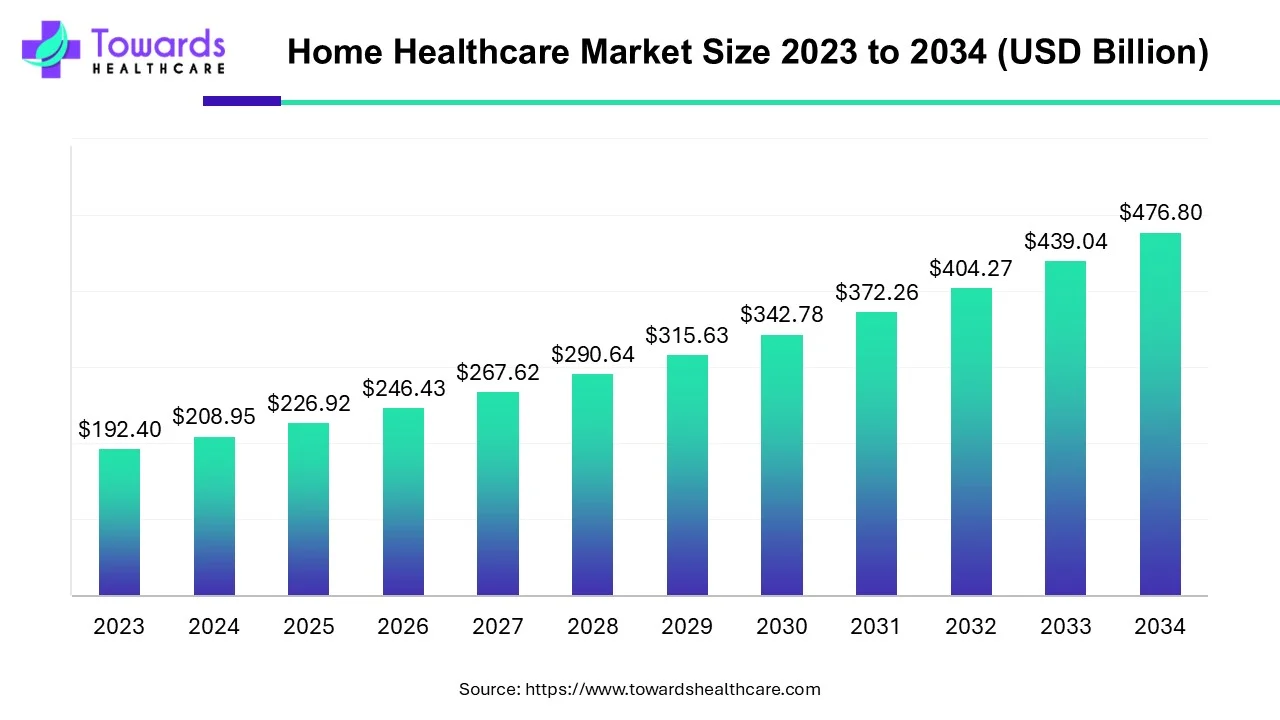

The global home healthcare market is growing rapidly, from USD 208.95 billion in 2024 (USD 226.92 B in 2025) and is forecast to reach USD 476.80 billion by 2034 at a CAGR of 8.6% (2025–2034), driven by diagnostics & monitoring devices (59% share in 2023), the diabetes indication (32% share in 2023), and North America’s regional leadership.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5110

Market size

Current baseline years

●2024 market size: USD 208.95 billion (reported).

●2025 estimate (start of forecast): USD 226.92 billion (report’s baseline for CAGR calculation).

Forecast endpoint

●2034 projected market size: USD 476.80 billion — more than double 2025, reflecting sustained growth.

Growth rate

●CAGR (2025–2034): 8.6%, implying market doubling roughly every 8–9 years.

Structural drivers of size (summary)

●Device-led value: diagnostics & monitoring devices dominated (59% share in 2023), so a large portion of dollar growth comes from device miniaturization, wearables, and supplies.

●Chronic-care tailwinds: diabetes (32% share in 2023) plus cardiovascular and respiratory needs underpin recurring revenue (consumables, monitoring subscriptions, telehealth follow-ups).

●Geography bootstrapping: North America as the largest regional market (44% share in 2023; ~USD 75–76B in 2024) provides disproportionate revenue and investment.

Yearly regional dollar context

●North America: USD 75.73 B

●Europe: USD 52.03 B

●Asia-Pacific: USD 55.77 B

●Latin America: USD 13.07 B

●Middle East & Africa: USD 12.36 B

Sector composition (monetary tilt)

●Medical supplies, diagnostics/monitoring and therapeutics devices are the three cash pools; medical supplies and monitoring/diagnostics are major, recurring revenue sources (see device-type table numbers).

Market Trends

Device-led adoption (Diagnostics & Monitoring dominance)

●Diagnostics & monitoring devices held 59% market share in 2023; they drive both unit volume (consumer wearables) and high-margin clinical devices for home use.

●Trend: migration of hospital-grade monitoring to compact, connected consumer devices.

Diabetes as a growth anchor

●Diabetes accounted for 32% of the market in 2023. Rising diabetes prevalence (CDC data cited) fuels demand for glucose monitors, insulin delivery and remote coaching.

Aging population / “age-in-place” preference

●Older adults’ preference to remain at home is expanding demand for nursing, therapy, mobility aids and chronic-care monitoring.

Telehealth & remote care integration

●Telemedicine is mainstreamed into home healthcare for consultations, monitoring and follow-up — enabling centralized care teams to supervise distributed patients.

Investment & startup activity

●Recent financings (e.g., Geneoscopy Series C for at-home colorectal test) and NEC X’s investment in GPx indicate capital flows into home diagnostics and chronic monitoring.

Regulatory approvals enabling wearables

●FDA clearances for multimodal wearable sensors (Cardiosense CardioTag) open clinical pathways for continuous cardiac monitoring outside hospitals.

AI and predictive analytics emergence

●Early implementations (referenced firms like Verily/CarePredict in the brief) point to predictive risk detection for early interventions and resource prioritization.

Supply & consumables monetization

●Medical supplies (consumables) create recurring revenue (dressings, tubing, glucose strips, etc.) and remain a large cash contributor.

Regional investment and public policy facilitation

●Governments and private investors (notably in Asia-Pacific: China, India) are supporting device adoption and affordability, expanding market reach.

Patient/caregiver education as adoption limiter and opportunity

●Limited awareness is a barrier; structured education programs and digital onboarding are increasingly packaged with devices and services.

AI impacts / roles in the home-healthcare market

Continuous signal processing & noise reduction

●Subpoints: AI filters motion artifacts from wearables, fuses multi-modal inputs (ECG + PPG + SCG) and produces clinically usable signals.

●Explanation: This raises the clinical grade of consumer wearables and enables remote clinicians to make decisions from home-collected data (e.g., CardioTag-style multimodal sensors).

Predictive risk scoring and early warning

●Subpoints: Models trained on longitudinal vitals produce early alerts (fall risk, impending decompensation, diabetic foot risk).

●Explanation: Predictive analytics turn continuous streams into actionable alerts, reducing hospitalizations and targeting home visits.

Personalized, adaptive care plans

●Subpoints: AI tailors therapy intensity, rehab exercises, medication reminders and dosing schedules per patient response.

●Explanation: This improves adherence and outcomes — particularly important for diabetes and cardiovascular management.

Automated triage for telehealth workflows

●Subpoints: AI classifies symptom reports and sensor anomalies into urgency tiers, routing to nurse, therapist or emergency services.

●Explanation: Efficiently uses scarce clinical resources and reduces clinician burden.

Image and signal diagnostics at point-of-care

●Subpoints: On-device AI analyzes wound photos, retinal images or sensor waveforms and provides preliminary diagnostics or referral recommendations.

●Explanation: Speeds up detection of complications (e.g., diabetic foot ulcers) and reduces time to intervention.

Medication adherence and optimization

●Subpoints: AI detects adherence patterns, predicts non-adherence causes and proposes interventions (alerts, caregiver escalation).

●Explanation: For chronic indications like diabetes, adherence is crucial — AI can reduce complications and cost.

Operational optimization and capacity planning

●Subpoints: AI forecasts demand for home visits, schedules staff dynamically, and optimizes supply chains for consumables.

●Explanation: Lowers operational costs for home-health providers and aligns inventory with real patient needs.

Natural language clinical documentation

●Subpoints: Automated visit note generation from voice or structured inputs, coding support, and summary generation for care teams.

●Explanation: Reduces administrative overhead and improves data capture consistency.

Remote patient education and coaching (conversational AI)

●Subpoints: Tailored education modules, motivational coaching for lifestyle, and onboarding for device usage, available 24/7.

●Explanation: Fills the “limited awareness” gap and scales caregiver education at low cost.

Regulatory compliance & quality monitoring

●Subpoints: AI monitors device performance, user engagement, and adverse event signals—feeds into post-market surveillance and quality dashboards.

●Explanation: Strengthens safety cases for new home diagnostics and supports claims required for reimbursement or regulatory approval.

Regional insights

A. North America — market leader (44% share in 2023; USD 75.7B in 2024)

Demand drivers

●Aging population, high chronic disease prevalence (diabetes, cardiovascular).

High per-capita spending & rapid reimbursement adoption

●Favorable reimbursement and private pay models accelerate adoption of remote monitoring and telehealth.

Innovation hub

●Strong startup & device ecosystem (FDA pathways enabling wearables like CardioTag).

Integration with hospital systems

●Home care vendors often integrate into hospital discharge and readmission-reduction programs.

B. Europe

Awareness & public-sector investments

●Government programs and private investments expanding access; strong emphasis on evidence and interoperability.

Cross-country fragmentation

●Diverse payer systems mean product rollouts often require local adaptation and clinical validation for different national systems.

C. Asia-Pacific

Rapid volume growth

●Large aging populations (China, India) and growing middle class drive unit demand for affordable devices.

Price sensitivity + scale

●Devices and services must be cost-competitive; government support can accelerate adoption.

Technology leapfrogging

●Mobile-first care models, telemedicine and scalable remote monitoring can expand reach quickly.

D. Latin America & Middle East/Africa

Emerging markets with access gaps

●Greater need for remote solutions due to limited hospital density; affordability and education are key constraints.

Opportunity in low-cost diagnostics

●Portable, low-cost screening devices (e.g., for diabetes complications) can capture unmet needs.

Market dynamics

Drivers

1. Rising Chronic Disease Prevalence (Diabetes as the Core Driver)

Diabetes alone accounts for 32% of chronic device use (2023), making it a key revenue driver for glucose monitors, insulin delivery systems, and continuous monitoring devices.

Growing incidence rates — fueled by aging, sedentary lifestyles, and obesity — are amplifying long-term care needs.

Governments and health systems are pivoting toward value-based care models emphasizing early detection and continuous management, both of which rely on connected diagnostic and monitoring tools.

The integration of AI and wearable sensors further strengthens this segment by enabling real-time intervention and outcome-based reimbursements.

2. Diagnostics & Monitoring Devices Lead Market Share (59% in 2023)

Continuous glucose monitors (CGMs), blood pressure monitors, and cardiac rhythm trackers represent the foundation of chronic care ecosystems.

These devices generate recurring data streams that feed into telehealth and electronic health records (EHRs), creating long-term engagement and subscription-based business models.

The shift from episodic care to continuous, preventive monitoring is attracting both medtech and digital health investors.

Device interconnectivity (IoMT) allows for automated alerts, clinical decision support, and early intervention — lowering hospitalization rates and overall system costs.

3. Aging Population & Desire to “Age in Place”

By 2030, 1 in 6 people globally will be aged 60+, driving up chronic conditions, rehabilitation, and mobility support needs.

The preference to stay at home rather than in institutional care settings is accelerating demand for assistive and home-based care technologies — from mobility aids and smart pill dispensers to remote monitoring tools.

Governments are investing in aging-in-place infrastructure and home-based reimbursement frameworks to reduce hospital burden.

Emotional and psychological benefits of remaining at home add an additional layer of demand for user-friendly, non-clinical looking devices.

Restraints

1. Limited Patient and Caregiver Awareness

Despite technological advances, education gaps persist, particularly in lower-income regions.

Complex setup processes or unclear benefits slow down adoption of newer smart devices or integrated homecare platforms.

Caregivers, who often play a central role in device use, may lack formal training or technical familiarity, reducing efficacy.

Manufacturers and healthcare systems need structured onboarding and engagement programs to bridge this awareness gap.

2. Reimbursement Fragmentation

Reimbursement policies differ by region, payer type, and device class, creating uncertainty for both providers and manufacturers.

Some advanced remote monitoring devices are still categorized as “non-essential”, limiting coverage.

Inconsistent value demonstration metrics across markets delay adoption, especially for AI-driven solutions.

This lack of harmonization slows innovation rollout and discourages smaller startups from entering regulated markets.

3. Technology Acceptance & the Digital Divide

Seniors and underserved populations face barriers due to low digital literacy, affordability issues, or poor internet access.

Even when devices are available, usability issues — small screens, complex interfaces — reduce adherence.

Developers must focus on inclusive design, voice-assist features, and simplified user experiences to expand reach.

The digital divide could exacerbate healthcare inequality if not proactively addressed.

Opportunities

1. AI-Enabled Predictive Care & Subscription Models

Integration of AI allows predictive analytics, detecting health deterioration before symptoms appear.

Companies can monetize this continuous insight via subscription services — offering bundled monitoring, coaching, and data analytics.

This transition from hardware sales to service-driven revenue models increases margins and customer lifetime value.

Healthcare providers benefit from improved patient outcomes and operational efficiency, fostering long-term partnerships with device firms.

2. Consumables and Supplies: A Recurring Revenue Engine

Chronic care devices rely heavily on disposables — test strips, lancets, sensors, infusion sets, electrodes, etc.

These consumables ensure steady, high-margin cash flows, supporting business sustainability.

Supply chain optimization and smart reordering systems (auto-refill via app or device) further enhance user retention.

As device penetration deepens, the aftermarket opportunity will surpass initial device sales in some categories.

3. Expansion into New At-Home Diagnostics

Innovations in colorectal stool tests, neuropathy screening, kidney function, and cardiac biomarkers are reshaping preventive care.

Moving diagnostics from clinics to homes not only reduces cost and time but also broadens the consumer base beyond chronic patients to include wellness-conscious individuals.

Partnerships between biotech firms, digital health startups, and retailers (like CVS, Walgreens) are accelerating commercialization.

These novel tools will extend the chronic care ecosystem into early detection and lifestyle management domains.

Threats

1. Regulatory and Safety Hurdles

Regulatory pathways (FDA, EMA, PMDA) require rigorous validation, safety testing, and post-market surveillance.

Delays in approval can increase time-to-market and development costs.

Adverse events or product recalls can erode consumer trust and lead to brand reputational damage.

New categories (AI-enabled or software-as-a-medical-device) are still facing unclear regulatory frameworks, causing compliance uncertainty.

2. Competition & Margin Pressure

Entry of tech giants (Apple, Google, Samsung) and established medtech players (Medtronic, Abbott, Philips) intensifies competition.

Market saturation in certain device categories drives price erosion and limits differentiation.

Startups often struggle to scale profitably without large distribution networks or partnerships.

As subscription and consumables markets grow, customer retention and ecosystem lock-in will become key differentiators.

3. Data Privacy & Cybersecurity Risks

With billions of patient data points generated daily, healthcare IoT devices are prime targets for cyberattacks.

Breaches can result in loss of trust, patient harm, and legal liabilities under strict privacy laws (HIPAA, GDPR).

Continuous device connectivity demands robust encryption, real-time threat detection, and compliance monitoring.

Lack of standardized cybersecurity protocols in medical devices creates a persistent systemic risk.

Top companies

GE HealthCare

Products: hospital-grade diagnostics, imaging, and monitoring systems adapted for home/remote workflows.

Overview: Large medtech incumbent with broad device portfolio.

Strengths: Product breadth, clinical credibility, ability to integrate with provider IT systems.

Amedisys

Products: home health nursing, hospice, and in-home therapy services.

Overview: Major provider of in-home clinical services.

Strengths: Operational scale in home nursing, payer relationships, care management expertise.

LHC Group

Products: home health, hospice, and personal care services delivered through extensive network.

Overview: Large service provider focused on home-based care delivery.

Strengths: Network scale, capability to operationalize home visits and integrate telehealth.

BAYADA Home Health Care

Products: nursing, therapy, personal care services in home settings.

Overview: Longstanding home care provider.

Strengths: Care continuity, family-centric models, local community footprint.

Koninklijke Philips N.V. (Philips)

Products: telehealth platforms, remote monitoring, sleep and respiratory devices; Philips Virtual Care Management (launched Mar 2023).

Overview: Technology provider bridging devices and care management platforms.

Strengths: Platform + device integration, enterprise deployments, global reach.

ResMed

Products: respiratory devices (CPAP, sleep apnea monitors), connected health solutions.

Overview: Specialist in respiratory care with strong home device penetration.

Strengths: Disease-specific expertise, subscription & device connectivity models.

Becton, Dickinson and Company (BD)

Products: infusion sets, diagnostic kits, recently launched AI hemodynamic platform (April 2025).

Overview: Large medtech/consumables company with strong supply presence.

Strengths: Consumables supply chain, clinical trust, product reliability.

Medline Industries, Inc.

Products: medical supplies and consumables for home and clinical settings.

Overview: Major supplier of medical disposables and supplies.

Strengths: Distribution scale, cost leverage, broad consumable catalogue.

Arkray, Inc.

Products: diabetes diagnostics and blood glucose monitoring solutions.

Overview: Specialist in glucose monitoring technologies.

Strengths: Diabetes focus, device know-how and distribution in multiple markets.

McKesson Medical-Surgical Inc.

Products: supply distribution, home care equipment and logistics support.

Overview: Large distribution and service company for healthcare supplies.

Strengths: Logistics, inventory, ability to serve home-care providers with consumables.

Latest announcements

Cardiosense — CardioTag (July 2025)

Announcement: FDA clearance for CardioTag wearable sensor that captures SCG, high-fidelity ECG and PPG simultaneously — a first multimodal wearable with non-invasive measurement authorization.

Implications: Enables richer physiology capture at home (combines mechanical and electrical cardiac signals) → improved arrhythmia, hemodynamic and perfusion monitoring for remote cardiac care.

Ayati Devices (April 2025)

Announcement: Bengaluru-based startup working on affordable, portable diagnostic tools for early neuropathy detection (diabetic neuropathy).

Implications: Low-cost point-of-care tools can expand screening in India and other price-sensitive markets, reducing downstream complications and hospitalizations.

BD — advanced hemodynamic monitoring platform (April 2025)

Announcement: Launched an AI + predictive algorithm powered hemodynamic monitoring system to detect blood pressure instability and optimize flow.

Implications: Extends advanced monitoring into non-ICU and possibly home settings (post-acute monitoring), improving early intervention for hemodynamic compromise.

Movano Health (April 2025)

Announcement: Positive clinical study results showing accurate blood pressure monitoring at levels consistent with regulatory standards.

Implications: Validates wearable BP monitoring for home use — could displace cuff-based home measurements and enable continuous BP surveillance.

Geneoscopy (Jan 2025 investment closed earlier)

Announcement: $105M Series C to support ColoSense at-home stool colorectal cancer screening commercialization.

Implications: Expands at-home diagnostic screening beyond chronic disease into cancer prevention — increases market breadth.

NEC X investment in General Prognostics Inc. (GPx) (Nov 2024)

Announcement: Investment focused on chronic disease monitoring/management startup.

Implications: Strategic capital flows into chronic monitoring platforms that will feed home-care ecosystems.

Philips — Virtual Care Management (Mar 2023)

Announcement: New integrated telehealth/virtual care services to boost patient engagement and outcomes.

Implications: Enterprise telehealth solution supporting scale up of home services.

Other past items (2023): OMRON Connect updates, Medtronic plan to acquire EOFlow (EOPatch insulin delivery), Home Instead & Meals on Wheels partnership — each indicates broader ecosystem activity in devices, delivery, and social support.

Recent developments

Regulatory and clinical validation momentum — FDA clearance for advanced wearables (Cardiosense) and clinical validation (Movano) show home devices reaching clinical standards.

Startups solving affordability & access — Ayati Devices and GPx investments indicate focus on low-cost diagnostics and remote chronic disease management.

Large medtechs adding AI capabilities — BD’s AI hemodynamic platform demonstrates incumbents embedding predictive analytics into monitoring products.

At-home cancer screening commercialization — Geneoscopy funding supports ColoSense rollout, expanding home testing beyond usual chronic conditions.

Platformization of telehealth — Philips Virtual Care Management and similar corporate initiatives signal bundling devices with care management.

Market segments covered

By Device Type (major buckets & explanation)

Diagnostic & Monitoring Home Devices

●Subitems: Blood glucose monitors, blood pressure monitors, ECG/heart rate monitors, pulse oximeters, sleep apnea monitors, temperature monitors, coagulation monitors, pedometers.

●Explanation: Largest revenue contributor (59% share in 2023). These devices generate continuous/episodic data enabling remote care and recurring services (subscriptions, analytics).

Therapeutics Home Healthcare Devices

●Subitems: Insulin delivery devices (pumps, patches), nebulizers, ventilator & CPAP devices, IV equipment, dialysis equipment, home mobility assist devices.

●Explanation: Typically higher unit price with clinical servicing needs; enable complex treatments at home (insulin infusion, respiratory support).

Medical Supplies

●Subitems: Consumables—dressings, infusion tubing, catheters, test strips, disposables.

●Explanation: Recurring, high-volume revenue with lower gross margin per unit but stable cash flows.

By Service

Rehabilitation Services

●Explanation: In-home physiotherapy and occupational therapy for mobility disorders and post-acute recovery.

Telehealth & Telemedicine Services

●Explanation: Virtual consults, remote monitoring platforms, integrated care management.

Infusion Therapy Services

●Explanation: Home delivery of specialty infusions (antibiotics, biologics) with nursing oversight.

Respiratory Therapy Services

●Explanation: CPAP/ventilator management, sleep therapy at home.

Unskilled Home Healthcare Services

●Explanation: ADL assistance, caregiver support and personal care.

By Indication

●Major categories: Diabetes (32% share in 2023), cardiovascular, respiratory diseases, cancer, movement disorders, wound care, pregnancy, hearing disorders, others.

●Explanation: Diabetes and cardiovascular diseases drive device and service demand; wound care and cancer screening are growing niches.

By Geography

●Regions as listed earlier (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa) with region-specific demand drivers and constraints.

Top 5 FAQs

Q1: How big is the home healthcare market today and where is it headed?

A: The market was USD 208.95 billion in 2024, estimated USD 226.92 billion in 2025, and projected to reach USD 476.80 billion by 2034, growing at a CAGR of 8.6% between 2025–2034.

Q2: Which device types and indications currently dominate the market?

A: Diagnostics & monitoring devices dominated with ~59% market share in 2023. Diabetes was the top indication with ~32% share in 2023.

Q3: Which region leads the home healthcare market?

A: North America leads (about 44% share in 2023) and accounted for roughly USD 75.7 billion of the market in 2024.

Q4: What are the major growth drivers?

A: Aging populations, rising chronic disease (notably diabetes), device miniaturization/wearables, telehealth expansion, and growing investment in at-home diagnostics.

Q5: What role is AI playing in home healthcare?

A: AI is used for signal processing, predictive risk scoring, personalized care plans, automated triage, clinical documentation, medication adherence support, operational optimization and regulatory/quality monitoring — all enabling earlier intervention, better outcomes and operational efficiency.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5110

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest