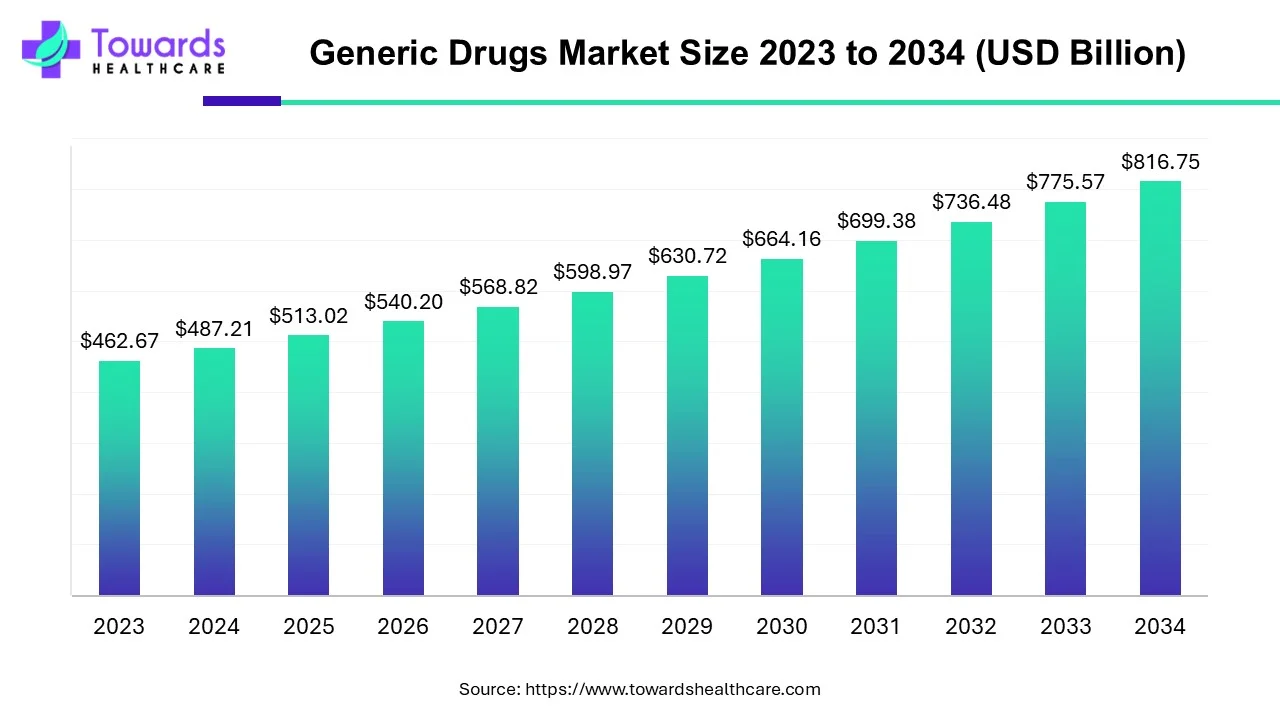

The global generic drugs market, valued at USD 487.21 billion in 2024, is projected to grow to USD 816.75 billion by 2034 (rising from USD 513.02 billion in 2025) at a CAGR of 5.3% (2025–2034), driven by patent expiries, rising approvals and expanding funding for generics.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5053

Market size

Current base and near-term anchor.

• 2024 reported market value: USD 487.21 billion — this is the latest baseline figure used for trend interpretation.

• 2025 intermediate figure cited: USD 513.02 billion — represents early growth as new approvals and policy actions start to take effect.

Long-term projection.

• 2034 forecast: USD 816.75 billion, reflecting cumulative expansion from increased approvals, manufacturing scale-up, and policy pushes to substitute generics for branded medicines.

Growth rate context.

• CAGR 2025–2034: 5.3% — steady, mid-single-digit growth consistent with large, mature pharmaceutical segments shifting share to generics as biologics/big brands lose exclusivity.

Value-driven composition (structural observation).

• Although volume penetration of generics is extremely high (e.g., >90% of U.S. dispensed prescriptions are generics), value growth is slower due to price erosion; therefore market growth is primarily volume + new product approvals + geographic expansion rather than price inflation.

Funding and investment lift.

• Increased public and private funding (R&D grants, manufacturing incentives) is explicitly cited as a major contributor to the forecasted expansion to USD 816.75B.

Supply chain and capacity impact.

• Investments in API and finished-dose capacity (e.g., announced collaboration for lomustine manufacture) are important to convert demand into realized sales growth.

Policy / structural shocks accounted for.

• Large government interventions (e.g., PMBJK expansion in India, CMS $2 list program) are modelled to accelerate adoption and distribution, especially through retail channels.

Time-phasing of growth.

• Near term (2024–2026): approvals and policy actions produce step-ups; mid term (2027–2030): manufacturing scale and international penetration; late term (2031–2034): continued expansion but moderated by market saturation in mature classes.

Market trends

Policy push toward affordability.

• India’s PMBJK expansion (14,000+ stores announced Dec 2024) increases low-cost access domestically and strengthens India’s export position.

• U.S. CMS initiative (Oct 2024) to make 101 generics available at $2/month for Medicare enrollees (implementation by Jan 2027) will reduce out-of-pocket costs and increase generic utilization.

Rising first-time approvals accelerate portfolio growth.

• Multiple first-time generic approvals (examples in 2023 list above) show active pipeline conversion — each new approval converts branded spend to lower-priced generics.

API and domestic manufacturing expansion.

• Collaborations (e.g., API Innovation Center + Apertus) to bring critical APIs and finished products back into domestic supply chains reduce shortage risk and support price stability.

Funding increases R&D and capacity.

• Public and private funding targeted at generic R&D and manufacturing improves quality compliance and shortens time to market.

Retail channel dominance with omnichannel growth.

• Retail pharmacies led 2024 distribution; emergence of home delivery and online pharmacies enhances convenience and adherence, especially for chronic therapies.

Hospital pharmacy growth for complex generics.

• Hospital pharmacies expected to grow for injectable and specialty generics that require clinical handling and inpatient use.

Market saturation and price erosion in mature molecules.

• Intense competition for off-patent molecules leads to commoditization, margin compression and rationalization among suppliers.

Specialty injectables and complex generics gaining share.

• Injectables and harder-to-manufacture generics are attracting entrants because they preserve better margins and fewer competitors.

Globalization of supply and geographic rebalancing.

• India remains a major supplier (≈20% global API/finished supply), while North America remains the largest revenue market due to higher unit prices and volumes.

Increased utilization and acceptance of generics.

• Awareness campaigns, payer incentives and clinical guidelines continue to push substitution rates upward — generating system savings (e.g., multibillion dollar savings cited for U.S. stakeholders).

10 ways AI can impact generic drugs market

Formulation design and excipient selection (preclinical / development).

• AI models predict optimal excipient–API interactions, improving bioavailability and stability for generic formulations.

• Result: shortened formulation cycles and higher first-pass success rates in bioequivalence studies.

Bioequivalence prediction and in-silico testing.

• ML algorithms can model pharmacokinetic (PK) profiles to predict BE equivalence to reference drugs, reducing the number of costly in-vivo studies required.

• Result: lower development cost and faster regulatory submissions.

Analytical method optimization.

• AI helps develop robust, high-throughput analytical methods (HPLC, dissolution) and flags batch anomalies early.

• Result: increased QA/QC throughput and fewer batch rejections.

Manufacturing process automation and predictive maintenance.

• AI monitors equipment signals to predict failures and optimize process parameters (mixing, granulation, coating).

• Result: higher yield, less downtime, and consistent product quality for commoditized generics.

Supply chain optimization and shortage prediction.

• Models ingest multi-source data (API supply, raw material lead times, demand patterns) to forecast shortages and re-route sourcing.

• Result: resilient supplies for essential off-patent drugs and decreased stockouts.

Regulatory submission intelligence.

• NLP tools assemble and check regulatory dossiers (ANDA, stability reports), suggesting likely queries and gaps.

• Result: fewer regulatory cycles and faster approval timelines.

Automated pharmacovigilance and post-market monitoring.

• ML analyzes real-world data and social reporting to detect signals for generic tolerability or efficacy issues.

• Result: quicker mitigation and stronger safety profiles.

Manufacturing scale selection and capacity planning.

• Demand forecasting models suggest where to scale production (geography, dosage strengths), optimizing CAPEX allocation.

• Result: smarter investment in facilities and API capacity.

Commercial intelligence and pricing optimization.

• AI analyzes competitor launches, price erosion curves and payer behavior to set launch pricing and timing.

• Result: better margin management in highly competitive molecule classes.

Clinical trial optimization for complex generics.

• For complex generics or biosimilars, AI can optimize trial design, patient selection and endpoint prediction to reduce time and cost.

• Result: more feasible development economics for specialty generic entrants.

Regional insights

North America (lead region; revenue-heavy).

• Market characteristics: highest revenue per prescription due to large insured populations and high unit service pricing.

• Structural drivers: aggressive substitution policies, payer incentives, GDUFA and FDA generic programs accelerating approvals.

• Consequence: while penetration (volume) is high (>90% of dispensed prescriptions), revenue growth depends on converting specialty and injectable classes to generics.

Asia-Pacific (fastest growing; manufacturing hub).

• India: major global supplier (~20% share of global supply cited), strong PMBJK domestic program (14,000+ outlets) expanding domestic consumption and export capability.

• China/Japan/South Korea: growing domestic capacity and regulatory modernization support exports.

• Consequence: strong manufacturing scale enables global price competition but also drives consolidation among low-margin suppliers.

Europe (regulated, quality-focused).

• Market drivers: national tendering in many countries, price referencing and substitution rules.

• Consequence: fiercely price-competitive tenders for widely used molecules; opportunities for differentiated complex generics.

Latin America (access expansion potential).

• Market traits: pockets of high unmet access; governments increasingly pursue generics to expand coverage.

• Consequence: export opportunities for Indian manufacturers and growth for local retail pharmacy penetration.

Middle East & Africa (emerging demand; procurement reliance).

• Traits: many countries rely on imports; government procurement programs and donor agencies drive volume purchases.

• Consequence: opportunity for international suppliers to secure large tenders; need for quality assurances and stable API supply.

Regional R&D / Approval differences.

• Observation: regulatory timelines and bioequivalence requirements vary regionally; successful generics companies tailor dossier strategies region by region.

• Consequence: companies with regulatory agility capture faster market entry and share.

Logistics and trade flow.

• APAC → global exports (APIs, finished dose) are central; supply-chain disruptions in one region ripple worldwide.

• Consequence: onshoring or dual-sourcing strategies gain traction in North America/Europe.

Market dynamics

Primary drivers

• Patent expirations/off-exclusivity create large addressable markets for generics.

• Policy initiatives (e.g., PMBJK, CMS $2 list) drive substitution and higher utilization.

• Rising chronic disease prevalence (diabetes, CVD) increases demand for long-term, low-cost medicines.

• Increased funding and manufacturing investments accelerate capacity and approvals.

Key restraints

• Market saturation for commoditized molecules → price compression and shrinking margins.

• Regulatory complexity and costs for quality compliance remain barriers for smaller players.

• Supply chain concentration risks (API dependence) can cause shortages or quality recalls.

Opportunities

• Complex generics and injectables: fewer competitors, higher margins.

• Geographic expansion into under-penetrated markets (LATAM, MEA).

• AI and digital tools to compress development time and reduce regulatory cycles.

• Consolidation and M&A to achieve scale and secure supply lines.

Threats

• Intense price competition leading to product withdrawals and supplier failures.

• Regulatory scrutiny or product recalls damaging trust and market access.

• Policy changes altering reimbursement or substitution rules.

Supply dynamics

• API availability and cost drives finished-dose economics — vertical integration (API + FDF) becomes a strategic advantage.

• Manufacturing lead times and capacity additions are key to realizing forecasted growth.

Commercial dynamics

• Retail pharmacies dominate distribution; online pharmacies and home delivery change adherence patterns.

• Hospital procurement favors reliable supply and clinical support for injectables and specialty generics.

Innovation dynamics

• “Innovation” in generics focuses on process improvements, complex formulations (e.g., chewables, extended release), and delivery systems rather than new molecules.

Top 10 companies

Abbott Laboratories

• Product/overview: global diversified healthcare firm with generics/OTC and diagnostics portfolios.

• Strengths: broad commercial footprint, supply chain scale, strong brand recognition in multiple markets.

Allergan

• Product/overview: historically known for branded products but operates in generics through subsidiaries/portfolio rationalizations.

• Strengths: deep R&D and regulatory experience; strong presence in specialty markets (ophthalmics, dermatology).

Aspen Pharmacare

• Product/overview: South African-headquartered manufacturer focused on generics and finished doses with global export reach.

• Strengths: cost-competitive manufacturing footprint and established tendering relationships in emerging markets.

Dr. Reddy’s Laboratories

• Product/overview: India-based global generics player with diversified portfolio across dosage forms.

• Strengths: API integration, emerging market reach, and experience with complex generics.

Eli Lilly & Co.

• Product/overview: primarily a branded innovator; participates in generics/biosimilar markets via partnerships/spinouts.

• Strengths: deep biopharma expertise and heavy R&D capabilities enabling complex product strategies.

Fresenius SE & Co. KGaA

• Product/overview: specialty in hospital products, infusion therapies and generics used in care settings.

• Strengths: hospital channel integration and strong parenteral/injectable manufacturing know-how.

Hikma Pharmaceuticals

• Product/overview: multinational generics manufacturer with notable injectable and specialty generics.

• Strengths: niche strength in injectables and regulated market experience.

Lupin

• Product/overview: India-based major generics and specialty pharmaceutical company.

• Strengths: strong R&D for complex generics, global distribution, and chronic therapy portfolios.

Mylan N.V. (now part of Viatris in many contexts)

• Product/overview: historic generics powerhouse with broad global reach.

• Strengths: scale manufacturing, deep generics pipeline, strong commercial networks.

Teva Pharmaceuticals Ltd.

• Product/overview: one of the largest global generic drug manufacturers with an extensive portfolio.

• Strengths: unparalleled breadth in molecule coverage, economies of scale, and global distribution.

Latest announcements

Sunshine Biopharma / Nora Pharma — January 2025

• Announcement: Release of two new generic prescription drugs in Canada and plan to launch 20 more in 2025.

• Implication: regional expansion and portfolio build — shows smaller players leveraging niche markets to expand catalogues.

Cosette Pharmaceuticals — Feb 2025 (Mayne Pharma acquisition agreement)

• Announcement: Definitive agreement to acquire Mayne Pharma Group (AUD$7.40/share; ≈USD 430M).

• Implication: consolidation strategy to gain scale, product lines and geographic reach.

Mallinckrodt plc & Endo, Inc. — March 2025

• Announcement: Definitive agreement to combine in stock + cash transaction to create a scaled diversified pharmaceutical player.

• Implication: consolidation to address margin pressure and achieve cost synergies.

Granules India — Dec 2024

• Announcement: Received U.S. FDA approval for Lisdexamfetamine Dimesylate chewable tablets (Vyvanse generic).

• Implication: success in entering ADHD market with multi-strength chewable generics — example of complex oral solid dosage commercialization.

Glenmark Therapeutics (USA) — Aug 2024

• Announcement: Launched Olopatadine Hydrochloride Ophthalmic Solution (OTC) in U.S.

• Implication: OTC launches broaden retail reach and consumer adoption.

API Innovation Center + Apertus Pharmaceuticals — Apr 2024

• Announcement: Collaboration to expand US manufacturing of lomustine (oncology API).

• Implication: strategic moves to reduce import dependence for critical oncology generics.

U.S. CMS — Oct 2024

• Announcement: List of 101 generic meds to be available for $2/month for Medicare (target Jan 2027 availability).

• Implication: major step to make generics ultra-affordable for millions, likely boosting utilization.

India Union Health Minister — Dec 2024

• Announcement: Expansion to 14,000+ PMBJK outlets.

• Implication: large domestic distribution network for affordable generics and a platform for export readiness.

Recent developments

Approvals & launches — Multiple first-time approvals and U.S. launches (e.g., lisdexamfetamine chewable) show active regulatory throughput and commercialization of higher-value generics.

Consolidation activity — Several M&A/combination deals (Cosette/Mayne, Mallinckrodt/Endo) indicate industry consolidation to manage margin pressure.

Supply chain reconfiguration — API manufacture initiatives highlight a push to onshore critical supplies for oncology and other essential generics.

Policy moves — Government programs in India and the U.S. indicate coordinated policy pushes to increase access and reduce patient cost burden.

Retail & OTC expansion — New OTC ophthalmic and chewable formulations demonstrate product diversification into consumer channels.

Segments covered

Therapeutic segmentation (summary)

• Diabetes, cardiovascular, cancer, infectious diseases — chronic disease segments dominate volume due to lifelong therapy needs (e.g., diabetes prevalence projection to 1.3B by 2050 fuels demand).

Route of administration

• Oral: largest share due to convenience, cost-efficiency and high adherence.

• Injections: growing due to bioavailability and hospital use; attracts manufacturers of complex generics.

• Others (topicals, ophthalmic, inhaled): niche but important for specialty launches and OTC transitions.

Distribution channels

• Retail pharmacies: dominant for outpatient chronic therapy; convenience and home delivery expand reach.

• Hospital pharmacies: important for inpatient and injectable markets; require clinical-grade supply chain.

• Online pharmacies: growing channel for chronic refills and subscription models.

Geographic segmentation

• North America: highest revenue concentration; strong payer systems and policy levers.

• Asia-Pacific: manufacturing hub and fastest growth; domestic programs increase local consumption.

• Europe, LATAM, MEA: mix of tendering, price controls, and growing procurement-based opportunities.

Top 5 FAQs

Q: What is the current size and projected size of the global generic drugs market?

• A: The market was USD 487.21 billion in 2024, projected to reach USD 816.75 billion by 2034, growing from USD 513.02 billion in 2025 at a 5.3% CAGR (2025–2034).

Q: Which region currently leads the generic drugs market and which is growing fastest?

• A: North America dominated the market in 2024 in revenue; Asia-Pacific is expected to grow at the fastest rate during the forecast period, driven by manufacturing expansion and domestic policies (e.g., India’s PMBJK).

Q: What are the main drivers of growth for generics to 2034?

• A: Key drivers are patent expiries/off-exclusivity, rising approvals, increased funding for generics R&D/manufacturing, and policy initiatives lowering patient costs.

Q: What are the principal restraints for the generic drugs market?

• A: Market saturation for common molecules leading to price erosion, regulatory compliance costs, and supply-chain concentration risks (API dependencies) are primary restraints.

Q: How will government programs affect access and pricing?

• A: Programs like India’s expansion of PMBJK outlets and the U.S. CMS $2 generic list (101 medications) are designed to broaden access and lower patient out-of-pocket costs—these actions are likely to increase generic utilization and shift market volumes further toward lower-priced generics.

Access our exclusive, data-rich dashboard dedicated to the therapeutics area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5053

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest