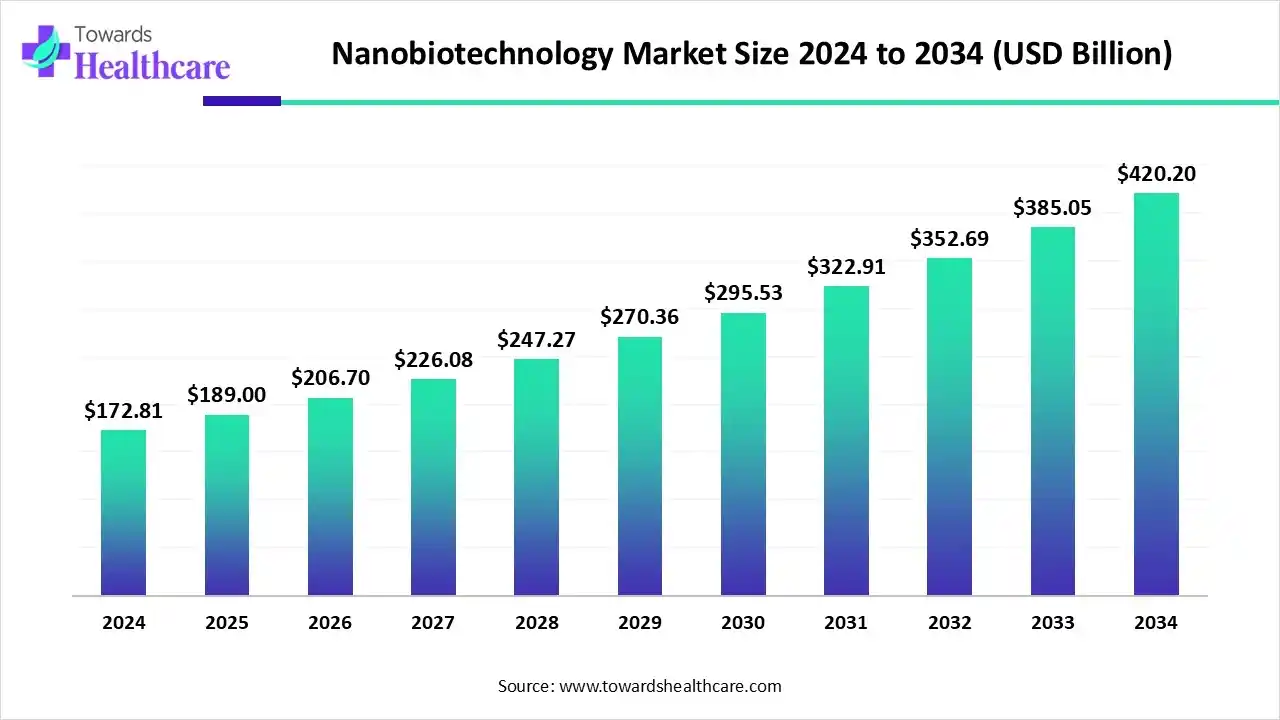

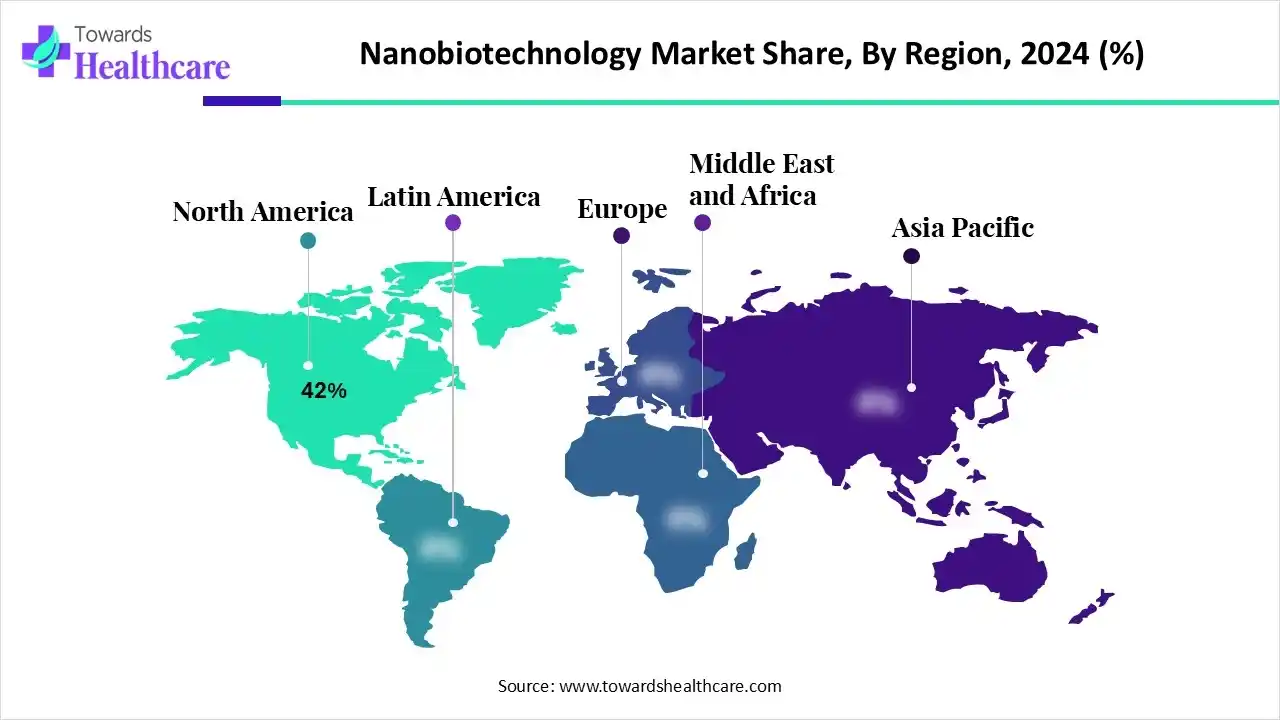

The global nanobiotechnology market is US$ 172.81B (2024), rises to US$ 289B (2025), and is projected to reach US$ 420.2B by 2034 at a 9.37% CAGR (2025–2034), led by North America (42% share, 2024) and fastest growth in Asia Pacific.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6359

Market Size

Baseline & Run-rate

➤2024 revenue: US$ 172.81B

➤2025 revenue: US$ 289B (scale-up from COVID-era nano platforms, capital re-deployment, and new RNA/vesicle pipelines).

➤2034 projection: US$ 420.2B (CAGR 9.37%, 2025–2034).

Growth Math & Implications

➤Absolute dollar growth (2025→2034): US$ 131.2B added.

➤Implied 2024→2034 multiple: 2.43×.

➤Share leader (2024): North America 42%; APAC fastest through 2034.

Capital & Capacity Indicators

➤US biotech VC (2024): US$ 15.5B early-stage + US$ 7.6B late-stage (rebound toward pre-pandemic).

➤China R&D spend (2024): ¥3,632.68B; intensity 2.69% of GDP.

➤UK government R&I (2025–2026): part of £20.4B commitment via UKRI.

Market Trends

➤Lipid Nanoparticles (LNPs) lead: 34% share (2024) among platforms as LNPs power mRNA/siRNA delivery and next-gen vaccines/therapeutics.

➤Therapeutics pull-through: 38% share (2024) as nano-carriers improve targeting, dose, and safety.

➤Nano-formulated vaccines/therapeutics dominate products: 40% share (2024); continuous pipeline beyond COVID.

➤Instrumentation & Services fastest: Characterization, consumables, analytics, and software scale with QC/regulatory complexity.

➤Exosomes/biological vesicles fastest platform growth: Native vesicles enable low-immunogenic precision delivery.

➤Oncology the top therapy area: 34% share (2024) with nano-imaging, targeted payloads, and biomarker mapping.

➤Ophthalmology & localized delivery surge: Chronic eye disease burden + nano-carriers that extend residence time.

➤Buyer mix skews to pharma/biotech: 46% share (2024); CDMOs/CMOs fastest as manufacturing professionalizes.

➤Regional divergence: NA 42% today; APAC accelerates on hospital build-out, precision medicine, and private investment.

➤AI infusion: ML-guided design, automated characterization, and in-silico scale-up compress R&D cycles (see AI section).

10 AI Roles in Nanobiotechnology

➤Inverse design of nanocarriers: ML optimizes lipid/polymer compositions for stability, endosomal escape, and tissue tropism.

➤Multi-omics→payload mapping: AI links patient omics to nano-payload choice/dose for personalized delivery.

➤In-silico ADME/Tox of nanoparticles: Predicts biodistribution, protein corona formation, immunogenicity—cuts animal studies.

➤High-throughput image analytics: Vision models quantify particle size/shape, uptake, and subcellular localization from microscopy.

➤Quality by Design (QbD) automation: Real-time analytics + AI SPC flags drift in particle size/PDI/encapsulation during manufacture.

➤Exosome cargo selection: NLP + graph ML surface disease-relevant miRNA/mRNA cargo and targeting ligands.

➤Digital twins of nano-processes: Simulate microfluidic mixing, shear, and scale-up to industrial skids.

➤Clinical response prediction: Models correlate nano-PK/PD with outcomes to stratify responders and guide trial design.

➤Supply-chain optimization: Predicts lipid/excipient demand, lead times, and CDMO slotting to de-risk launches.

➤Regulatory documentation assist: AI assembles CMC, characterization, and comparability packages with audit trails.

Regional Insights

North America (42% share, 2024)

➤Strengths: Deep VC/IPO markets; established CDMOs; FDA guidance experience.

➤Focus areas: Oncology nano-combinations, RNA therapeutics, advanced analytics.

➤Outlook: Stable leadership; partnerships with APAC for cost-efficient scale-up.

Asia Pacific (fastest CAGR)

➤China

➤Drivers: ¥3.63T R&D; state programs; hospital expansion.

➤Themes: LNP inputs, exosome platforms, domestic characterization tools.

India

➤Drivers: CDMO/CMO capacity, cost-advantaged bioprocessing.

➤Themes: Nano-formulation services, generic-to-complex transitions.

Japan & S. Korea

➤Drivers: Materials science leadership, precision medicine adoption.

➤Themes: Inorganic nanoparticles, nanorobotics research, ocular delivery.

Europe

➤Drivers: UK/continental R&I ecosystems; strong QC/analytics vendors; EMA pathways.

➤Themes: Theranostics, GMP analytics, AI-assisted characterization.

➤Outlook: High-value niches; cross-border clinical networks.

Latin America & MEA

➤Drivers: Select hospital networks, academic hubs, and public initiatives.

➤Themes: Diagnostics access, targeted oncology imports, early CDMO footholds.

➤Outlook: Smaller base; opportunity in tech transfer and kits.

Market Dynamics

Drivers

➤Platform maturity: LNPs (34% share 2024) and exosomes enable new drug classes.

➤Clinical demand: Oncology (34% share 2024) and ophthalmology needs.

➤Capital flow: US VC US$ 23.1B (2024) combined; China R&D ¥3.63T; UKRI within £20.4B.

Restraints

➤Regulatory complexity: Particle heterogeneity and long-term safety datasets.

➤Manufacturing reproducibility: Tight control of size/PDI/encapsulation across scales.

➤Cost & supply: Lipids/excipients, single-use assemblies, and skilled labor constraints.

Opportunities

➤CDMO/CMO growth: Fastest buyer segment; turnkey nano-manufacturing and analytics.

➤Exosome therapies: Fastest-growing platform for immune-quiet delivery.

➤Software/analytics: Fastest product growth—AI QC, comparability, and release testing.

Challenges

➤Immunogenicity & corona effects: Patient variability impacts efficacy.

➤Cold-chain/logistics: Especially for RNA/LNP stability.

➤Talent gap: Nano/AI/regulatory tri-skill scarcity.

Top 10 Companies

Moderna

➤Product: mRNA therapeutics/vaccines using LNP delivery.

➤Overview: End-to-end mRNA platform from design to scale.

➤Strength: Rapid design-to-clinic, deep LNP IP, global manufacturing playbooks.

BioNTech

➤Product: mRNA oncology and vaccines (LNP).

➤Overview: Immunotherapy + RNA engine co-developed with pharma partners.

➤Strength: Personalized cancer vaccines, robust trial network.

Pfizer

➤Product: Comirnaty (with BioNTech), expanding nanoparticle therapies.

➤Overview: Big-pharma scale, late-stage dev and global distro.

➤Strength: Regulatory execution, supply chain, partnerships.

Acuitas Therapeutics

➤Product: LNP delivery systems licensed broadly.

➤Overview: Specialist IP/licensing powerhouse behind multiple RNA programs.

➤Strength: Best-in-class LNP chemistries and know-how.

Precision NanoSystems (PNS)

➤Product: NanoAssemblr microfluidic “nanoparticle factory.”

➤Overview: From R&D to GMP scale with reproducible mixing.

➤Strength: Scale-translatable platforms, ecosystem training.

Evonik / CordenPharma

➤Product: Lipids, excipients, and GMP manufacturing for RNA/LNP.

➤Overview: Materials + CDMO for critical lipids/supply.

➤Strength: Secure supply, specialized lipids, global plants.

Lonza / Catalent

➤Product: CDMO services for nano-therapeutics (fill/finish, analytics).

➤Overview: End-to-end industrialization partners.

➤Strength: Capacity, regulatory track record, tech transfer.

Thermo Fisher Scientific

➤Product: Characterization instruments, consumables, analytics software.

➤Overview: Tooling backbone for nano R&D/QC.

➤Strength: Portfolio breadth, installed base, service reach.

Merck / MilliporeSigma

➤Product: Lipids, single-use systems, nanoparticle analytics kits.

➤Overview: Materials + process solutions provider.

➤Strength: GMP supply chains, application support.

Nanobiotix

➤Product: NBTXR3 nano-radioenhancer.

➤Overview: Solid-tumor radiosensitization via inorganic nanoparticles.

➤Strength: Unique modality with combo potential in oncology.

Latest Announcements & Recent Developments

Alzheimer’s breakthrough (Oct 2025): Nano-based therapy in mice rapidly clears amyloid-β, restores BBB, and improves cognition—foregrounds vascular health as a lever and sets a translational agenda for human studies.

UK nanotech mega-project (Aug 2025): National initiative to industrialize healthcare nanotechnology, building on LNP vaccine success and Vyxeos® (nano-liposomal chemotherapy) to expand platforms and manufacturing.

Funding rebound (2024): US biotech VC rebounds (US$ 15.5B early / US$ 7.6B late), signaling renewed investor risk appetite in nano-modalities.

China R&D (2024): ¥3.63T spend and 2.69% R&D intensity support domestic nano-materials, analytics, and therapy pipelines.

UKRI commitment (2025–2026): Part of £20.4B government R&I spend, sustaining nano-innovation, infrastructure, and skills.

Top 5 FAQs

1 What’s the market size and growth?

Ans US$ 172.81B (2024) → US$ 289B (2025) → US$ 420.2B (2034) at 9.37% CAGR (2025–2034).

2 Which region leads today?

Ans North America with 42% (2024); Asia Pacific grows fastest through 2034.

3 Which platforms and products dominate?

Ans LNPs (34%) by platform; nano-formulated therapeutics & vaccines (40%) by product.

4 Who buys the most?

Ans Pharma/biotech (46%); CDMOs/CMOs are the fastest-growing buyers.

5 Which therapy area leads?

Ans Oncology (34% 2024); ophthalmology & localized delivery grows fastest.

Latest Moves Snapshot

➤Moderna/BioNTech/Pfizer: Extending LNP-RNA beyond vaccines into oncology and rare diseases; global CMC scale-ups with CDMOs.

➤Acuitas: Expanding LNP licensing and formulation toolkits.

➤PNS: Rolling out GMP-ready NanoAssemblr lines for seamless lab→plant translation.

➤Evonik/CordenPharma/Merck/MilliporeSigma: Securing lipid/excipient supply chains; new grades for stability.

➤Lonza/Catalent: New fill-finish and analytics suites for nano products.

➤Nanobiotix: Advancing radioenhancer programs with combo trials.

➤Thermo Fisher/Bruker/Malvern/Cytiva/Pall/Sartorius: Next-gen characterization, single-use, and release testing stacks.

Access our exclusive, data-rich dashboard dedicated to the biotechnology sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6359

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest