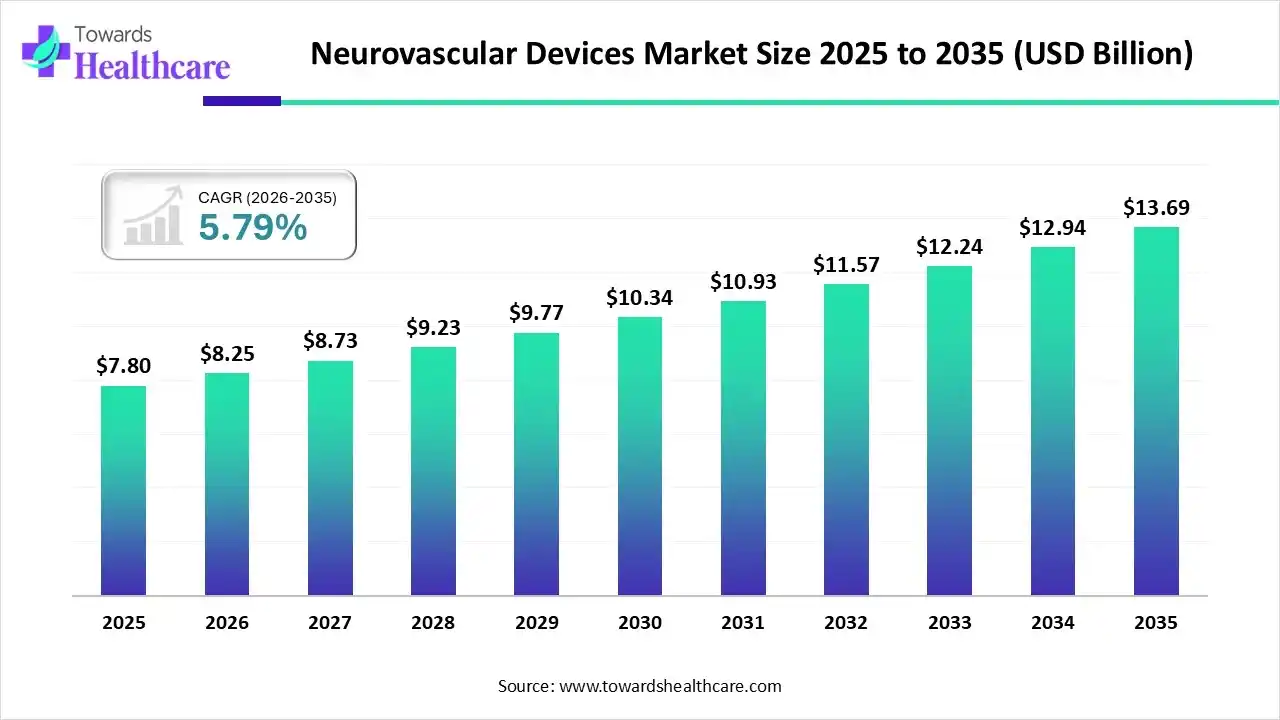

The global neurovascular devices market is valued at USD 7.80 billion in 2025, growing to USD 8.25 billion in 2026, and is projected to reach USD 13.69 billion by 2035 at a CAGR of 5.79%, driven by the rising burden of stroke, aneurysms, minimally invasive procedures, and continuous R&D.

Download Free Sample of Neurovascular Devices Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5706

Market Size

A. Historical & Current Market Valuation

-

2025 Market Size – USD 7.80 Billion

Shows strong recovery post-pandemic and increasing adoption of neurointerventional tools. -

2026 Market Size – USD 8.25 Billion

Driven by rising stroke incidence, geriatric population, and new clinical device introductions.

B. Long-Term Growth Projection

-

2035 Market Size – USD 13.69 Billion

Represents long-term investment in flow diverters, thrombectomy devices, and imaging-guided interventions. -

Overall CAGR (2026–2035): 5.79%

Stable growth supported by endovascular innovation and broader clinician adoption globally.

C. Regional Revenue Contributions

-

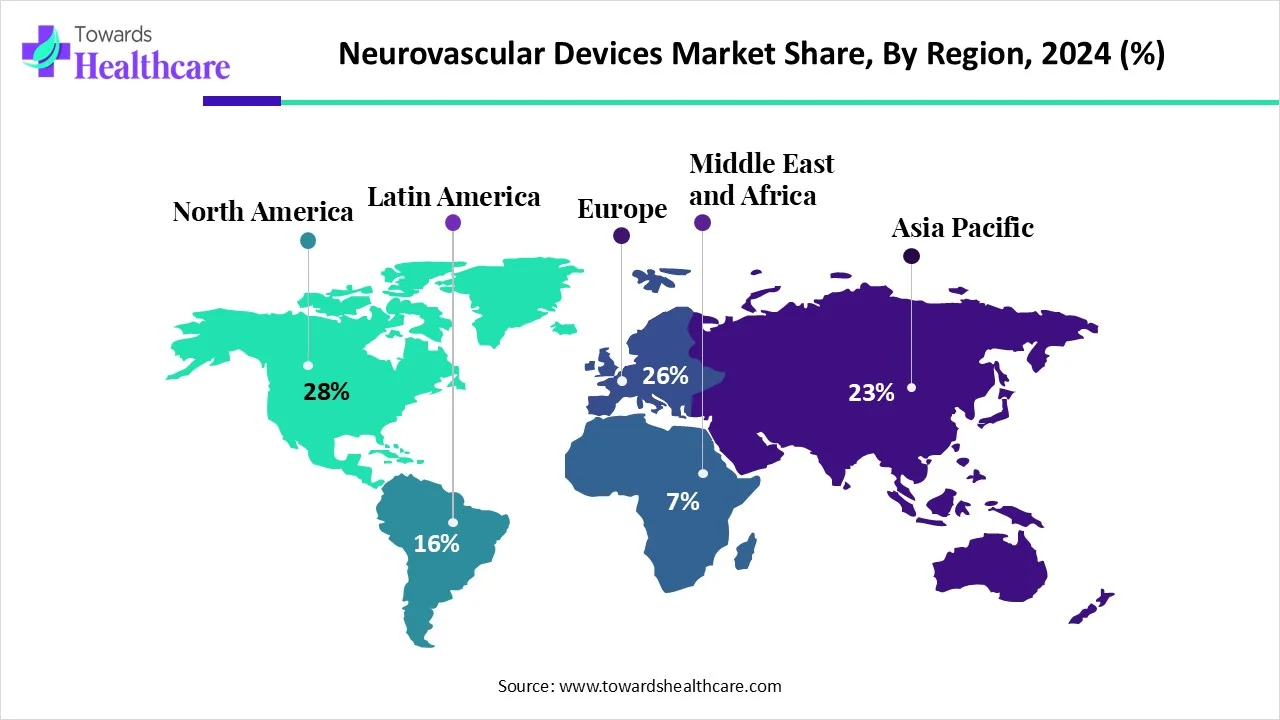

North America – 28% share in 2024

Largest region due to advanced healthcare systems, insurance support, and high disease burden. -

Asia-Pacific – Fastest CAGR

Demand boosted by aging population, stroke prevalence, and new government health initiatives.

D. Market Structure Volume

-

High device approvals

FDA approved 320 neuroendovascular devices (2000–2022), indicating a large competitive device pipeline.

E. Patient Pool Size Driving Revenue

-

Stroke prevalence – 93.8 million globally (2021)

Continuously expanding patient population increases demand for neurointervention devices.

F. Neurovascular Mortality & Burden

-

15 million affected yearly and 5 million deaths globally

High disease burden increases device adoption for prevention and treatment.

G. Cost Distribution & Procedure Volume

-

High-value procedures

Neurovascular surgeries often involve devices costing thousands of dollars, improving market value per procedure.

Market Trends

A. Growing Disease Burden

-

Sharp rise in stroke incidence, aneurysm cases, and AVMs driving device adoption.

-

Increasing cardiovascular issues among ages 18–64 pushing neurothrombectomy demand.

B. Strong Push Toward Minimally Invasive Surgery

-

Industry shift from open neurosurgery to microcatheters, coils, flow diverters, and aspiration catheters.

-

Lower trauma, faster recovery, and reduced hospital stay increase procedure acceptance.

C. Technological Advancement & Miniaturization

-

Miniaturized coils, flexible microcatheters, and soft-metal devices improve navigation in cerebral vessels.

-

Emergence of deflectable access platforms for advanced neurointerventional reach.

D. Strategic Collaborations and Acquisitions

-

Kaneka acquiring ESM (96.8% shares) to expand aneurysm treatment portfolio (Nautilus).

-

Philips x Sim&Cure partnership to integrate Sim&Size into image-guided platforms.

E. High R&D Investment

-

Leading companies expanding R&D for next-gen thrombectomy, stenting, and embolization systems.

-

Government funding (U.S., Canada, EU, China, India) encouraging medical device innovation.

F. Imaging & Precision Navigation Integration

-

More devices are being designed for AI-enabled imaging, precision stent placement, and vessel mapping.

AI Impacts on the Neurovascular Devices Market

1. AI-Enhanced Neurovascular Imaging

AI can automatically detect aneurysms, clots, stenosis, and vessel malformations on CT/MRI.

2. Automated Measurement & Vessel Segmentation

AI outlines vessel boundaries, clot lengths, aneurysm dome/neck ratios—reducing clinician effort.

3. Procedure Planning & Navigation

AI algorithms simulate catheter pathways, select ideal access routes, and reduce navigation errors.

4. Predictive Patient Outcome Modeling

AI predicts likelihood of rupture, re-bleeding, thrombosis, and treatment success for individual patients.

5. Implant Compatibility Assessment

AI systems evaluate biocompatibility to minimize immune reactions and select optimal implants.

6. Real-Time Intraoperative Support

AI overlays real-time guidance during coiling, clot retrieval, or stent deployment.

7. Remote Monitoring & Early Alerts

Wearables and smart systems track neuro signs in post-op patients and trigger alerts for complications.

8. Workflow Optimization for Hospitals

AI integrates with image-guided therapy systems (e.g., Philips Azurion + Sim&Size).

9. Automated Data Capture for Clinical Trials

AI reduces trial time by analyzing device performance, reducing manual documentation.

10. Robotics & AI-Assisted Endovascular Surgery

Future systems will combine micro-robotics + AI to navigate ultrathin catheters through cerebral arteries.

Regional Insights

North America – 28% Market Share (Leader)

Key Drivers

High prevalence of aneurysms (6.8M U.S. citizens).

30,000 ruptures annually → massive clinical need.

Strong insurance support for high-cost surgeries.

Government Support

U.S. BRAIN Initiative – $740M (FY2025) for neurological innovation.

Strong FDA approval ecosystem (320 neuroendovascular devices approved 2000–2022).

B. Asia-Pacific – Fastest Growing Region

Why Fastest?

Highest global stroke burden.

Rapidly aging population (China, Japan, South Korea).

High adoption of minimally invasive care.

Government Initiatives

China Stroke Prevention Program under Healthy China 2030.

India establishing 500 stroke care units and mobile stroke centers.

Industry Attraction

NMPA incentives encouraging foreign device manufacturing in China.

C. Europe – Strong Growth

Key Factors

Mature healthcare systems, strong reimbursements.

Large presence of major players (Medtronic, Heraeus Medevio, iVascular).

Government Support

Germany’s National Health Alliance (NHA) for CVD prevention.

Pilot programs for early detection of hypercholesterolemia and heart failure.

D. Middle East & Africa – Growing Awareness

Drivers

Rising neurological disorders and increased screening culture.

Expanding private healthcare investments.

Notable Initiative

UAE MOHAP’s “National Framework for Healthy Ageing 2025–2031” supports neuro care for elderly.

Market Dynamics

A. Driver – Rising Prevalence of Neurovascular Disorders

15M people affected and 5M deaths annually worldwide.

Stroke prevalence in 2021: 93.8M; incidence: 11.9M.

Increasing diabetes, hypertension, obesity worsen risks.

B. Restraint – High Device & Procedure Cost

Neurovascular surgeries require expensive coils, stents, aspiration catheters.

Limited affordability in low- and middle-income groups.

C. Opportunity – Minimally Invasive Surgery Boom

Reduced trauma, faster recovery, lower infection risk.

Increasing patient preference → higher device demand.

New materials increase biocompatibility and device safety.

Top 10 Companies

1. Medtronic

Products: Flow diverters, microcatheters, stent systems.

Overview: Global medical device giant.

Strength: Broad portfolio, strong regulatory approvals, global distribution.

2. Stryker Corporation

Products: Aneurysm coils, thrombectomy devices.

Strength: Pioneer in neurointervention; strong U.S. hospital penetration.

3. Johnson & Johnson (MedTech)

Products: Cereglide 92 Catheter System.

Strength: Deep R&D capabilities; large clinical network.

4. Penumbra, Inc.

Products: Aspiration catheters, stroke solutions.

Strength: Leader in clot removal technologies.

5. Royal Philips

Products: Image-Guided Therapy Platform (Azurion).

Strength: Best-in-class imaging + software integration.

6. Terumo Neuro

Products: SOFIA 88 Support Catheter.

Strength: Strong access and aspiration catheter technologies.

7. Rapid Medical

Products: DRIVEWIRE 24 deflectable access platform.

Strength: Robotics-like deflection control; innovation focus.

8. Kaneka Corporation

Products: Nautilus aneurysm device (via ESM acquisition).

Strength: Aggressive expansion; new aneurysm tech.

9. Perflow Medical

Products: Novel flow modulation devices.

Strength: Strong focus on precision blood-flow engineering.

10. Heraeus Medevio

Products: Neurovascular implant components.

Strength: Material science excellence, device customization.

Latest Announcements

A. Johnson & Johnson MedTech

Launched Cereglide 92 Catheter System.

Designed to address access challenges and improve thrombectomy outcomes.

Supports ischemic stroke suite of technologies.

B. Kaneka Corporation

Acquired 96.8% of EndoStream Medical (ESM).

Gains Nautilus aneurysm treatment technology.

Targeting sales of 20 billion yen by 2030.

C. Royal Philips

Expanded partnership with Sim&Cure.

Integrating Sim&Size into the Azurion platform for aneurysm planning.

Recent Developments

A. Terumo Neuro – SOFIA 88 (May 2025)

Large-bore catheter for advanced procedural flexibility.

Supports precise control during interventions.

Adds to company’s stroke portfolio.

B. Rapid Medical – DRIVEWIRE 24 (July 2024)

First-of-its-kind deflectable access platform.

Enables direct navigation of aspiration catheter to arterial occlusion.

First clinical procedure successfully completed.

Segments Covered

A. By Device

Cerebral Embolization & Aneurysm Coiling Devices

Function: These devices block or fill aneurysms to prevent rupture.

Clinical Relevance: Endovascular coiling prevents blood flow into the aneurysm, reducing hemorrhage risk.

Market Insights: This segment held dominant revenue share in 2024 due to the rising prevalence of cerebral aneurysms, availability of miniaturized coils, and use of soft metals improving patient comfort.

Innovation Trend: Development of spring-shaped or polymer-based coils enhances efficacy and safety for fragile cerebral vessels.

Flow Diversion Devices

Function: Redirect blood flow away from aneurysm sacs without occluding parent arteries.

Clinical Relevance: Particularly used for large or complex aneurysms unsuitable for standard coiling.

Market Insight: Increasing adoption in complex neurovascular cases and inclusion in hospital interventional suites.

Innovation Trend: Integration with AI-based imaging for precise placement, reducing procedural complications.

Liquid Embolic Agents

Function: Fill aneurysms or arteriovenous malformations (AVMs) and solidify in situ.

Clinical Relevance: Provides controlled embolization in fragile or complex vessel structures.

Market Insight: Preferred for AVMs and microvascular occlusions where mechanical coils may be insufficient.

Innovation Trend: New bio-compatible polymers improve long-term vessel safety and minimize inflammatory response.

Neurothrombectomy Devices

Function: Retrieve or aspirate blood clots during ischemic stroke treatment.

Clinical Relevance: Rapid clot removal reduces ischemic injury and long-term disability.

Market Insight: Fastest-growing device segment due to rising stroke cases and FDA approvals for acute ischemic stroke interventions.

Innovation Trend: Multi-modal devices (clot retrieval + aspiration) and deflectable catheter platforms like DRIVEWIRE 24 improve procedural success.

Angioplasty & Stenting Systems

Function: Widen stenosed arteries and prevent re-narrowing.

Clinical Relevance: Used for cerebral artery stenosis, preventing ischemic events.

Market Insight: Provides long-term vessel patency and complements thrombectomy procedures.

Innovation Trend: Miniaturized stents and drug-eluting variants reduce restenosis rates and procedural risk.

Support Devices (Microcatheters, Micro Guidewires, Trans Radial Access Devices)

Function: Facilitate navigation, device deployment, and procedural control.

Clinical Relevance: Critical for reaching tortuous cerebral vasculature.

Market Insight: Hospitals prefer high-quality microcatheters for procedure efficiency; TRA devices reduce vascular trauma.

Innovation Trend: Flexible, kink-resistant, and hydrophilic coatings improve maneuverability and safety.

By Size

0.021”

Dominance: Most commonly used due to universal compatibility and optimal flexibility.

Clinical Relevance: Suitable for aneurysm treatment, clot removal, and other neurovascular interventions.

Market Insight: Devices in this size are preferred by hospitals and specialty clinics for most procedures.

Other Sizes (0.027”, 0.071”, 0.017”, 0.019”, 0.013”, 0.058”, 0.068”)

Function: Designed for specific vessel diameters and anatomical variations.

Clinical Relevance: Larger sizes (0.071”) may be used for major arteries, smaller sizes (0.013”–0.019”) for distal microvasculature.

Market Insight: Custom sizing improves procedural safety and efficacy; demand grows with personalized therapy approaches.

By End-Use

Hospitals

Dominance: Largest segment due to infrastructure availability, skilled staff, and higher patient inflow.

Market Insight: Hospitals invest in high-end image-guided systems, robotic-assisted platforms, and comprehensive stroke care programs.

Clinical Relevance: Hospitals perform complex aneurysm and stroke interventions requiring multidisciplinary expertise.

Specialty Clinics

Growth Potential: Fastest-growing end-use segment.

Market Insight: Clinics focusing on neurovascular disorders increasingly adopt minimally invasive devices due to lower operational cost compared to hospitals.

Clinical Relevance: Provide targeted treatment for high-risk patients, including elective coiling, flow diversion, and thrombectomy.

By Region

North America

Share: 28% in 2024; largest market.

Growth Drivers: High stroke prevalence, advanced healthcare infrastructure, favorable reimbursement policies.

Key Trends: U.S. BRAIN initiative, 320 FDA-approved devices (2000–2022), hospital-led adoption.

Europe

Growth Factors: Strong medical device sector, high geriatric population, widespread clinical adoption.

Key Countries: Germany leads with advanced neurovascular care infrastructure.

Trends: Mergers & acquisitions and regulatory support for innovative devices.

Asia-Pacific

Fastest Growing: Driven by stroke prevalence, aging population, and government initiatives like Healthy China 2030.

Market Trends: Increasing hospital and clinic investments, foreign manufacturer incentives, and growing demand for home healthcare.

Latin America (LATAM)

Drivers: Rising awareness of stroke, urban healthcare adoption, and improving neurovascular facilities.

Trend: Gradual adoption of advanced thrombectomy and coiling devices.

Middle East & Africa (MEA)

Growth: Moderate CAGR expected.

Drivers: Awareness campaigns, government initiatives (UAE MOHAP), and increasing private investments.

Trend: Gradual adoption of neurointerventional devices for stroke and aneurysm treatment.

Top 5 FAQs

1. What is the market size of neurovascular devices?

USD 7.80B in 2025 → 8.25B in 2026 → 13.69B by 2035 (CAGR 5.79%).

2. Which region leads the market?

North America with 28% share (2024).

3. Which region will grow fastest?

Asia-Pacific, driven by stroke burden, aging population, and healthcare initiatives.

4. What are the major factors driving growth?

Rising stroke prevalence, increasing aneurysm cases, minimally invasive surgeries, and strong R&D.

5. Who are the top key players?

Medtronic, Stryker, Johnson & Johnson, Penumbra, Philips, Terumo Neuro, Rapid Medical, Kaneka, Perflow, Heraeus Medevio, Evasc.

Access our exclusive, data-rich dashboard dedicated to the medical devices industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Neurovascular Devices Market Report Now at: https://www.towardshealthcare.com/checkout/5706

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest