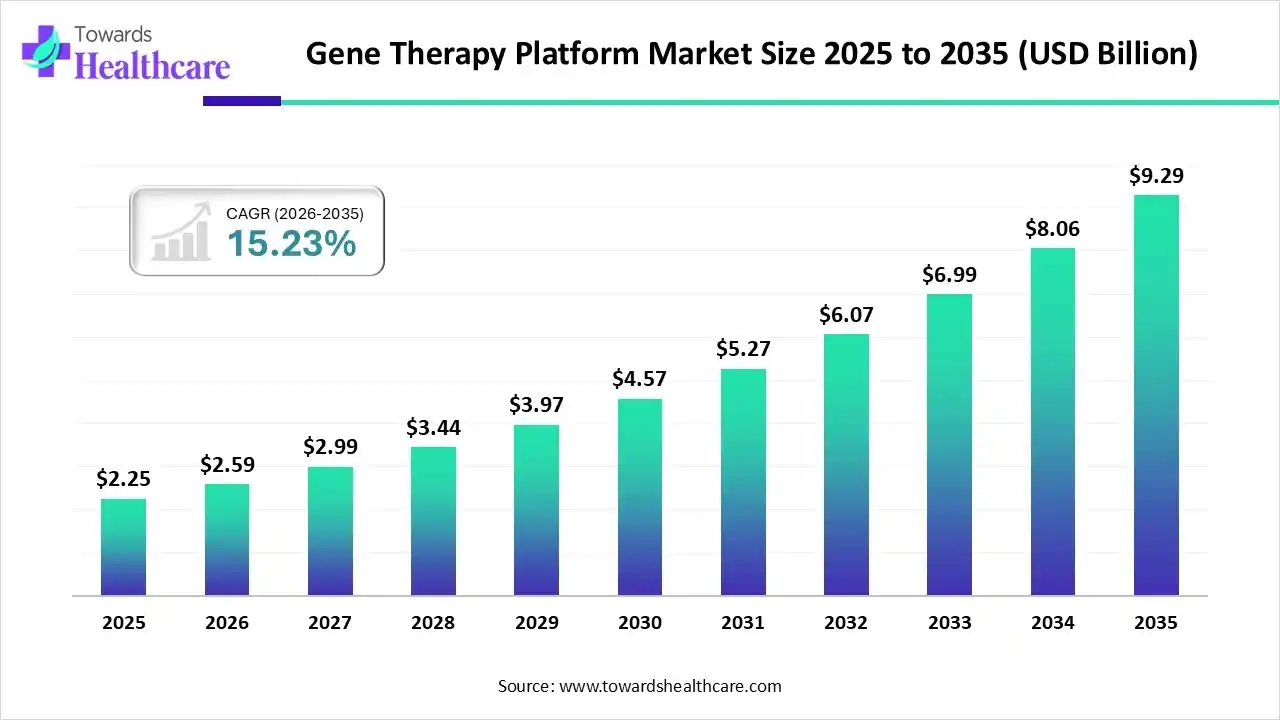

Gene therapy platform market valued at US$ 2.25 billion in 2025, the market is projected to grow to US$ 2.59 billion in 2026 and surge to approximately US$ 9.29 billion by 2035, expanding at a compelling 15.23% CAGR. These numbers signal more than economic expansion; they reflect a profound shift in how the medical community approaches genetic and chronic disease.

Download Free Sample Report: https://www.towardshealthcare.com/download-sample/6506

This is not incremental innovation. This is structural reinvention.

Rewriting Medicine at the Genetic Level

A gene therapy platform functions as the foundational infrastructure for delivering therapeutic genes into cells. It enables scientists and clinicians to:

-

Replace defective genes

-

Insert functional genes

-

Silence harmful gene expression

-

Precisely edit DNA sequences

Unlike conventional pharmaceuticals that require repeated dosing, many gene therapies aim for long-term or even single-dose treatment outcomes. Viral vectors, lipid nanoparticles, CRISPR-based editing tools, and advanced analytics systems form the technological backbone of these platforms.

What distinguishes modern gene therapy platforms is their integration of delivery science, genomic editing, scalable manufacturing, and increasingly, artificial intelligence.

The Market in Motion: Key Structural Insights

The gene therapy platform market is expanding across multiple dimensions:

-

North America led the global market in 2025 with a 35% share.

-

Asia Pacific is projected to grow at the fastest rate.

-

Viral vector platforms captured 50% of the product-type share.

-

Oncology applications accounted for 45% of market share.

-

On-premise R&D models dominated deployment with 55% share, though cloud-based analytics is accelerating.

These figures reflect where the industry stands today—and where it is heading tomorrow.

Why Viral Vectors Still Lead the Platform Race

Viral vector-based gene therapy platforms held half of the market share in 2025. Researchers rely heavily on:

-

Adeno-associated viruses (AAV)

-

Adenoviruses

-

Lentiviral vectors

These vectors have demonstrated promising clinical outcomes across oncology and rare genetic disorders. Their reliability, regulatory familiarity, and clinical validation provide confidence in product development and commercialization.

However, viral systems are not without challenges. Immunogenicity, production complexity, and scalability constraints continue to demand innovation.

Non-Viral Platforms: The Silent Disruptors

While viral platforms dominate today, non-viral technologies are rising rapidly.

Lipid nanoparticles (LNPs), plasmid DNA systems, and GalNAc-based delivery models offer:

-

Lower immunogenicity

-

Greater scalability

-

Reduced manufacturing complexity

-

Cost advantages

The success of mRNA-based therapeutics during global health crises has also validated non-viral delivery as a credible, flexible approach. As gene editing moves beyond rare diseases into broader indications, non-viral platforms may gain strategic importance.

AI: The Invisible Architect of Gene Therapy

Artificial intelligence is not an accessory to gene therapy—it is becoming its operational brain.

AI-driven systems analyze:

-

Genomic sequences

-

Off-target mutation risks

-

Protein expression patterns

-

Clinical outcomes

-

Patient-specific biological variables

These models help researchers design guide RNA (gRNA) sequences with optimal on-target activity while minimizing unintended effects. Machine learning platforms can process vast genomic datasets and simulate editing outcomes before laboratory validation begins.

As datasets expand, AI models will move from optimization tools to predictive therapeutic design engines.

Oncology Leads—But Rare Diseases Accelerate

In 2025, oncology captured 45% of the application segment. Gene editing now allows precise targeting of oncogenes and resistance pathways, enabling therapies that address cancer at its molecular roots.

CAR-T therapies and gene-modified immune cells are reshaping hematological malignancy treatment. For example, innovations from companies like Novartis AG and Gilead Sciences, Inc. have advanced cell-based oncology platforms significantly.

Meanwhile, rare genetic disorders are emerging as the fastest-growing segment. Many rare diseases are monogenic—caused by a mutation in a single gene—making them ideal candidates for gene replacement therapy.

This dual momentum—high-volume oncology and precision rare disease targeting—creates a balanced expansion model for the market.

Deployment Dynamics: Why In-House R&D Still Dominates

In-house R&D environments accounted for 55% of deployment share in 2025. Organizations prefer on-premise models because they offer:

-

Full control over vector design and manufacturing

-

Rapid iteration in process development

-

Direct oversight of Chemistry, Manufacturing, and Controls (CMC)

-

Secure handling of patient-specific therapies

For cell therapies with limited shelf life, time-sensitive workflows demand operational autonomy.

However, cloud-based analytics platforms are expanding rapidly. Remote computational infrastructure enables scalable antibody discovery, gene sequence analysis, and real-time trial monitoring without heavy capital expenditure in hardware.

Hybrid deployment models may define the next phase.

Manufacturing: The Industry’s Most Complex Challenge

Gene therapy manufacturing differs fundamentally from traditional pharmaceutical production. Scaling viral vectors or gene-edited cells from laboratory batches to commercial volumes introduces logistical and regulatory complexities.

Automation now streamlines:

-

Genetic modification

-

Cell extraction

-

Expansion

-

Purification

-

Formulation

Advanced biomanufacturing hubs are emerging globally to address scalability constraints. The ability to industrialize gene therapy production will determine how quickly treatments become accessible beyond niche patient populations.

Regional Forces Shaping the Market

North America: Infrastructure and Investment Power

North America dominated the market in 2025, driven by strong biotech ecosystems, venture capital funding, and regulatory frameworks supportive of advanced therapies.

The United States benefits from:

-

A robust clinical pipeline

-

Active FDA engagement

-

Substantial NIH funding

-

Nearly 3,500 therapies in preclinical and clinical development

Companies like Pfizer Inc. and Johnson & Johnson continue exploring transformative gene therapy strategies.

Asia Pacific: Policy-Driven Acceleration

Asia Pacific is emerging as the fastest-growing region. Governments across China, Japan, South Korea, and India are investing heavily in biotechnology infrastructure.

India has launched indigenous CRISPR-based therapies and humanized CAR-T innovations with support from national biotechnology agencies. Private investment from firms such as Bharat Biotech reflects growing domestic capability.

Large patient pools, expanding manufacturing capacity, and cost-efficient research models position the region as a future powerhouse in gene therapy platforms.

Europe: Regulatory Evolution and Rare Disease Leadership

Europe continues to advance gene therapy through regulatory approvals and clinical trial expansion. Organizations like European Medicines Agency have approved landmark therapies such as Casgevy and Libmeldy.

The United Kingdom leads Europe in cell and gene therapy trials, supported by collaborative innovation networks and translational research hubs.

Europe’s strong rare disease focus reinforces its strategic importance in gene therapy advancement.

China’s Clinical Momentum in Immune Cell Therapies

Recent clinical trial data in China reveals a strong focus on CAR-T therapies, accounting for approximately 83% of immune cell and gene therapy trials. TIL, NK, CAR-NK, and dendritic cell therapies also show growing representation.

This signals a concentrated push toward immune-modified gene therapies, especially in oncology.

The Competitive Landscape: Strategic Realignments

Leading players are restructuring portfolios to align with platform-driven growth.

-

BioMarin Pharmaceutical Inc. has reconsidered parts of its gene therapy portfolio.

-

Sarepta Therapeutics, Inc. is prioritizing siRNA platform assets.

-

bluebird bio, Inc. completed strategic acquisitions to reposition operations.

-

uniQure N.V. continues advancing therapies for neurodegenerative disorders.

The competitive environment reflects a maturing industry where platform scalability and pipeline efficiency determine long-term positioning.

SWOT Perspective: Where the Industry Stands

Strengths

-

Root-cause disease intervention

-

Potential for long-term or curative outcomes

-

Reduced dependency on chronic medication

Weaknesses

-

High treatment costs

-

Complex manufacturing

-

Risk of off-target genetic effects

Opportunities

-

Automation in CGT development

-

Advances in viral and non-viral vector engineering

-

AI-powered genomic analytics

-

Expansion into neurodegenerative and cardiovascular indications

Threats

-

Scalability barriers

-

Reimbursement challenges

-

Regulatory variability across regions

The balance between technological innovation and economic accessibility will define the next decade.

Value Chain: From Bench to Bedside

The gene therapy platform value chain spans:

-

R&D – Vector design, CRISPR editing, toxicology testing

-

Clinical Trials – Regulatory navigation and long-term monitoring

-

Manufacturing – Viral vector scaling and cell processing

-

Patient Services – Logistics, reimbursement support, treatment coordination

Companies like CRISPR Therapeutics and Roche contribute to upstream innovation, while firms such as REGENXBIO focus on clinical translation.

This integrated ecosystem underscores that gene therapy is not a single product—it is a platform economy.

The Long-Term Outlook: Precision Meets Scalability

By 2035, the gene therapy platform market is expected to approach US$ 9.29 billion. However, market value only tells part of the story.

Three structural shifts will define the next decade:

-

Convergence of AI and Genomics – Predictive editing and personalized design.

-

Industrialized Biomanufacturing – Automated, high-throughput vector production.

-

Affordable Precision Medicine – Expansion beyond rare diseases into broader chronic conditions.

The industry stands at a crossroads. If stakeholders successfully align regulation, cost structures, and manufacturing scalability, gene therapy platforms could transition from niche solutions to mainstream medical infrastructure.

Final Reflection: Cure, Control, or Transformation?

Gene therapy platforms challenge the traditional pharmaceutical model. They promise interventions that target the biological source of disease rather than managing symptoms indefinitely.

Yet the transition from promise to accessibility requires overcoming cost, scalability, and ethical complexities.

As AI integrates deeper, non-viral vectors mature, and governments invest strategically, gene therapy may redefine how healthcare systems conceptualize treatment itself.

The question is no longer whether gene therapy works.

The real question is: How fast can the world make it accessible to everyone who needs it?

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Gene Therapy Platform Market Report Now at: https://www.towardshealthcare.com/checkout/6506

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest