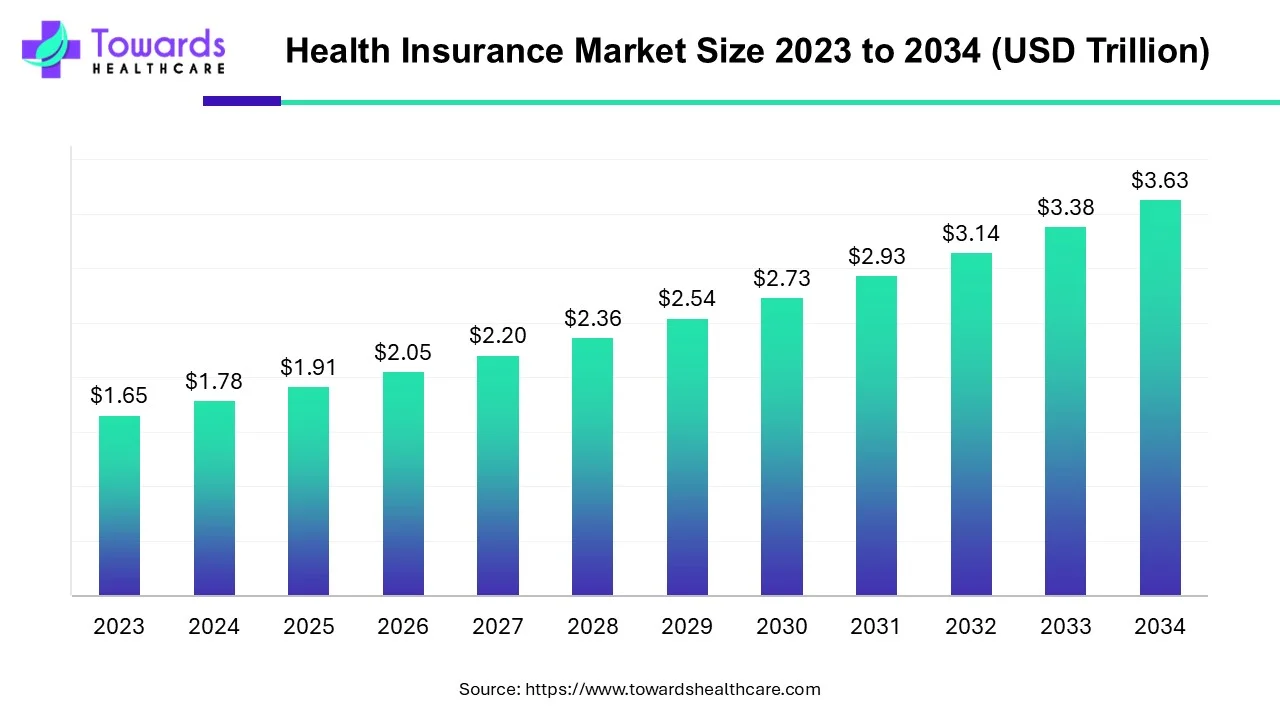

The global health insurance market valued at USD 1.78 trillion in 2024, is expected to grow to USD 3.63 trillion by 2034 (7.4% CAGR), driven by rising healthcare costs, increasing chronic illnesses, and broader uptake of public and private health coverage.

Download Free Sample of Health Insurance Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5085

Market Size

2024 Market Value: USD 1.78 trillion.

2022 Premiums: Total global health insurance premiums reached ~ USD 1.54 trillion — indicating most of the market value flows via premiums and coverage.

2034 Forecast: Market expected to reach USD 3.63 trillion by 2034.

CAGR (2024–2034): Forecast growth rate of 7.4% per year — showing robust long-term expansion.

Underlying Cost Pressure: Rising costs of surgeries, diagnostics, hospital stays, pharmaceuticals globally — increasing demand for insurance coverage to offset high out‑of‑pocket expenses.

Healthcare Spending Growth (example: U.S.): Healthcare spending in the U.S. rose from 8.2% of GDP (1980) to 17.8% in 2021. High and rising per‑person costs (e.g. average ~$13,000/year per American) push insurance uptake.

Large Insured Populations in Developed Markets: For example, in the U.S., ~163 million people (~half the population) are covered via employer-sponsored insurance — demonstrating large baseline demand.

Public Spending in Emerging Economies: Even in low-income countries, governments spending (e.g. ~USD 8 per head) on public health insurance contributes to the global total, indicating public-sector role.

Growing Private Insurance Share: Private insurers are expected to grow fastest due to better services, tech adoption, and customization — signaling increasing market share for private health insurance.

Medical Insurance (Core) as Dominant Segment: Among plan types, core medical insurance (hospitalization, surgery, outpatient) remains the backbone of the market — driven by high cost and necessity of these services.

Market Trends

Rising Medical Costs Driving Demand

As hospital stays, surgeries, diagnostics, and treatments become more expensive globally, individuals and families lean on insurance to avoid catastrophic out-of-pocket expenses.

Insurance as Financial Risk Mitigation

Insurance becomes a safety net, reducing uncertainty for individuals facing sudden health crises — especially where medical costs are unpredictable and high.

Greater Awareness Post‑Pandemic

The COVID-19 pandemic significantly improved global awareness about the importance of health insurance, preventive care, and medical coverage — accelerating market growth.

Public and Private Mix Expanding

Governments in many countries (especially low- and middle-income) are expanding public health insurance or subsidies; simultaneously, private insurers are offering tailored plans — broadening overall coverage.

Customization and Product Innovation

Insurance products are evolving — more flexible, tailored, long-term coverage, combined benefits (e.g. wellness, preventive, critical illness, chronic disease management) rather than one-size-fits-all.

Technological Integration & Digitalization

Insurers increasingly adopt digital solutions — mobile apps for enrollment/payment, online claim filing, telemedicine — making purchasing and using insurance easier.

Rise of InsurTech & Funding for Innovation

Start-ups and tech-enabled insurers (InsurTechs) are attracting funding (VCs or public), especially where conventional insurance penetration was low — leading to new business models and reach.

Preventive & Wellness Focus

Insurance is shifting from just covering illness to encouraging wellness — preventive screenings, regular checkups, chronic-disease management, incentivised healthy behavior.

Regulatory Support & Universal Coverage Push

In many regions, governments are pushing universal health coverage goals — triggering regulatory support, public schemes, social equity orientation — expanding the market’s public component.

Competitive Dynamics & Partnerships

Insurers are forming partnerships, acquisitions, and leveraging collaborations with health-tech firms, employers, and platforms — resulting in innovative distribution channels and improved customer value.

Roles / Impacts of AI on the Health Insurance Market

AI‑Powered Risk Assessment & Underwriting

Machine learning can analyze large datasets (medical history, demographics, lifestyle) to more accurately assess risk and set premiums.

This reduces adverse selection and allows insurers to price more fairly, even for people with chronic diseases or higher risk — expanding inclusion.

Predictive Analytics for Health Trends

AI can predict population health trends (e.g. rising chronic illnesses, seasonal outbreaks), enabling insurers to design proactive coverage, preventive care packages, and dynamic pricing strategies.

Fraud Detection and Claim Validation

AI / NLP algorithms can detect unusual claim patterns, alert for potential fraud, and validate claims faster — reducing administrative losses and enabling lower premiums or better services.

Automated Claims Processing & Faster Settlements

Using AI chatbots, OCR, automated workflows — claim filings, verification, approval — all can be faster and more accurate. This improves customer experience significantly.

Personalized Insurance Products

Based on user data and predictive modeling, insurers can tailor policies (e.g. wellness-based, lifestyle-based, disease-risk-based), rather than one-size-fits-all — catering to diverse consumer needs.

Dynamic Premium Pricing

With continuous data (health metrics, lifestyle, wearable data), premiums could be dynamically adjusted (e.g. lower for healthy lifestyle), rewarding preventive behavior — incentivizing wellness.

Telemedicine + AI Diagnostics Integration

Insurers can partner with telemedicine platforms; AI-driven diagnostics could enable early detection and remote consultations — reducing cost and expanding access, especially in remote regions.

Improved Customer Service via Virtual Assistants / Chatbots

AI chatbots can handle policy queries, claim status, renewals, FAQs — giving 24/7 support, reducing customer service load, and improving user satisfaction.

Risk Pool Optimization and Segmentation

AI can help insurers segment customers (by age, risk, lifestyle, geography) and manage risk pools better — balancing high-risk vs low-risk clients, preventing skewed losses.

Operational Efficiency & Cost Reduction

Administrative tasks, paperwork, documentation, data entry — AI can automate these, reducing overhead for insurers; savings can be passed to customers in lower premiums or better coverage.

These AI and tech roles together can transform health insurance from reactive (only when you’re sick) to proactive, personalized, and more accessible — accelerating global market growth and inclusion.

Regional Insights

🌍 North America

High Healthcare Costs = High Insurance Penetration: With average per-person spending as high as ~USD 13,000/year in the U.S., insurance is almost essential.

Large Employer-Sponsored Base: ~163 million Americans are covered via employer-based health insurance — showing employer-sponsored insurance underpins large share of coverage.

Mature Private Insurance Market: Well-established private insurers offering a variety of plans (HMO, PPO, POS, etc.) with high customer awareness.

Chronic Disease Prevalence & Aging Population: ~60% Americans reportedly have at least one chronic disease — driving demand for comprehensive lifetime medical coverage.

Regulatory and Plan Variety: The market supports managed-care plans like HMOs, PPOs, POS — giving choice and flexibility to consumers.

🌏 Asia-Pacific

Fastest Growth Potential: Rapid urbanization, rising disposable incomes, improving healthcare infrastructure, and increasing chronic diseases (diabetes, obesity) — all boost demand.

Low Historical Penetration + Rising Awareness: Many populations uninsured or underinsured — increasing awareness post‑COVID & growing middle class is expanding coverage uptake.

Public + Private Mix Growing: Governments gradually pushing universal health coverage, combined with private insurers offering tailored plans — bridging the coverage gap.

InsurTech & Digital Reach: Mobile penetration + internet access enable app-based insurance products, remote enrollment, ease of premium payment — great scope for digital-first insurers.

🇪🇺 Europe

Aging Population & Senior Coverage Demand Rising: Growing share of seniors increases demand for health insurance (especially chronic condition and long-term care).

Regulatory Influence & Socialization: Many European nations have strong public healthcare frameworks — insurance often supplements public coverage (for advanced treatments, private care, etc.).

Technology & Coverage Innovation: Insurers may innovate by offering add-ons such as private hospital access, elective procedures, better patient comfort — appealing to affluent segments.

🌐 Emerging Markets / Low‑Income Countries

Public Health Schemes as Entry Point: Small per-capita public spending (e.g. ~USD 8/person) already begins to provide baseline coverage.

Huge Untapped Potential: Low insurance penetration + rising disease burden + rising awareness = major growth opportunity.

InsurTech & Mobile-First Distribution: Mobile phones and internet allow reaching remote, rural populations — enabling micro‑insurance, low-premium plans, and easier administration.

Market Dynamics

Cost Pressure vs. Affordability Tension

Rising medical costs increase demand — but also risk making premiums unaffordable, especially in low/middle-income regions. Insurers must balance coverage breadth and premium cost, which may lead to product segmentation (basic, premium, wellness‑added plans).

Public vs. Private Insurer Balance

Public insurers (government schemes) dominate in many regions due to social equity — but private insurers grow faster due to better service, customization, flexibility. This duality shapes coverage patterns.

Regulatory & Social Equity Influence

Governments’ push for universal health coverage influences public-sector market share and regulatory frameworks (e.g. minimum coverage requirements, mandatory public-private cooperation).

Innovation & Technology as Competitive Differentiator

InsurTech adoption, AI, mobile apps, remote claim processing — insurers embracing technology have stronger competitive advantage, especially in markets with digital penetration.

Product Diversification & Customization

Insurers increasingly offer varied products — lifetime coverage, term insurance, critical illness coverage, wellness plans, network‑based plans (PPO/HMO/POS), and tiered coverage (platinum, gold, silver, bronze, catastrophic) — to serve different customer segments.

Distribution Channel Variation

Direct sales, brokers/agents, banks, online platforms — multiple distribution channels increase market reach. Digital channels especially important for scalability and cost efficiency.

Network Models & Provider Partnerships

Insurers negotiate with hospitals/ providers (PPOs, HMOs, POS) to set fee schedules, manage costs — creating networks that offer discounted services while controlling cost inflation.

Risk Pool Management & Demographics

Aging populations, chronic disease prevalence increase risk. Insurers must manage risk pools carefully — segment by age, health status, geography — to avoid excessive losses.

Competitive Landscape & Consolidation

With many players (public + private), competition pushes for mergers, partnerships, acquisitions — leading to consolidation but also innovation and broader product portfolios.

Consumer Awareness & Education Impact

Awareness (or lack thereof) significantly affects penetration rates. Insurance uptake grows where people understand benefits; lack of knowledge restrains demand — reinforcing the need for education, transparent communication.

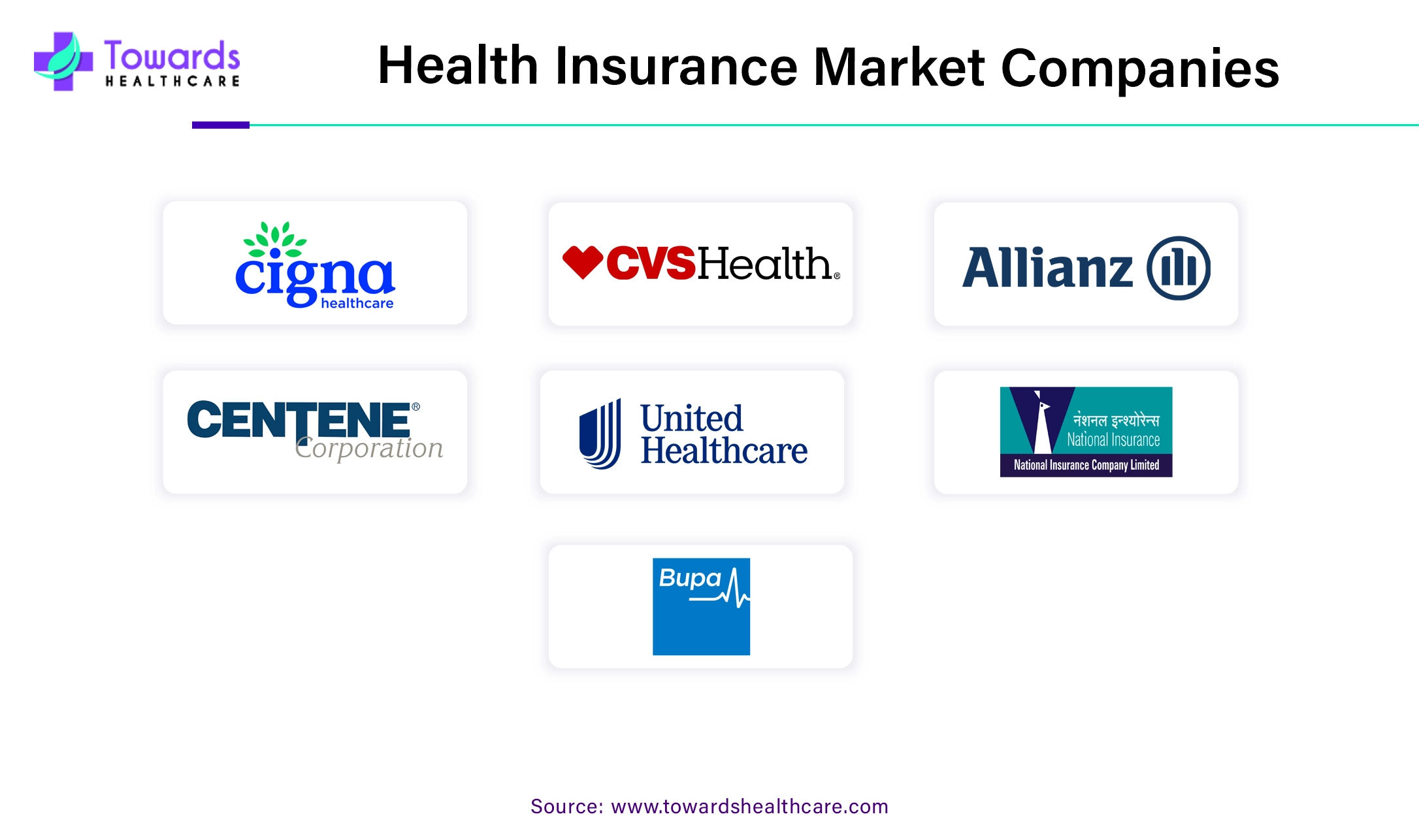

Top 10 Companies in Global Health Insurance Market

Cigna Corporation

Products / Offerings: Global health insurance plans, employer & individual coverage.

Overview & Strengths: Strong international presence; diversified offerings; able to cover expats and multinational clients effectively.

CVS Health Corporation

Products / Offerings: Health insurance via its insurance arm; integration with pharmacy and care services.

Overview & Strengths: Vertical integration combining insurance, pharmacy, and care; provides cost efficiencies and holistic patient experience.

Allianz

Products / Offerings: International health insurance, private medical insurance, expatriate plans.

Overview & Strengths: Wide global footprint, strong financial stability; trusted brand, appealing to travelers and globally mobile individuals.

Centene Corporation

Products / Offerings: Managed care, public-sector insurance programs, Medicaid-type offerings.

Overview & Strengths: Focuses on public and underserved populations; strong in government-linked plans and low-income / high-need segments.

UnitedHealthcare Services, Inc.

Products / Offerings: Comprehensive health insurance; PPO, HMO, POS plans; employer and individual coverage.

Overview & Strengths: Large provider network, flexible plan options; scale advantage with strong customer base.

National Insurance Company Limited

Products / Offerings: Health insurance and general insurance services in specific regions.

Overview & Strengths: Regional knowledge; tailored plans for local markets; trusted within its operating regions.

Bupa Global

Products / Offerings: International health insurance, private medical coverage, expatriate plans.

Overview & Strengths: Focus on premium private care; strong international reach; preferred by individuals seeking high-quality global coverage.

Humana, Inc.

Products / Offerings: Health insurance plans; HMO/PPO options; Medicare/Medicaid plans in the U.S.

Overview & Strengths: Expertise in senior citizen coverage and government-sponsored plans; strong in managed care sector.

AIA Group Limited

Products / Offerings: Health and life insurance; private medical insurance; critical illness and supplementary health coverage (primarily Asia-Pacific).

Overview & Strengths: Strong regional presence in Asia-Pacific; able to serve rising middle-class demand with customized solutions.

Life Insurance Corporation of India (LIC)

Products / Offerings: Recently expanding into health insurance through acquisition of independent health insurer.

Overview & Strengths: Legacy insurer with large customer base and deep brand trust; poised to capture significant share in India’s growing health insurance market.

Latest Announcements & Recent Developments

Star Health and Allied Insurance Company Limited + Policybazaar (Sept 2024): Launched “SUPER STAR”, a personalized long-term health insurance plan — signifying push toward consumer-centric and flexible health coverage.

Care Health Insurance (Jan 2025): Launched “Ultimate Care”, a modern health insurance product combining extensive emergency coverage and rewards for healthy behavior — highlighting trend toward wellness‑linked and value-added plans.

Prudential plc (Mar 2025): Announced joint venture with Vama Sundari Investments Private Limited (an HCL‑Group promoter) to operate a standalone Indian health insurance business — indicating growing foreign/international interest in Indian health insurance market.

Galaxy Health (2025 plan): Announced ambition to become significant player in Indian health insurance; aims to launch at least one product per month, leveraging technology to improve customer service and efficiency — shows aggressive market entry strategies.

MyBenefits + Metropolitan Life (Nov 2024): Collaboration to provide direct access to health insurance packages to employees via MyBenefits platform — illustrating corporate‑benefits distribution growth.

Life Insurance Corporation of India (LIC) (Nov 2024): Acquisition of an independent health insurance firm, with expectation to fully enter health insurance business by 2025 — marking a strategic expansion by a legacy insurer into a growing segment.

Implication: These developments show a global and regional momentum: insurers expanding product lines, wellness-based plans, digital distribution, foreign investment in emerging markets (especially India), and legacy insurers diversifying into health coverage.

Market Segments Covered

By Provider

Public: Government-funded or social insurance schemes. Strength: reaches broad population including low-income groups; contributes to social equity.

Private: Private insurers/companies offering health coverage — growing fastest due to better services, flexibility, customization.

By Coverage Type

Lifetime Coverage: Policy can be renewed for life without re-qualifying — offers long-term security, especially for chronic illness or lifelong healthcare needs.

Term Insurance: Coverage for a fixed period — more affordable, often used by younger or low-risk individuals, or for temporary protection.

By Network Provider (Care Delivery Model)

Preferred Provider Organization (PPO): Network-based; insured use negotiated network for lower cost; out-of-network allowed at higher cost.

Point-of-Service (POS): Hybrid model mixing aspects of HMO and PPO (you may need referrals but sometimes allowed out-of-network) — combining flexibility and managed care.

Exclusive Provider Organization (EPO): (mentioned in list) — network-based, but typically no out-of-network coverage.

Health Maintenance Organization (HMO): Prepaid network care; emphasis on preventive & managed care; lower premiums but less flexibility.

By Plan Type

Medical Insurance (Core Health Insurance): Covers hospitalizations, surgeries, diagnostics, treatments — largest and most fundamental segment.

Critical Illness Insurance: For major illnesses; adds specialized coverage when high-cost diseases hit.

Family / Foster Health Insurance / Others: Plans designed for families, children, special care, supplemental coverage (e.g. maternity, wellness, preventive) — targeting broader demographics.

By Level of Plan Coverage (Tier / Benefit Level)

Platinum, Gold, Silver, Bronze, Catastrophic: Tiered benefit plans — higher tiers offering more comprehensive coverage, lower tiers more affordable/basic coverage. This segmentation helps insurers cater to different income segments and risk appetites.

By Age Group

Minor (Children), Adults, Senior Citizens: Age-based segmentation — different risk, needs, and pricing. Seniors may need more coverage (chronic illness, hospitalization), while children plans may focus on preventive and pediatric care.

By Distribution Channel

Direct Sales (through insurer), Brokers / Agents, Banks, Others (e.g. digital platforms, employer benefits) — multiple channels help reach diverse customers. Digital/online channels increasingly important for scale and convenience.

By Geography

Regions: North America, Europe, Asia-Pacific, Latin America, Middle East & Africa — segmentation by geography helps account for differences in income levels, healthcare infrastructure, regulatory environment, population demographics, disease burden, and insurance penetration.

This segmentation framework allows insurers to design tailored products — for example, a “Silver” plan for young adults in Asia-Pacific, or a “Gold/PPO” plan for expatriates in Europe — optimizing coverage, risk, and affordability.

Top 5 FAQs (With Answers Using Provided Data)

Q1. What is the current size and growth forecast of the global health insurance market?

A1. The global health insurance market was valued at USD 1.78 trillion in 2024, and is expected to grow to USD 3.63 trillion by 2034, representing a 7.4% CAGR over the period.

Q2. What factors are driving this growth?

A2. Key drivers include rising costs of medical services (hospitalization, surgeries, diagnostics), growing prevalence of chronic diseases and aging populations, increased healthcare spending globally, rising awareness post-COVID, and greater penetration of both public and private insurance coverage.

Q3. How does the market split between public and private insurance providers?

A3. While public insurers (government‑funded schemes) hold a large share — especially in low- and middle-income countries — the private segment is projected to grow the fastest, driven by enhanced services, technology adoption, and customized offerings.

Q4. What are the different types of health insurance plans globally?

A4. Plans vary by coverage type (lifetime vs term), care-delivery model (PPO, HMO, POS, EPO), plan benefit levels (platinum, gold, silver, bronze, catastrophic), age-group targeted (minor, adult, senior), and by plan type (core medical, critical illness, family/foster, etc.).

Q5. How is technology (particularly AI) influencing the health insurance market?

A5. AI and related technologies are transforming underwriting and risk assessment, enabling predictive health analytics, automating claims, enabling personalized and dynamic pricing, improving customer service through chatbots, detecting fraud, and overall increasing operational efficiency — which can reduce costs, improve coverage, and accelerate market growth globally.

Access our exclusive, data-rich dashboard dedicated to the healthcare services sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Health Insurance Market Report Now at: https://www.towardshealthcare.com/checkout/5085

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest