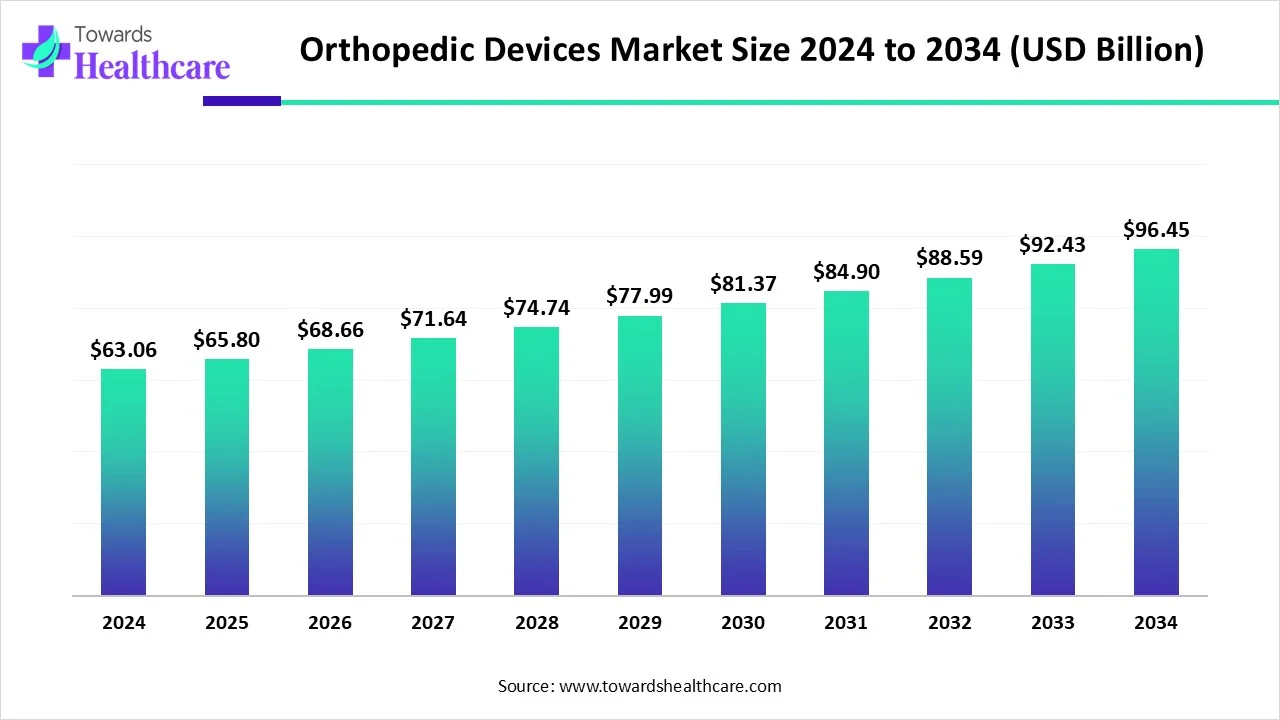

The global orthopedic devices market was USD 63.06 billion in 2024, grew to USD 65.8 billion in 2025, and is projected to reach USD 96.45 billion by 2034 (CAGR 4.34% from 2025–2034), driven by rising orthopedic disorders, aging populations, faster adoption of advanced manufacturing (3D printing) and single-use devices, and expanding care settings (hospitals → outpatient/ASCs).

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5721

Market size

Historical & near-term size

●2024 market value: USD 63.06B — baseline reflecting implant, trauma, orthobiologics, instruments and services demand.

●2025 market value: USD 65.8B — early growth driven by continued surgery volumes and new product launches.

Long-term projection

●2034 projected value: USD 96.45B — reflects cumulative demand expansion across regions, incremental adoption of novel materials and devices, and greater use of outpatient surgical pathways.

Growth rate

●CAGR 4.34% (2025–2034) — steady, moderate expansion consistent with medical device industry norms where product innovation and demographic tailwinds combine with regulatory and reimbursement constraints.

Regional concentration

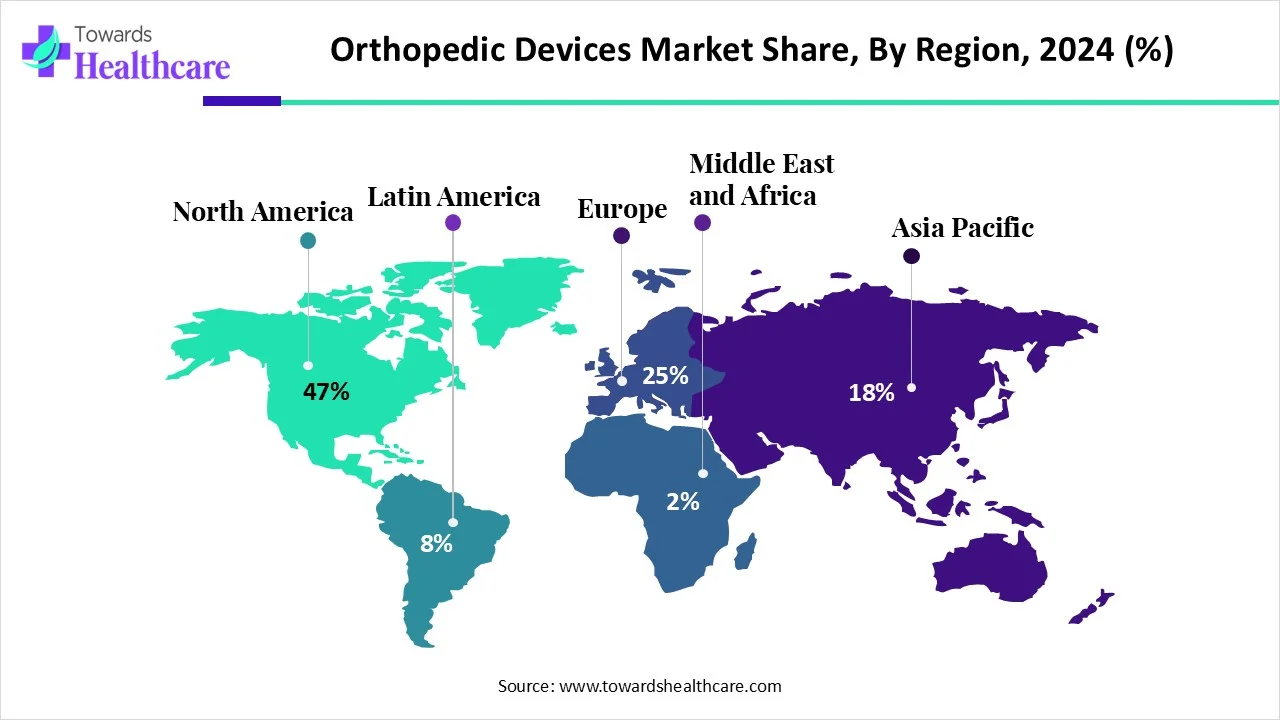

●North America = 47% revenue share (2024) — largest market due to reimbursement, high procedure rates, and presence of leading players.

Product mix impact on TAM

●Joint replacements/orthopedic implants are the largest single product contributor in 2024 (knee highest).

●Orthobiologics show the fastest projected CAGR — will increasingly lift TAM as biologics, stem cell and growth-factor solutions scale.

End-use split (impact on market size)

●Hospitals currently capture most spend because they host complex surgeries and have capital equipment budgets.

●Outpatient facilities (ASCs, specialty clinics) are the fastest-growing channel—shifting procedures here increases procedure throughput and reduces per-procedure costs, expanding accessible volume.

Value creation levers

●New materials (e.g., plant-based nanocellulose), single-use disposables, smart implants, and additive manufacturing will unlock higher-value products and new service revenues (monitoring, analytics).

Supply & export dynamics

●Large exporter countries and manufacturing hubs influence realized market value through industrial policy, cost of goods, and trade flows.

Patient demographics

●Aging populations and rising osteoarthritis prevalence directly scale volume side of the market (more joint replacements, regenerative procedures).

Clinical & reimbursement environment

●Favorable reimbursement and registry data (e.g., large arthroplasty registries) support adoption of new devices and justify premium pricing for demonstrably better outcomes.

Market trends

Rising global rehabilitation focus

●WHO’s Rehabilitation 2030 raises priority on rehab access for musculoskeletal disorders → stronger demand for post-op devices, orthoses, and home-based recovery tools.

Academic–industry partnerships

●Example: IIT Guwahati × Miraclus Orthotech (Jan 2025) to accelerate R&D, testing, IP and skills — trend: universities + med-tech co-developing implants and validation pipelines.

Startup funding & scale-up

●OSSIO’s $27.6M equity (Dec 2024) to expand pipeline and U.S. manufacturing → trend: capital flows into bio-material and next-gen implant startups.

New device launches with focused engineering

●Fusion’s Metalogix Eternal Fixation Systems (Jan 2025) and Group FH ORTHO’s JARVIS (Jan 2025) show engineering toward specific anatomic needs (long bones, reverse shoulder) — trend toward niche, problem-solving products.

Materials innovation

●UPM Biomedicals’ plant-based nanocellulose (FibGel) and other biocompatible polymers indicate strong movement toward sustainable, animal-free, injectable materials enabling minimally invasive procedures.

Shift to outpatient care

●Growth of ASCs and specialized clinics → more procedures outside hospitals, shorter stays, and device designs optimized for fast turnover and simpler logistics.

Additive manufacturing (3D printing) adoption

●Patient-specific implants and reduced waste become operational realities; 3D printing supports lower run-size customization and complex geometries.

Single-use device demand

●Infection control and procedural efficiency push single-use instruments and disposables; this increases recurrent consumable revenue.

Rise of orthobiologics

●Greater use of stem cell therapies, BMPs, viscosupplementation and growth factors moves part of treatment away from mechanical-only solutions to biologically driven healing.

Policy & local manufacturing push

●China’s “Made in China” and India’s MedTech program (Rs 500 crore) encourage local production, impacting pricing, supply security, and export competitiveness.

10 ways AI can (and will) impact this market

Smart implants & in-vivo monitoring

●What: AI-enabled sensor suites inside implants to measure strain, temperature, pressure, alignment, biochemical markers.

●Why it matters: Real-time anomaly detection reduces complications, enables earlier interventions, and creates follow-up service revenue (remote monitoring subscriptions).

Predictive surgical planning & simulation

●What: AI models process imaging + motion data to recommend implant size, alignment and surgical approach.

●Why: Shorter OR time, fewer revisions, improved outcomes — makes premium implants easier to justify.

Generative design for optimized implants

●What: AI algorithms propose lattice structures and topology-optimized geometries tailored to patient bone quality.

●Why: Stronger, lighter implants and reduced material use; pairs with 3D printing for rapid manufacturing.

Manufacturing automation & robotics

●What: AI controls robotic arms and process lines for precise machining, additive manufacturing and assembly.

●Why: Higher yield, consistency, and lower unit cost—critical for complex materials (PEEK, nanocellulose composites).

Quality control via machine vision

●What: CV systems detect micro-defects, surface irregularities, or deviations in implants and instruments.

●Why: Faster QA, fewer recalls, better regulatory dossiers.

Supply chain optimization & demand forecasting

●What: AI forecasts procedure volumes by region, manages inventory across hospitals/ASCs.

●Why: Reduces stockouts/overstock for high-value implants and single-use kits; improves distributor efficiency.

Clinical trial & regulatory acceleration

●What: AI finds optimal patient cohorts, simulates outcomes, and synthesizes real-world evidence.

●Why: Shorter trials, stronger submissions to regulators (FDA/EMA), lower cost to bring new devices to market.

Post-market surveillance & safety signal detection

●What: AI mines registries, electronic records, and device telemetry for adverse event patterns.

●Why: Timely safety signals, iterative product improvements and stronger market trust.

Personalized rehabilitation & tele-rehab

●What: AI provides adaptive rehab protocols via wearables and apps, monitoring gait, range, and adherence.

●Why: Better functional outcomes, reduced readmissions, and added digital service revenue.

Clinical decision support & reimbursement optimization

●What: AI calculates cost-benefit and outcome projections to support surgeons and payors choosing devices.

●Why: Helps justify higher-cost biologics or smart implants by demonstrating value in outcomes and total cost of care.

Regional insights

North America (lead — 47% share in 2024)

Drivers

●High procedure volumes (arthroplasty registry >4M hip/knee procedures by Oct 2024).

●Strong reimbursement frameworks and hospital budgets.

Strengths

●Home to many top players & R&D centers → rapid clinical validation and market launch.

Challenges

●High costs and stringent regulatory expectations demand robust clinical evidence.

Implication

●North America will remain premium market for high-value implants, smart devices, and digital services.

United States

Clinical capacity

●Large number of active orthopedic surgeons concentrated in states like CA, TX, NY → enables high procedural throughput.

Trade

●U.S. exported $14.6B in orthopedic appliances (2023) → strong manufacturing & global market influence.

Implication

●Device makers prioritize U.S. approvals and supply chains; registry data from U.S. influences global adoption.

Canada

Trends

●Active professional bodies (Canadian Orthopedic Association) and Health Canada approvals.

●Company expansions (Contura Orthopedics Canada Ltd., Feb 2025) indicate market entry/availability for new treatments.

Implication

●Canada is an adoption market with public healthcare nuances — manufacturers focus on regulatory clarity and cost-effectiveness.

Asia-Pacific (fastest growing)

Drivers

●Large patient pools, rising geriatric population, government MedTech support programs.

China

●“Made in China” policy to boost domestic production of mid-to-high-end devices — will reduce import dependence and shift global manufacturing balance.

India

●50M knee osteoarthritis patients; Rs 500 crore MedTech program supports local producers and export growth.

Implication

●Asia-Pacific offers volume growth and cost-competitive manufacturing; companies will localize R&D and production.

Europe

Strengths

●Robust healthcare infrastructure and R&D; Switzerland & Ireland major exporters (large per-capita exports in 2023).

Implication

●Europe balances innovation with export orientation — strong base for specialty device development.

Middle East & Africa (MEA)

Drivers

●Rising burden of bone disorders, increasing adoption of advanced tech, government funding.

Country examples

●UAE: local providers (Auxein, ORTEK Medical, Bonetech) and high arthritis prevalence.

●Saudi Arabia: growing clinical trial activity; notable osteoarthritis prevalence.

Implication

●MEA is a growth frontier; local manufacturing and tailored reimbursement models will be key.

Latin America

Notes

●Increasing need for improved orthopedic care; potential growth with investments in infrastructure and skilled workforce.

Market dynamics

Primary driver — rising prevalence of orthopedic disorders

●Osteoarthritis affects 7.6% global population and is projected to increase substantially by 2050 → higher demand for knee/hip replacements and orthobiologic therapies.

●Aging population (projected hundreds of millions more elderly by mid-century) increases lifetime likelihood of orthopedic interventions.

Secondary driver — technology & materials innovation

●3D printing, better biomaterials (PEEK, plant-based nanocellulose), smart implants and orthobiologics expand treatment options and device value.

Channel & care model shift

●Movement from inpatient hospital care to ASCs/outpatient facilities increases procedure volumes and turns device design toward short-stay, modular systems.

Regulatory & reimbursement environment

●Strong registries and approvals support adoption but require robust clinical data — positive for companies that invest in evidence generation.

Restraint — biocompatibility & material limitations

●Biomaterial incompatibility risks (hypersensitivity, calcification, mismatch with tissue mechanics) limit adoption of some innovations and raise clinical liability concerns.

Opportunity — additive manufacturing & customization

●3D printing enables patient-specific implants, reduces waste, and supports rapid prototyping — addresses biocompatibility via tailored design and porous structures.

Supply-side dynamics

●Local manufacturing policies (China, India) and export leadership (Switzerland, Ireland, U.S.) shape competitive landscape and margins.

Capital & funding

●Venture and equity funding (OSSIO $27.6M) accelerate pipeline companies; larger players continue M&A and partnership strategies.

Value chain evolution

●R&D → clinical trials → approvals → distribution to hospitals/ASCs → patient support services — digital tools and remote monitoring increasingly sit across the chain to add recurring revenue.

Outcome economics

●Payors and providers seek devices that shorten recovery and reduce lifetime costs (fewer revisions, faster rehab) — devices that demonstrate this capture premium positions.

Top 10 companies

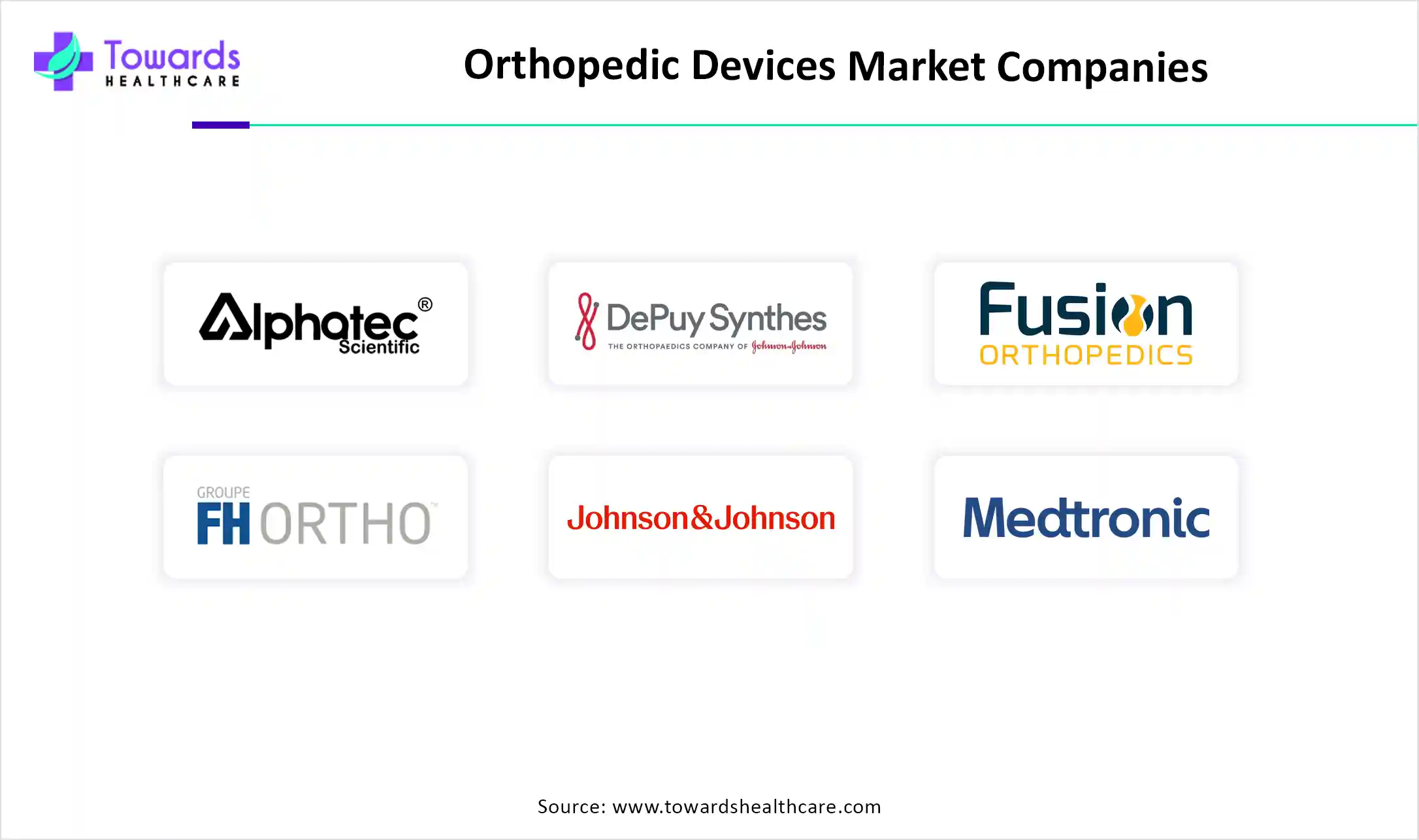

Alphatec Scientific

●Product / overview: Spine and orthopedics-focused implant systems.

●Strength: Niche specialization in spinal implant technologies and clinical focus driving surgeon adoption.

DePuy Synthes (J&J family)

●Product / overview: Broad portfolio including joint replacements, trauma and spine implants.

●Strength: Global scale, deep clinical relationships, extensive implant portfolio and strong R&D resources.

Fusion Orthopedics USA LLC

●Product / overview: Fixation systems and trauma implants; recently launched Metalogix Eternal Fixation Systems for long bone fractures and limb lengthening.

●Strength: Focused engineering for complex long-bone solutions; recent product launches indicate rapid innovation cycle.

Group FH ORTHO

●Product / overview: Shoulder prostheses (e.g., JARVIS reverse shoulder baseplate launched in U.S.).

●Strength: Engineering innovation in joint arthroplasty components with options for compression/locking screws and glenosphere compatibility.

Johnson & Johnson

●Product / overview: Through DePuy and other subsidiaries, major global orthopedic implant presence.

●Strength: Global commercial footprint, trusted brands, strong distribution and payer relationships.

Madison Ortho

●Product / overview: Orthopedic implant and device offerings (mid-to-niche players).

●Strength: Focused offerings, agility to partner with clinicians and adopt new materials/practices.

Medtronic

●Product / overview: Broad medtech portfolio including spinal implants and instrumentation.

●Strength: Large R&D and regulatory capability; cross-product synergies in devices and digital health.

Miraclus Orthotech

●Product / overview: Orthopedic implants and equipment; entered partnership with IIT Guwahati to accelerate R&D and validation.

●Strength: Academic partnerships for rapid prototype testing and tech transfer; focus on regionally relevant innovations.

Stryker Corporation

●Product / overview: Comprehensive orthopedic portfolio: joint replacement, trauma, surgical equipment.

●Strength: Strong commercially, broad device reach, surgical tools & service offerings that lock in hospital customers.

UPM Biomedicals

●Product / overview: Biomaterials — first to develop plant-based nanocellulose for medical devices (FibGel) intended for injectable hydrogel applications.

●Strength: Material innovation (sustainable, animal-free), potential to enable minimally invasive procedures and new regenerative approaches.

Zimmer Biomet

●Product / overview: Major joint reconstruction and spine portfolio.

●Strength: Longstanding clinical adoption, broad international reach, and extensive implant catalog.

Latest announcements

UPM Biomedicals — plant-based nanocellulose (FibGel)

What: Claimed first to develop plant-based nanocellulose for medical devices in injectable hydrogel form. Plans to initiate clinical trials in 2025 and to collaborate across soft tissue repair, joint/disk repair, wound care, drug delivery, and cell therapy.

Implication: If clinical trials validate safety/efficacy, FibGel may offer a sustainable, animal-free alternative to current hydrogels and support minimally invasive regenerative interventions.

Fusion Orthopedics — Metalogix Eternal Fixation Systems (Jan 2025)

What: New generation fixation systems engineered for long bone fractures, limb lengthening and corrections; designed for strength and patient comfort.

Implication: Addresses complex orthopedic trauma and limb reconstruction markets; may enable better outcomes and reduce revision rates.

Group FH ORTHO — JARVIS reverse shoulder baseplate (Jan 2025)

What: Round baseplate for reverse shoulder prostheses with options for compression/locking screws and glenosphere compatibility; launched in U.S.

Implication: Expands choices for surgeons in shoulder arthroplasty and may improve fixation options for difficult glenoid anatomies.

OSSIO, Inc. — $27.6M equity raise (Dec 2024)

What: Funding to expand product pipeline (OSSIOfiber implants), sales channels, medical education and build U.S. manufacturing.

Implication: Increased capital to commercialize regenerative implant offerings; signals investor interest in biomaterial-based orthopedics.

Miraclus Orthotech × IIT Guwahati partnership (Jan 2025)

What: Collaboration on R&D, product testing/validation, skill development and IP creation.

Implication: Strengthens indigenous innovation capacity and accelerates translational research.

Contura Orthopedics — Canada launch (Feb 2025)

What: Formation of Contura Orthopedics (Canada) Ltd. to supply Health Canada-approved Arthrosamid for knee osteoarthritis pain.

Implication: Illustrates ongoing market entry activity and product availability expansion in Canadian markets.

Registry & export highlights

AJRR: >4M hip & knee arthroplasty procedures logged as of Oct 2024 — supports large dataset for outcomes research.

U.S. exports: $14.6B orthopedic appliances (2023) — underscores manufacturing & trade strength.

Recent developments

Product launches (Fusion, Group FH ORTHO) are tightening the gap between niche clinical needs and device offerings (long-bone fixation, reverse shoulder glenoid solutions).

Materials & biotech funding (UPM FibGel, OSSIO funding) show a pivot toward biologics and sustainable materials, enabling minimally invasive and regenerative strategies.

Academic–industry collaboration (IIT Guwahati × Miraclus) accelerates regionally relevant innovation and workforce skill development.

Market structure shifts — outpatient facilities and ASCs are scaling, pressuring device makers to offer modular, fast-turnover solutions and disposable kits.

Geopolitical policy effects — “Made in China” and India MedTech support alter manufacturing footprints and pricing dynamics globally.

Data & registries (AJRR scale) create fertile ground for device validation, benchmarking and post-market surveillance.

Export leadership (Switzerland, Ireland, U.S.) continues to influence trade flows and competitive edge in high-end device manufacturing.

Clinical trial activity growth in markets such as Saudi Arabia demonstrates expanding regional research capacity.

Growing orthobiologics momentum (fastest CAGR) reflects clinical appetite for non-mechanical healing options and lower revision risk.

Single-use & infection control demand increases recurring consumables revenue and reshapes OR logistics.

Segments covered

Joint Replacement / Orthopedic Implants

●Subsegments: Knee, hip, shoulder, elbow, foot & ankle, upper/lower extremity.

●Explanation: Largest revenue contributor in 2024; knee replacements most numerous due to osteoarthritis prevalence. Innovations include patient-specific implants and smart implant sensors.

Orthobiologics

●Subsegments: Viscosupplementation, demineralized bone matrix, synthetic bone substitutes, BMPs, stem cell therapy, allografts.

●Explanation: Fastest growing due to biological compatibility, regenerative potential and reduced need for mechanical revision.

Trauma

●Subsegments: Implants (plates, screws, nails, pins, wires) and instruments.

●Explanation: High volume for acute injuries; demand rises with urbanization and sports injuries; new fixation systems (e.g., Metalogix) target complex cases.

Spinal Implants

●Subsegments: Fusion systems, motion preservation, cages, instrumentation.

●Explanation: Specialized devices with long development cycles; AI and robotics increasingly used in planning and navigation.

Sports Medicine & Body Reconstruction

●Subsegments: ACL/PCL repair, soft tissue repair, cartilage repair.

●Explanation: Driven by active populations; regenerative approaches increasingly applied.

Body Monitoring & Evaluation / Support & Recovery

●Subsegments: Wearable sensors, motion analysis, orthoses, recovery aids.

●Explanation: Enables tele-rehab, outcome tracking and personalized recovery programs.

Dental & Craniomaxillofacial Implants

●Subsegments: Dental implants, CMF plates and fixation devices.

●Explanation: Smaller but steady volumes with high margin, often leveraging similar biomaterials.

Accessories & Instruments

●Subsegments: Surgical instruments, navigation tools, disposables.

●Explanation: Critical for OR workflows; single-use instruments increase consumable revenue streams.

Body Reconstruction & Repair Accessories

●Explanation: Covers soft tissue scaffolds, drug-delivery implants and cell therapy carriers.

Others (emerging niches)

●Examples: Nanocellulose hydrogels, smart implants with telemetry, modular lengthening systems.

Top 5 FAQs

-

Q: What was the orthopedic devices market size in 2024 and 2025?

A: It was USD 63.06B in 2024 and USD 65.8B in 2025. -

Q: What is the projected market size and growth rate to 2034?

A: Projected ~USD 96.45B by 2034, with a CAGR of 4.34% (2025–2034). -

Q: Which product segment dominated in 2024 and which will grow fastest?

A: Joint replacement/orthopedic implants dominated in 2024; orthobiologics are expected to register the fastest CAGR going forward. -

Q: Which region led the market in 2024?

A: North America led with 47% revenue share in 2024. -

Q: What are key risks or restraints for the market?

A: Biocompatibility issues with some biomaterials (hypersensitivity, calcification, biomechanics mismatch) pose clinical and regulatory risks that can delay adoption.

Access our exclusive, data-rich dashboard dedicated to the medical devices industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5721

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest