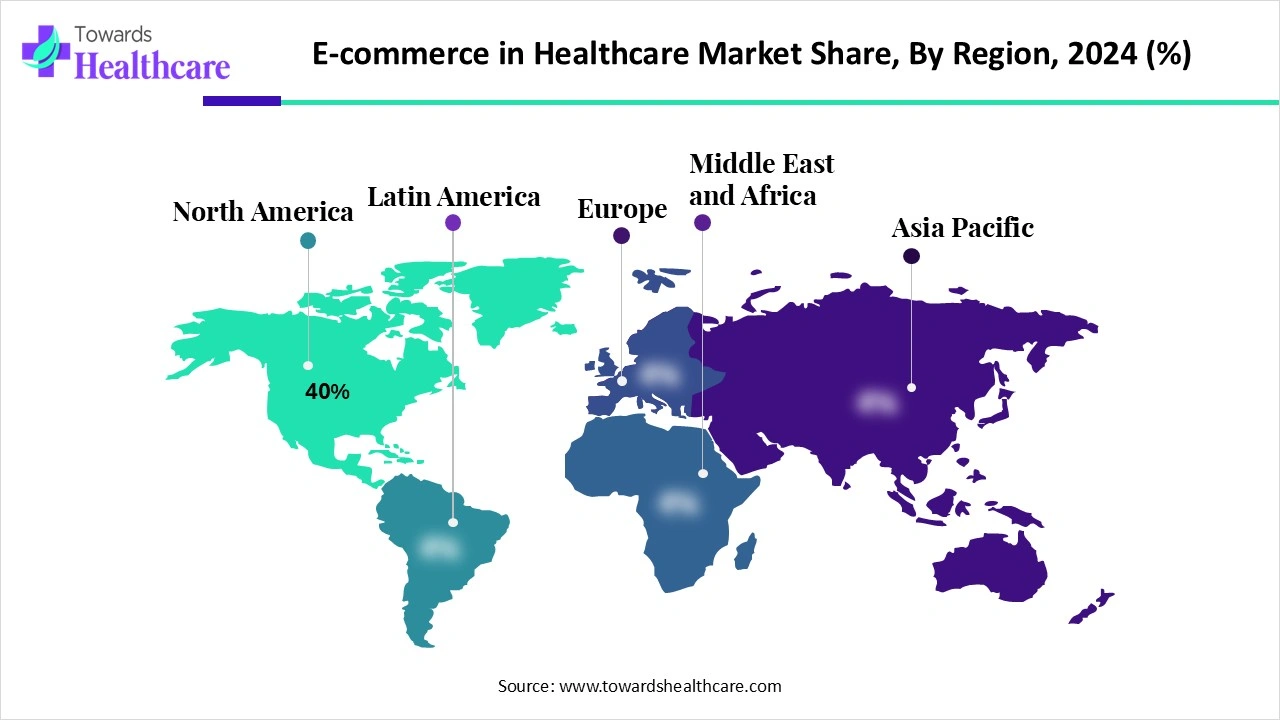

The global e-commerce in healthcare market is experiencing rapid expansion (projected to reach several hundred million dollars by the end of the 2025–2034 forecast window), with strong 2024 market structure signals — North America 40% share (2024), prescription drugs/refills 42% share (2024), online pharmacies 48% platform share (2024), and consumers/patients 70% end-user share (2024) — driven by telehealth, e-prescribing, last-mile logistics improvements, and AI-enabled services.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6067

Market size

Overall market framing (TAM perspective)

◉The total addressable market (TAM) is described in the source as expanding to “several hundred million dollars” by the end of the 2025–2034 forecast horizon. That wording implies a still-maturing but meaningful digital healthcare commerce economy combining Rx, OTC, devices, diagnostics, telehealth bookings, and B2B procurement.

◉The market is multi-revenue: product sales (Rx/OTC/devices), subscription services (DTC, digital therapeutics), telehealth consultation fees + integrated Rx fulfillment fees, logistics/fulfillment revenue, and platform fees (marketplaces/B2B).

2024 anchor metrics (structural shares used to estimate scale)

◉North America: 40% of total 2024 market revenue — indicates a concentration of volume and value there (large per-capita spend, advanced telemedicine adoption, regulatory enablement for e-prescribing).

◉Prescription drugs & refill services: 42% share in 2024 — single largest revenue stream within the e-commerce healthcare stack.

◉Online pharmacies / e-pharmacies: 48% share by platform type in 2024 — nearly half of the market captured by dedicated digital pharmacy platforms.

◉Mail/parcel fulfillment: 50% share of fulfillment models in 2024 — traditional parcel delivery remained the dominant logistics mode even as same-day/on-demand emerged.

◉Consumers/patients: 70% of end-user share in 2024 — the market is consumer-driven today.

Growth posture 2025–2034

◉Expectation is for sustained expansion, with rapid growth pockets in DME (medical devices & durable medical equipment), same-day/on-demand delivery, telehealth + clinical workflow integrations, and DTC/prescription-as-a-service models.

◉The size growth will be driven by (a) broader telehealth uptake tied to e-prescribing, (b) improved last-mile logistics and new delivery modes (drone, e-bike, EV), and (c) platform monetization (subscriptions, marketplace commissions, API integrations).

Revenue mix evolution (qualitative)

◉Short term (2025–2027): Rx/refill + online pharmacies maintain majority revenue; mail/parcel fulfillment remains dominant logistics income.

◉Medium term (2028–2034): DME, telehealth-bundled commerce, and same-day fulfillment capture increasing share; platform services (PaaS for prescription fulfillment, B2B marketplaces) gain higher-margin business.

Key structural levers that determine realized market size

◉Regulatory clarity (e-prescribing, telepharmacy rules) — accelerates addressable Rx volume.

◉Logistics capacity (same-day, temperature-controlled), which unlocks urgent meds and cold-chain devices.

◉Consumer digital literacy and trust — influences conversion rates and average basket sizes.

◉Integration of clinical workflows (RPM data, e-prior auth) — allows enterprise contracts and payer / employer procurement.

Market trends

Post-pandemic acceleration of digital adoption

◉Telehealth and telemedicine remained a catalytic trend since COVID-19, enabling remote diagnosis → digital prescription → online order + home delivery; this converged the care and commerce workflows.

Consolidation of online pharmacies and platform expansion

◉Online pharmacies/e-pharmacies captured 48% platform share in 2024 — incumbents and large retailers (Amazon, Walmart, CVS, Walgreens) are extending pharmacy and fulfillment services, leading to marketplace consolidation and vertically integrated models (telehealth + Rx + logistics).

Shift to omnichannel / DTC and PaaS models

◉DTC brands and Prescription-as-a-Service (PaaS) are expected to grow fastest — brands bypass intermediaries to sell prescription or wellness products directly, often bundled with telehealth and subscription refills.

Logistics evolution: from mail/parcel to same-day & drone

◉Mail/parcel was 50% of fulfillment in 2024, but same-day & on-demand is the fastest growing segment for 2025–2034; investments in drones, EVs, route optimization, and automated lockers are key enablers.

Integration of e-prescribing & prior authorization

◉E-prescribing & e-prior authorization integration led the technology capability share in 2024 — reducing friction from prescribing to fulfillment and enabling safer controlled substance monitoring.

Personalization, recommendation engines, and AI

◉AI drives personalization (product recommendations, refill reminders), operational optimization (inventory forecasting), and customer support (chatbots) — increasing conversion and retention.

Regulatory and trust dynamics

◉Regulatory moves (e.g., India’s e-pharmacy licensing, GDPR/HIPAA in the West) are shaping market participation: tightening verification improves safety but raises compliance costs, filtering out illegitimate operators.

Geographic acceleration: Asia Pacific growth

◉Asia Pacific identified as fastest-growing region due to rising middle class, mobile-first commerce, and significant last-mile opportunities in India, China and Southeast Asia.

Employer & payer penetration

◉Employer & payer segments expected to grow rapidly; these actors will push platforms for telemedicine, digital claims, and subscription Rx management — bringing larger, recurring revenue contracts to platforms.

Healthcare supply chain digitization

◉B2B procurement marketplaces, blockchain for traceability, and fulfillment automation are growing trends to improve transparency, reduce fraud, and optimize procurement costs.

AI impact / role

AI as front-door consumer interface (chatbots, virtual assistants)

◉24/7 symptom checkers and triage bots reduce friction to conversion (recommend OTC vs telehealth vs emergency), schedule teleconsultations, verify prescriptions, and guide users through refill/subscription flows.

◉Outcome: higher self-service transaction rates and lower contact-center costs.

Personalization & recommendation systems

◉AI analyzes purchase history, prescription schedules, comorbidities, and device usage (where allowed) to suggest timely refills, DME upgrades, adherence nudges, and tailored promotions — increasing order frequency and average order value.

Clinical decision support at the commerce edge

◉Integration of e-prescribing with AI decision support can flag drug-drug interactions or propose therapeutic alternatives that are available via the platform, streamlining prescribing + fulfillment and reducing returns or dispensing errors.

Prior-authorization and claims automation

◉AI can automate e-prior authorization workflows, assessing payer rules and generating documentation — reducing clearance times and increasing successful e-prescription fulfillment rates.

Supply chain and inventory intelligence

◉Machine learning models forecast demand at SKU/zip level, optimize inventory allocation across FBA-style nodes, predict cold-chain needs, and dynamically route orders to minimize costs and delivery times.

Logistics & route optimization

◉Real-time AI routing balances same-day delivery commitments, EV/bike constraints, and temperature control needs to improve on-time rates and reduce last-mile CO₂ footprint.

Fraud detection and compliance monitoring

◉AI systems can detect fake prescriptions, anomalous orders (potential abuse), and irregular supply chain patterns; this supports regulatory compliance and protects platform reputation.

AI for customer retention & lifecycle management

◉Churn prediction and tailored retention offers (e.g., switch to subscription, auto-refill incentives) increase lifetime value; natural language generation personalizes outreach while respecting privacy rules.

Clinical workflow integration & remote monitoring

◉AI processes RPM data (e.g., glucose, oxygen saturation) to trigger medication refill suggestions or clinician outreach through platform channels — creating tighter care-commerce loops.

B2B procurement automation

◉For hospitals and clinics, AI automates reordering thresholds, cross-vendor sourcing, and contract compliance, delivering procurement efficiency and improved inventory turns.

Risks & governance of AI

◉Model explainability, bias, data privacy (HIPAA/GDPR compliance), and safety in clinical recommendations are central; platforms must establish human-in-the-loop controls and auditable logging for regulatory acceptability.

Investment signal: AI funding & platform growth

◉Examples in provided data (HealthKois $400M fund; EliseAI $250M series E) illustrate capital flows into AI-enabled health commerce and automation companies, accelerating product maturity and hiring.

Regional insights

North America

◉Market concentration & maturity — 40% share in 2024. High per-capita digital healthcare spend, strong telehealth infrastructures, and established retail pharmacy integration make NA the dominant region.

US specifics

◉Large players (Amazon Pharmacy, Walmart, CVS, Walgreens) integrate logistics and retail footprints.

◉AR/VR experiments (personalization & remote support) and advanced e-prescribing adoption are trends.

◉Regulatory environment: both enabling (HITECH, telehealth reimbursement reforms) and constraining (controlled substance monitoring).

Canada specifics

◉Growing digital health investment (e.g., Phoenix’s $50M raise) supports telehealth + e-commerce expansion.

◉Provincial healthcare models create variability in adoption and procurement, but rising digital spending is favorable.

Asia Pacific

Fastest-growing region expectation

◉Mobile-first consumers, rising middle class with disposable income, and high chronic disease prevalence drive large upside.

India

◉Rapid online pharmacy expansion, AI chatbot adoption, blockchain for supply chain security, and drone delivery pilots (e.g., India First 10-minute diagnostic drone delivery by Apollo + TECHEAGLE).

◉Tata 1mg + Unicommerce partnership to simplify operations across 1,000+ cities underlines logistics and platform scaling focus.

◉ONDC (government-backed) democratization of e-commerce could widen reach for small/local health sellers.

China & Japan

◉China: large online health platforms (Alibaba Health, JD Health) with pharmacy, telehealth, and logistics integration.

◉Japan: AI+IoT integration in health apps, digital payment evolution, and corporate digital health programs drive e-commerce adoption.

Europe

Regulatory trust & data security

◉GDPR and national digital health initiatives encourage secure digital health commerce — enabling cross-border trust but increasing compliance costs.

UK & Western Europe

◉Investment in logistics automation (DHL £550m investment) to support life sciences e-commerce.

◉France: investments in preventative digital healthcare (Withings + French government €20.7m) support consumer health product adoption.

Latin America

Emerging expansion

◉Novo Nordisk launching e-commerce in Latin America (Mexico platform) indicates big pharma entering direct access channels — a sign of commercialization maturation.

◉Key barriers: logistics across large geographies, regulatory heterogeneity, variable digital infrastructure.

Middle East & Africa (MEA)

◉Early adoption pockets (UAE, Saudi) due to high digital penetration and payer/employer programs; elsewhere, infrastructure & regulatory development pace will dictate timing.

Market dynamics

Drivers

◉Ongoing digitization: telehealth + e-prescribing integration — telemedicine adoption directly feeds digital Rx demand and e-commerce conversion.

◉Demographics: aging population & chronic disease prevalence — increases recurring Rx volumes and need for DME/home monitoring.

◉Logistics and fulfillment innovations — same-day delivery, drone pilots, fulfillment networks (FBA-style) support timely delivery for critical meds and devices.

◉Capital inflows into healthtech — funds like HealthKois ($400M) and company raises (e.g., EliseAI $250M) accelerate product development and distribution expansion.

◉Platformization and DTC models — brands using subscription and PaaS strategies increase recurring revenue and margin capture.

Restraints

◉Digital literacy & consumer trust gaps — especially in older and rural populations limiting adoption; requires user education and simplified UX.

◉Regulatory & compliance complexity — HIPAA/GDPR and country-level e-pharmacy rules increase compliance cost and operational friction.

◉Controlled substances / abuse risk — necessitates stringent verification and monitoring systems.

◉Logistics constraints in last-mile and rural delivery — many markets still lack consistent same-day capability, impacting service reach.

Opportunities

◉Same-day & drone delivery expansion — unlocks urgent med delivery, on-demand care logistics, and new service tiers (e.g., perishable biologics).

◉B2B procurement marketplaces — digitalizing hospital/clinic procurement improves margins and creates sticky enterprise relationships.

◉Employer/payer partnerships — offering curated telehealth + Rx bundles to employees/members provides scale and recurring revenue.

◉AI-driven personalization & operational automation — reduces costs, improves adherence and cross-sell/up-sell potential.

◉Untapped geographies & pin code reach — e.g., Zeno Health reaching 23,000 pin codes in India expands addressable user base.

Top companies

Amazon Pharmacy / PillPack

◉Product / offering: End-to-end online pharmacy and fulfillment (subscription refills, integrated logistics).

◉Overview: Retail & cloud giant leveraging vast fulfillment network to distribute Rx/OTC and integrate digital services.

◉Strengths: Massive logistics & FBA capability, scale, brand trust, data assets for personalization, and ability to bundle services (Prime).

Walmart Health / Walmart Pharmacy

◉Product / offering: Omnichannel health retail (in-store pickup + online pharmacies), integration with Walmart’s logistics.

◉Overview: Large retailer deploying omnichannel strategies to capture pharmacy & DME commerce.

◉Strengths: Physical footprint + e-commerce scale, low-cost positioning, and same-day/local pickup options.

CVS Health / Caremark

◉Product / offering: Pharmacy services, PBM (Caremark), digital health integration, and patient fulfillment.

◉Overview: Integrated pharmacy chain + benefits manager enabling closed-loop Rx fulfillment and payer relationships.

◉Strengths: Clinical integration via retail clinics, payer relationships, large Rx volume and compliance experience.

Walgreens Boots Alliance

◉Product / offering: Retail pharmacy network with digital pharmacy services and logistics partnerships.

◉Overview: Wide retail footprint in US/Europe acts as pickup and fulfillment hubs for digital orders.

◉Strengths: Local accessibility, retail + online hybrid model, and convenience services.

GoodRx

◉Product / offering: Price transparency & discount platform, connecting consumers to lower-cost Rx options and e-commerce links.

◉Overview: Consumer cost-comparison platform driving traffic and conversions to pharmacies.

◉Strengths: Consumer search/price discovery audience and partnerships with pharmacies for conversion.

McKesson / Cardinal Health / AmerisourceBergen

◉Product / offering: Distributors and wholesale logistics, supporting pharmacy inventories and B2B procurement.

◉Overview: Backbone of medication supply and logistics for e-commerce fulfillment and cold-chain.

◉Strengths: Scale distribution networks, regulatory expertise, and B2B contracting power.

Zuellig Pharma / Zuellig Healthcare

◉Product / offering: Regional distribution & logistics across Asia Pacific, supporting pharma e-commerce.

◉Overview: Distributor with presence in markets where last-mile logistics are complex.

◉Strengths: Regional logistics expertise, cold-chain capabilities, and relationships with local providers.

Alibaba Health / JD Health

◉Product / offering: Large Chinese e-commerce healthcare platforms combining pharmacy, telehealth, and logistics.

◉Overview: Platform-led consumer health ecosystems with integrated payment and delivery.

◉Strengths: Massive consumer reach, payment integration, and strong logistics partnerships.

Ping An Good Doctor

◉Product / offering: Integrated telehealth + e-pharmacy + digital health services in China.

◉Overview: Platform combining insurance, telemedicine, and commerce.

◉Strengths: Insurance and platform integration enabling user acquisition and retention.

Shop Apotheke / Zur Rose Group / DocMorris

◉Product / offering: European online pharmacy players with cross-border fulfillment and pharmacy services.

◉Overview: Pan-EU e-pharmacy models capitalizing on cross-border e-commerce and DME sales.

◉Strengths: Regulatory navigation, European logistics specialization, and pharmacy licensing.

PharmEasy / 1mg / Netmeds (India)

◉Product / offering: Indian online pharmacy ecosystems offering Rx refills, logistics, and telehealth tie-ins.

◉Overview: Rapidly scaling players in India enabling massive pin-code reach and mobile commerce.

◉Strengths: Local market knowledge, partnerships (e.g., Tata 1mg + Unicommerce), and logistics scaling.

Capsule / Blink Health / NowRx / Zipline / Teladoc / Amwell / Rite Aid

◉Product / offering & strengths: Capsule (fast local delivery & tech-first pharmacy), Blink Health (consumer savings), NowRx (ultra-fast delivery), Zipline (drone logistics), Teladoc/Amwell (telehealth platforms integrating Rx), Rite Aid (retail + pharmacy). Each contributes specialization in speed, technology, telehealth or logistics.

Latest announcements

HealthKois — June 2025

◉Announcement: $400 million sector-specific fund to back early growth-stage companies across healthtech, biopharma, medtech, healthcare delivery, and climate health.

◉Implication: Large capital pool accelerates startups building commerce integrations (telehealth + Rx + logistics), AI applications and supply chain innovations — fueling faster productization and market entry.

Tata 1mg + Unicommerce — May 2025

◉Announcement: Partnership to simplify e-commerce operations across 1,000+ Indian cities.

◉Implication: Strengthens last-mile and seller operations in India, enabling broader pin-code coverage and better inventory/fulfillment management for pharmacy & DME sellers.

Health-E Commerce® + LifeMD™ — Feb 2025

◉Announcement: Telehealth collaboration to make weight-management medications accessible through FSA Store and HSA Store.

◉Implication: Demonstrates integration of telehealth prescribing with tax-advantaged health spending platforms — new commercial channels and improved affordability.

EliseAI — August 2025

◉Announcement: $250M Series E to automate healthcare and housing, hiring to drive growth.

◉Implication: Significant funding into AI automation reflects investor confidence in AI operationalizing service delivery for e-commerce in healthcare (e.g., chatbots, supply chain automation).

WELL Health — June 2025

◉Announcement: Availability for 45,000 new primary care patients across 3 provinces via physician recruitment and digital transformation investments.

◉Implication: Scaling of primary care capacity tied to digital platforms increases telehealth appointment supply, which feeds Rx demand for e-commerce channels.

Esyms + DHL eCommerce Malaysia — March 2025

◉Announcement: Collaboration to transform medicine distribution in Malaysia.

◉Implication: Strategic logistics partnerships are crucial for improving delivery speed and reliability in regionally diverse markets.

Novo Nordisk — July 2025

◉Announcement: Launched primary e-commerce platform in Latin America (Mexico) offering direct access to therapies.

◉Implication: Pharma taking direct channel approaches to reach patients — a structural shift creating manufacturer-to-patient commerce flows.

Davaindia — April 2025

◉Announcement: Launched an e-commerce platform in Pune focused on affordable and accessible healthcare delivery.

◉Implication: Localized platforms aiming at affordability expand market inclusion and reach.

Apollo Hospitals & TECHEAGLE — Feb 2025

◉Announcement: India’s first 10-minute diagnostic drone delivery.

◉Implication: Demonstrates extreme last-mile innovation for urgent diagnostics and potential for urgent med delivery in urban/rural challenging areas.

Zeno Health — July 2025

◉Announcement: Launched e-commerce operations to reach over 23,000 pin codes for medicine delivery.

◉Implication: Massive geographic reach increase in India, addressing access gaps and boosting potential addressable market.

Withings + French Government — Dec 2024

◉Announcement: €20.7M investment to advance preventative digital healthcare in France.

◉Implication: Government + private funding to support preventative device/digital commerce penetration.

Phoenix (Canada) — March 2025

◉Announcement: $50M investment to expand access to men’s digital health.

◉Implication: Niche telehealth + commerce verticals gaining capital to scale.

Recent developments

◉Platform launches & expansions

Novo Nordisk (Latin America), Davaindia (Pune), Zeno Health (India pin code expansion) represent manufacturer, local platform, and logistics reach expansions — collectively increasing market coverage and direct access.

◉Logistics & partnerships

Tata 1mg + Unicommerce and Esyms + DHL highlight strategic tie-ups to solve operational complexity (inventory, parcel networks) — crucial to scale mail/parcel and same-day services.

◉AI / investment momentum

HealthKois and EliseAI funding rounds inject capital for AI and growth-stage scaling — accelerating automation, personalization, and operational resilience.

◉Drone & ultra-fast delivery pilots

Apollo + TECHEAGLE diagnostic drone and Zipline mentions indicate experimentation with non-conventional last-mile methods for critical deliveries.

◉Policy & regulatory shifts

India’s move to regulate e-pharmacies (licensing, prescription verification) will reshape marketplace composition, removing bad actors and increasing trust but also raising compliance requirements.

◉Employer/payer & FSA/HSA integration

Health-E Commerce & LifeMD integration with FSA/HSA stores shows commercial innovation to improve affordability and consumer access.

Segments covered

By Product / Service Type

◉Prescription Drugs & Refill Services — Largest 2024 share (42%). Core revenue engine: recurring prescriptions, chronic care management, and refill automation (subscriptions). Integration needs: e-prescribing, adherence reminders, e-prior auth.

◉OTC & Consumer Health Products — Fast consumer demand, lower regulatory friction, higher margins for DTC brands; used for cross-sell and acquisition funnels.

◉Medical Devices & Durable Medical Equipment (DME) — Expected rapid growth (2025–2034): includes wheelchairs, oxygen concentrators, remote monitors; requires logistics for size/weight and sometimes cold-chain or installation support.

◉Home Diagnostics & At-home Test Kits — Growth via telehealth recommendation; requires secure sample logistics (where applicable) and regulatory compliance for medical testing.

◉Telehealth + e-prescribing bundled services — Platform bundles clinical consult + e-prescription + fulfillment; high conversion and stickiness when integrated.

◉Digital Therapeutics & Subscription Care Programs — Recurring revenue models; requires clinical evidence and reimbursement model alignment.

◉B2B Healthcare Procurement Marketplaces — Enterprise procurement for clinics/hospitals: bulk purchasing, contract compliance, and logistics; attractive higher-ticket, lower-frequency but sticky revenue.

By Platform Type / Business Model

◉Online Pharmacies / e-Pharmacies — Core transactional platforms for Rx & OTC; led in 2024 (48% platform share).

◉Retailer Omnichannel — Brick-and-mortar retailers integrating online ordering + in-store pickup for convenience and cost efficiency.

◉Marketplaces / Aggregators — Comparison and multi-seller marketplaces aggregating choice; monetize via commissions.

◉Direct-to-Consumer (DTC) & Prescription-as-a-Service (PaaS) — Brands and PaaS enablement platforms sell direct, often subscription-based; high margin potential.

◉B2B Marketplaces & Procurement Platforms — Serve clinics, distributors, and hospitals — often with integration into ERP and inventory systems.

By Fulfillment & Delivery Model

◉Mail / Parcel Fulfillment — Dominant in 2024 (50%); uses existing parcel networks for non-urgent deliveries.

◉Same-day & On-demand Delivery — Fastest CAGR expected; requires localized dark stores, micro-fulfillment, and route optimization.

◉Click-and-Collect / In-store Pickup — Hybrid model reducing delivery costs and leveraging retail footprint.

◉Locker & Automated Pickup Points — Secure pickup for discreet products and to serve dense urban areas.

◉Clinic / Telehealth-linked Fulfillment — Direct-to-patient fulfillment from point of care for convenience and adherence.

By End User

◉Consumers / Patients — Largest segment (70% in 2024) — direct retail transactions and subscription management.

◉Healthcare Providers & Clinics — Purchase DME and consumables for patient care; procurement marketplaces serve this group.

◉Employers & Payers — Growing fast; often procure at scale for members/employees and drive telehealth + Rx benefits.

◉Pharmacies & Distributors — Use platforms for reorder, inventory management, and multi-channel fulfillment.

By Technology / Capability

◉E-prescribing & e-prior authorization integration — Key enabler for Rx commerce and compliance.

◉Mobile Apps & Consumer UX — Mobile-first UX critical in APAC and emerging markets.

◉Telehealth integration & clinical workflow — Connects care delivery to commerce; drives conversions.

◉AI / Personalization & Recommendation Engines — Improves conversion, supply planning, and customer lifetime value.

◉Fulfillment Automation, Inventory & Cold-chain tech — Enables DME and temperature-sensitive product distribution.

◉Payment & Reimbursement Integrations — FSA/HSA, payer APIs, and installment/payment options expand affordability.

Top 5 FAQs

Q: Which region dominated the e-commerce in healthcare market in 2024?

A: North America dominated with approximately 40% of the market in 2024.

Q: Which product/service segment led the market in 2024?

A: Prescription drugs & refill services led the market in 2024 with roughly 42% share.

Q: Which platform/business model held the largest share in 2024?

A: Online pharmacies / e-pharmacies captured about 48% platform share in 2024.

Q: Which fulfillment model was dominant in 2024 and which is expected to grow fastest?

A: Mail/parcel fulfillment was dominant in 2024 (50% share). Same-day & on-demand delivery is expected to register the fastest CAGR over 2025–2034.

Q: How is AI impacting the e-commerce in healthcare market?

A: AI is driving 24/7 virtual assistants and chatbots for symptom checking and scheduling, powering personalization and recommendation engines, automating B2B procurement and e-prior authorization, optimizing inventory and last-mile logistics, and enabling fraud/compliance detection — with major funding examples like HealthKois ($400M fund) and EliseAI ($250M Series E) accelerating these capabilities.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/6067

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest