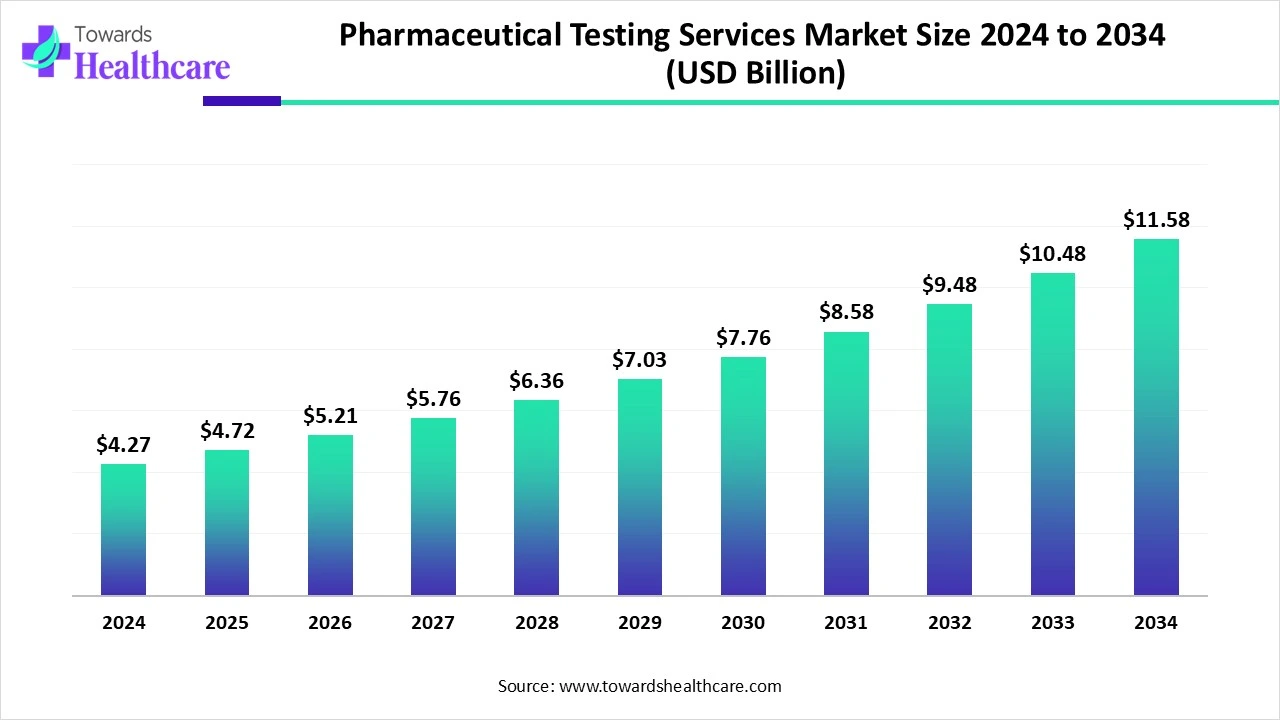

The global pharmaceutical testing services market reached US$ 4.27 billion in 2024, is expected to grow to US$ 4.72 billion in 2025, and is projected to hit US$ 11.58 billion by 2034 at a strong CAGR of 10.54%, driven by rising biologics demand, AI-integrated analytical testing, and expanding R&D pipelines.

Download Free Sample of Pharmaceutical Testing Services Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5937

Market Size (2024–2034)

1. Strong Baseline Market Expansion

Market size in 2024: US$ 4.27 billion

Market size in 2025: US$ 4.72 billion

Indicates a 10.5% YoY rise, reflecting growing outsourcing and demand for precision testing.

2. Long-Term Growth Projection

Projected to reach US$ 11.58 billion by 2034, more than 2.4x growth in 10 years.

Steady, predictable expansion showing strong structural industry demand.

3. CAGR of 10.54% (2025–2034)

Higher than average pharmaceutical sector CAGR (~5–7% globally).

Shows testing is one of the fastest-growing sub-sectors in pharma.

4. Clinical Testing Share Leadership

Clinical phase testing held 35–38% share in 2024, showing most revenue stems from drug trials.

5. Dominance of Small Molecules

Small molecules held 60–65% share in 2024, reaffirming their continued dominance in drug pipelines.

6. Analytical Testing Commanding Penetration

Analytical testing services captured 18–20% share in 2024, the largest among services.

7. Larger Opportunity Space in Large Molecules

Large molecule testing expected to grow fastest due to monoclonal antibodies, vaccines, and biosimilars.

8. Rising Share of Biopharma End-Users

Biopharmaceutical companies expected to show highest CAGR among end-use categories.

9. Asia-Pacific Fastest Growing Region

APAC highlighted as fastest-growing region from 2025–2034 due to rapid clinical trial expansion.

10. North America Leading Revenue

Held 38–40% global share in 2024, driven by FDA regulatory requirements and CRO strength.

Market Trends

1. Rapid Adoption of AI & Automation

AI used for clinical trial optimization, early failure prediction, automated documentation, and dataset analysis.

AI reduces testing time and cost across chemical and biological testing.

2. Growth of Biologics & Biosimilars

High demand for monoclonal antibodies, vaccines, gene therapies → boosts need for advanced bioanalytical testing.

3. Integration of Digital Tools (LIMS, analytics platforms)

LIMS improves data integrity, regulatory compliance, and workflow automation.

4. Rising Outsourcing to CROs

Companies outsource due to cost efficiency, lack of in-house expertise, and stringent FDA/EMA standards.

5. Increasing Regulatory Stringency

FDA, EMA, NMPA reforms require more method validation, stability testing, sterility testing.

6. Growing Phase III Clinical Trials

Phase III dominated 2024 due to the need for large-scale efficacy and safety testing.

7. Expansion of Specialized Testing Capabilities

Includes:

Extractables & leachables

Endotoxin and sterility testing

Biomarker analysis

Genomic testing partnerships

8. Rising Investments in Advanced Labs

Examples from provided data:

LGM Pharma expanded ATS with sterility capabilities

Nelson Labs launched rapid sterility testing

9. Geographic Expansion in APAC

APAC becoming a global hub for bioanalytical, sterility, and clinical testing with major partnerships.

10. M&A and Strategic Alliances Rising

NAMSA acquiring WuXi operations

Centivax alliance with Emery Pharma

Frontage–Medicover genomic partnership

Impact / Role in Pharmaceutical Testing Services

1. AI-Driven Clinical Trial Optimization

Uses patient stratification, predictive modeling, and protocol simulation.

2. Automated Data Entry & Documentation

AI minimizes human error and accelerates electronic lab notebook (ELN) workflows.

3. AI-Enhanced Quality Control

Algorithms detect abnormalities, impurities, stability issues, and deviations in real-time.

4. Predictive Failure Detection

AI identifies potential batch failures before they occur, saving cost and materials.

5. Accelerated Analytical Data Processing

AI models analyze LC-MS, GC-MS, NGS outputs faster than manual interpretation.

6. Biomarker Identification & Validation

Machine learning analyses omics datasets to identify disease-specific biomarkers.

7. Automated Image and Microscopy Analysis

AI accelerates cell-based assays, microbial identification, and material defect detection.

8. Real-Time Monitoring of Stability Studies

AI detects early degradation patterns and environmental fluctuations.

9. Faster Regulatory Report Generation

AI automates compliance documentation (FDA, EMA, ICH), reducing cycle time.

10. Enhanced Patient Recruitment Modeling

AI identifies ideal patient populations, improving bioanalytical and PK/PD study efficiency.

Regional Insights

A. North America (Largest Market – 38–40% Share)

1. Strong FDA Compliance Pressure

Drives increased outsourcing for complex method validation, sterility, and analytical testing.

2. Technologically Advanced CRO Ecosystem

Home to Labcorp, Charles River, Pace Analytical, ICON, etc.

3. High Demand for Biologics Testing

Due to heavy investment in oncology, vaccines, and autoimmune therapies.

4. Strategic Acquisitions

NAMSA acquired WuXi AppTec’s U.S. operations → strengthens medtech testing.

B. Asia Pacific (Fastest Growing Region)

1. Massive Clinical Trial Expansion

APAC is a cost-effective destination for Phase I–III trials.

2. Strategic Partnerships

LabConnect + Australian Clinical Labs

Gene Solutions + ZaoDx + MagicBiotech (China)

3. Strong Government Support

India (Agilent biopharma capability center)

China (NMPA reforms aligned with ICH)

4. Growth of Sterility and Bioanalytical Testing

APAC becoming a hub for biologics QC and stability testing.

C. Europe (High Outsourcing, Technological Advancement)

1. Strong Biologics Development Hub

Germany, UK, Switzerland lead in monoclonal antibodies & next-gen therapies.

2. AI & Robotic Testing Initiatives

UK uses robotic technology for genomic cancer testing.

3. Major Pharma Investments

BMS + BioNTech partnership (Germany) for next-gen immunotherapy.

D. Latin America and MEA (Emerging Markets)

1. Growing investment in sterile pharma testing

2. Increasing dependency on global CRO partnerships

Market Dynamics

Drivers

1. Rising R&D Investments

Large pharma & biopharma investing to accelerate drug discovery & clinical trials.

2. Increasing Demand for Biologics

Need for complex bioanalytical testing including LC-MS, GC-MS, immunoassays.

3. Growth of Biosimilars & Gene Therapies

Requires extremely detailed analytical characterization.

Restraints

1. High Cost of cGMP Facilities

Requires heavy investment in compliant labs, automation, and high-end equipment.

2. Regulatory Strictness

FDA, EMA, NMPA impose intense stability, sterility, and method validation requirements.

Opportunities

1. Specialized Testing Services

Extractables/leachables

Biomarker testing

Cell-based assays

Material characterization

2. Digitalization Boom

LIMS, AI, ML, automated reporting

Massive demand for data integrity & regulatory documentation

Top 10 Companies

1. Eurofins Scientific

Products/Services: Analytical testing, microbiology, bioanalytical, GMP testing.

Strengths: Largest lab network globally; strong regulatory credibility.

2. SGS SA

Products: Bioanalytical services, stability testing, GMP lab services.

Strengths: Global presence, recognized for quality assurance & compliance.

3. Charles River Laboratories

Products: Preclinical testing, toxicology, microbial testing.

Strengths: Leader in early-stage drug testing.

4. Labcorp Drug Development

Products: Clinical trial testing, PK/PD testing.

Strengths: Large patient database; strong Phase I–III capabilities.

5. Thermo Fisher Scientific

Products: Analytical instruments, bioanalytical testing services.

Strengths: Strong technology base and AI-ready platforms.

6. WuXi AppTec

Products: Analytical chemistry, material characterization, biologics testing.

Strengths: End-to-end pharmaceutical development ecosystem.

7. Intertek Group

Products: GMP testing, stability studies, sterility testing.

Strengths: Strong regulatory compliance expertise.

8. PPD Inc.

Products: Bioanalytical testing, clinical trial services.

Strengths: Part of Thermo Fisher; global CRO presence.

9. Pace Analytical Services

Products: Material testing, elemental impurities, microbiology.

Strengths: Strong chemical and environmental testing integration.

10. BioAgilytix Labs

Products: Large molecule bioanalysis for biologics & cell/gene therapies.

Strengths: Excellence in LC-MS/MS and immunoassays.

Latest Announcements

1. Centivax + Emery Pharma (March 2025)

Strategic alliance for universal vaccine readiness.

Enhances GLP/cGMP bioanalytical testing capabilities.

2. LGM Pharma Expansion (October 2024)

Added endotoxin & sterility testing capabilities.

Strengthens ATS for small & large molecule customers.

Recent Developments

1. DDL Launches New GMP Lab (April 2025)

Supports pharmaceutical, biotech, and combination product testing.

2. Nelson Labs Introduces Rapid Sterility Test (March 2025)

Reduces sterility testing time dramatically → faster product releases.

3. SGS Introduces New Bioanalytical Services (August 2024)

Expands presence in North America’s biologics market.

Segments Covered

1. Service Type

a. Analytical Testing Services

Analytical testing forms the backbone of pharmaceutical quality control and regulatory compliance. Key offerings include:

Method Development & Validation:

Establishes accurate, reproducible testing methods for identifying and quantifying active ingredients and impurities. Validation ensures reliability across labs and batches.

Stability Testing:

Determines how environmental conditions (temperature, humidity, light) affect drug potency and shelf life. Essential for finalizing product expiry dates.

Dissolution Testing:

Measures how quickly and efficiently a drug dissolves in the body. Critical for oral solid dosage forms like tablets and capsules.

Why it matters:

Analytical testing ensures the safety, identity, purity, and potency of drug substances and finished products, making it one of the most heavily regulated and outsourced services in the industry.

b. Bioanalytical Testing Services

Bioanalytical testing supports both drug discovery and clinical development. Major components include:

Pharmacokinetics (PK) & Pharmacodynamics (PD):

PK explains how the drug moves through the body (absorption, distribution, metabolism, excretion).

PD explains how the drug affects the body (mechanism, effect, toxicity).

BA/BE Studies (Bioavailability/Bioequivalence):

Required for generics to prove equivalence to the innovator drug. Essential for ANDA approvals.

Biomarker Analysis:

Increasingly important for personalized medicine and biologics.

Why it matters:

Bioanalytical testing is critical for clinical trials, regulatory submissions, and the expanding biologics & biosimilars market.

c. Microbiology Testing

Microbial testing ensures that products are free from harmful contamination. Key areas:

Sterility Testing:

Mandatory for injectables, ophthalmic solutions, and implants.

Endotoxin Testing:

Detects pyrogens (toxins released from bacteria) that can cause dangerous fevers or shock.

Microbial Limits Testing:

Ensures the number of microorganisms in a sample stays within regulatory permissible limits.

Why it matters:

Microbiology testing ensures product safety, especially in sterile and high-risk formulations.

d. Material Characterization

Material characterization focuses on packaging components, container systems, and delivery devices. Services include:

Extractables & Leachables (E&L):

Identifies chemicals that may migrate from packaging into drug products, especially in biologics and inhalation drugs.

Particulate Matter Analysis:

Detects visible and sub-visible particles that can affect injectables’ safety.

Container Closure Integrity (CCI):

Confirms that packaging prevents contamination and maintains sterility throughout shelf life.

Why it matters:

Crucial for packaging validation, especially for injectables, vaccines, biologics, and advanced therapies.

e. Physical Testing

Covers the physicochemical properties of drug substances and formulations:

Residual Solvent Testing:

Ensures harmful solvents used during manufacturing are removed to safe levels.

Preservative Efficacy Testing (PET):

Confirms preservatives effectively prevent microbial growth.

Other tests include:

pH, viscosity, melting point, moisture content.

Why it matters:

Physical testing ensures chemical stability, formulation integrity, and patient safety.

2. Molecule Type

a. Small Molecules

Represent the largest share of the drug pipeline due to historical dominance.

Common in generic drugs, anti-infectives, cardiovascular drugs, and CNS therapies.

Require extensive analytical, dissolution, and stability testing.

b. Large Molecules (Biologics)

Fastest-growing segment, driven by monoclonal antibodies, vaccines, cell & gene therapies, and biosimilars.

Require advanced bioanalytical, microbiology, and E&L testing due to structural complexity.

Trend:

Shift toward biologics is accelerating demand for specialized testing services worldwide.

3. Phase

a. Preclinical Phase

Includes:

Toxicology studies

Method development

Early stability studies

Animal PK/PD analysis

Focus: safety, dose selection, and regulatory approval for first-in-human trials.

b. Clinical Phase (Phase I–III)

This segment holds the largest share due to extensive testing requirements:

PK/PD profiling

BA/BE studies

Biomarker and immunogenicity testing

Batch release and stability for trial materials

Reason: Clinical development demands continuous, large-scale testing in human trials.

c. Manufacturing Phase

After approval, products undergo:

Ongoing stability testing

Quality control testing for every batch

Microbial & sterility checks

Release testing for global distribution

Importance: Ensures compliance throughout the product lifecycle.

4. End-Use Segments

a. Pharmaceutical Companies (Largest Share)

Major users of analytical, microbiology, and physical testing.

Outsourcing preferred for cost-efficiency and regulatory compliance.

b. Biopharmaceutical Companies (Fastest Growing)

Increased demand due to biologics, biosimilars, and advanced therapies.

Require highly specialized testing like bioassays, E&L, immunogenicity testing.

c. Contract Research Organizations (CROs)

Provide full-scale drug development support.

Integrate analytical and bioanalytical services for clinical trials.

d. Research Institutions

Involved in early-stage drug discovery.

Require testing for academic research, early validation, and translational studies.

5. Region Analysis

a. North America

Largest market due to strong biopharma industry.

High regulatory standards (FDA) fuel specialized testing demand.

b. Europe

Strong biotech ecosystem, especially in Germany, UK, Switzerland.

Strict EMA guidelines drive outsourcing to testing service providers.

c. Asia Pacific (Fastest Growing)

Rapid expansion due to India, China, Japan, and South Korea.

Cost advantages + growing CRO industry = high outsourcing demand.

d. Latin America

Emerging market for generics and local manufacturing.

Increasing regulatory harmonization boosting demand for QC testing.

e. Middle East & Africa (MEA)

Gradually growing due to government efforts to expand local pharma production.

Reliance on imports still high, but testing capacity improving.

Top 5 FAQs

1. What is the current size of the pharmaceutical testing services market?

The market is US$ 4.27 billion in 2024, expected to reach US$ 11.58 billion by 2034 at a CAGR of 10.54%.

2. Which region leads the market?

North America dominates with 38–40% share due to strong regulatory oversight and advanced CROs.

3. Which segment is growing the fastest?

Bioanalytical testing services (service type)

Large molecules (molecule type)

Phase I testing (clinical sub-phase)

4. What is driving market growth?

Rising R&D investment, high demand for biologics, AI adoption, and the expansion of clinical trials.

5. Who are the top players?

Eurofins Scientific, SGS, Charles River, Labcorp, Thermo Fisher, WuXi AppTec, Intertek, PPD, Pace Analytical, BioAgilytix.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Pharmaceutical Testing Services Market Report Now at: https://www.towardshealthcare.com/checkout/5937

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest