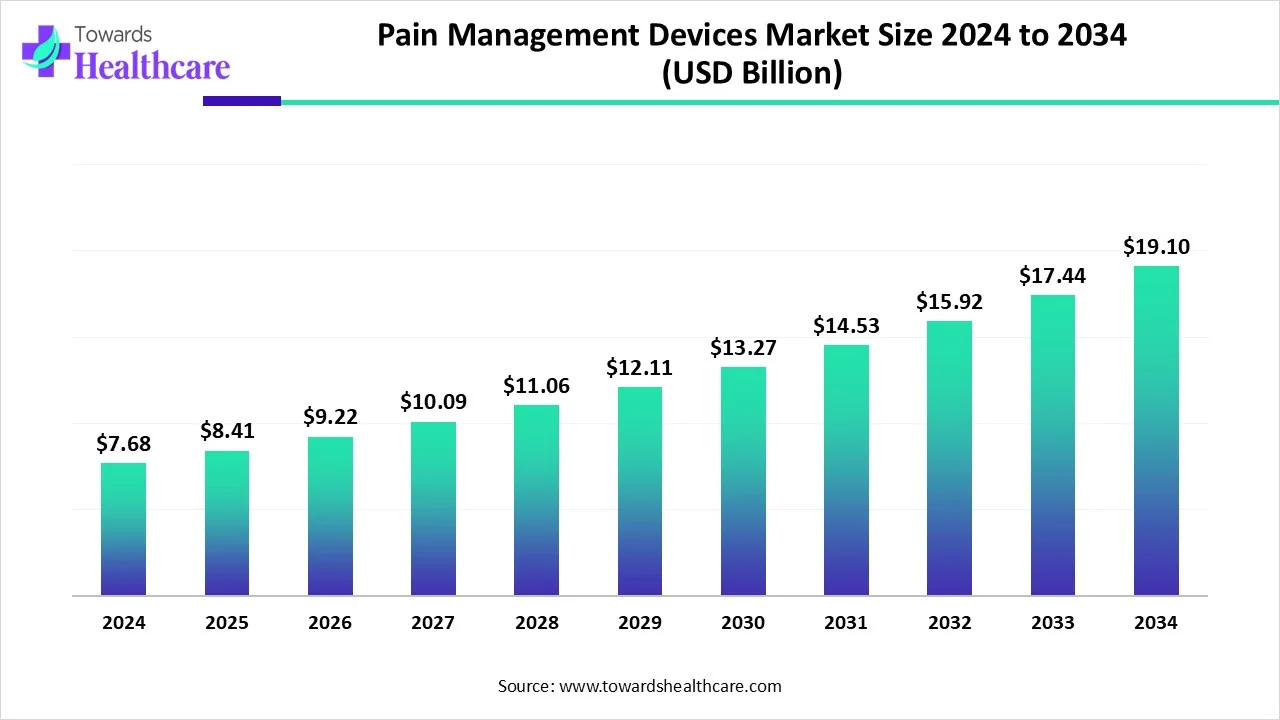

The global pain management devices market was valued at USD 7.68 billion in 2024, grew to USD 8.41 billion in 2025, and is forecast to reach ≈ USD 19.1 billion by 2034 — expanding at a 9.54% CAGR (2025–2034) driven by rising chronic-pain prevalence, neuromodulation expansion and demand for minimally invasive solutions.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5742

Market size

Historical / near-term numbers (anchor data):

• 224 market value: USD 7.68B.

• 2025 market value: USD 8.41B.

Long-term projection:

• Forecast for 2034 ≈ USD 19.1B, reflecting tech adoption, wider reimbursement access and more minimally invasive therapies.

Growth rate:

• CAGR 2025–2034: 9.54% — indicates a sustained, above-average expansion vs many medtech segments.

Regional skew (high-level):

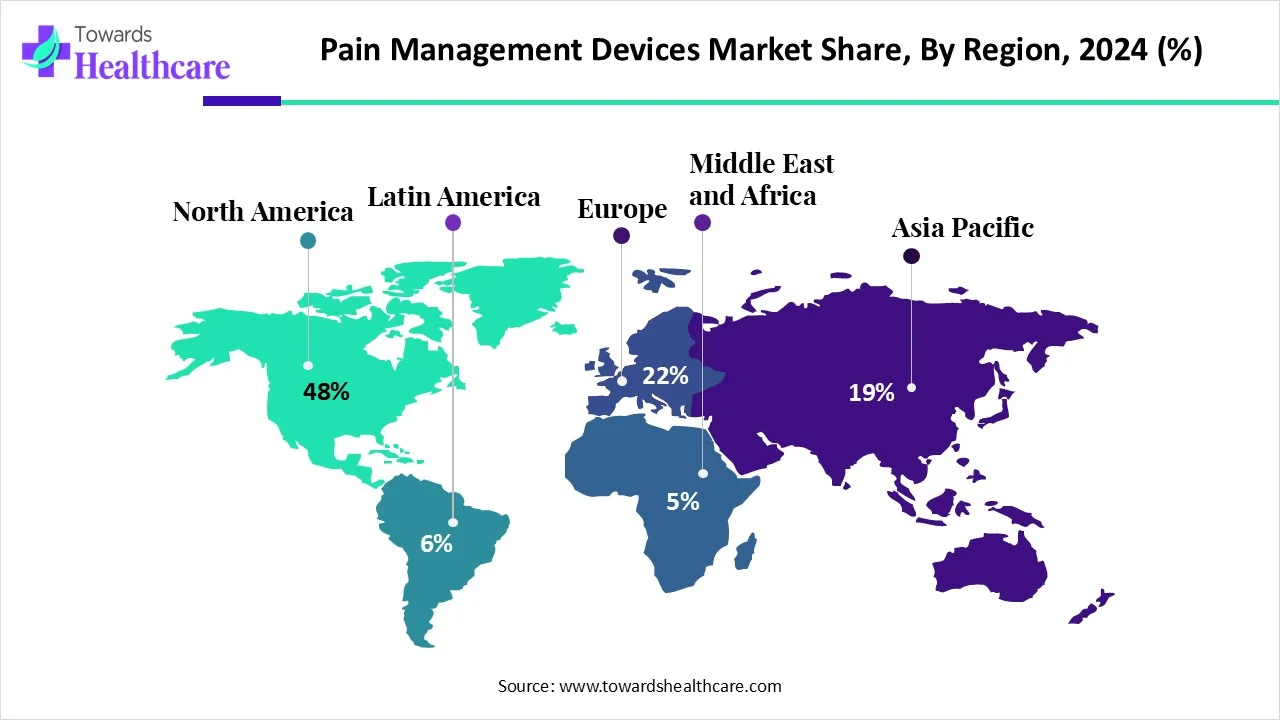

• North America dominated in 2024 (48% of revenue) — driven by strong reimbursement, R&D and high adoption of neurostimulation and RFA.

• Asia-Pacific expected fastest CAGR going forward — rising healthcare spend, aging populations and medtech startups.

Market concentration:

• Mix of large diversified device players (Abbott, Boston Scientific, Stryker, etc.) plus scale-up specialists (Nevro, NeuroOne, Zynex, SPR Therapeutics) — meaning strategic M&A and partnerships are likely as big players fill capability gaps.

Market trends

Shift to neuromodulation (dominant product class): neurostimulation led the market in 2024 due to both implantable and non-implantable options and strong clinical outcomes for chronic neuropathic pain.

Radiofrequency ablation (RFA) adoption accelerating: RFA is expected to be the fastest-growing product segment — perceived as effective, minimally invasive and increasingly affordable.

Non-opioid treatment emphasis: a global move to reduce opioid dependence increases demand for device-based options (TENS, neurostimulation, RFA, infusion pumps).

Digital + remote care integration: wearables, sensors and remote-monitoring platforms are being bundled with devices for better longitudinal pain tracking.

AI/ML inclusion in device platforms: AI is being embedded to optimize stimulation parameters, detect patterns and enable closed-loop control (see AI section below).

Regulatory momentum for targeted ablation/stimulation: more 510(k)/CE clearances for novel ablation and neurostimulation platforms (examples: NeuroOne, Zynex).

Commercial scale-up via funding rounds: startups with differentiated tech (closed-loop SCS, implantable drug systems) have attracted large capital raises to commercialize — e.g., Saluda’s $100M financing for Evoke commercialization.

Shift to outpatient & physiotherapy channels: shorter stays, outpatient RFA and growth of physiotherapy centers as end-use segments.

Patient personalization & biomarkers: objective neuromodulation biomarkers and patient-specific dosing (closed-loop) are gaining traction.

Reimbursement & health policy shaping uptake: favorable reimbursement in NA and some EU markets accelerates adoption; gaps in LMICs slow it down.

AI: 10 deep roles / impacts for this market

Closed-loop stimulation optimization (real-time dosing):

• AI models process evoked neural signals (e.g., ECAPs) to automatically adjust stimulation amplitude/frequency to maintain therapeutic targets — reducing manual programming time and improving consistency of relief. (Directly ties to closed-loop SCS like Evoke.)

Predictive patient responder models (trial selection):

• ML classifiers trained on clinical, imaging and intraoperative biomarkers can predict which patients will respond to SCS/RFA/TENS — increasing trial success and lowering unnecessary implants.

Personalized therapy profiles (longitudinal adaptation):

• AI ingests wearable and patient-reported pain logs to adapt device programs over days/weeks to match circadian patterns, activity and analgesic needs.

Anomaly detection & device safety monitoring:

• Unsupervised AI flags unusual electrical signatures, lead migration indicators or early battery degradation — enabling preemptive clinic interventions and fewer complications.

Dose-response modeling for RFA & ablation planning:

• Simulation models estimate lesion size and nerve targeting for RFA using patient anatomy to optimize thermal dosing while minimizing collateral damage.

Augmented programming UI for clinicians:

• Explainable AI suggests parameter sets, ranks options by predicted pain reduction and shows expected side-effect probabilities — speeding clinic visits and making programming accessible to more providers.

Remote triage & adherence monitoring:

• AI analyzes home TENS/wearable usage and pain diaries to triage patients for follow-up, improving outcomes and reducing unnecessary appointments.

Real-world evidence generation & regulatory support:

• Federated learning on anonymized device telemetric data can produce regulatory-grade safety/effectiveness evidence across geographies without centralizing PHI.

AI-enabled imaging guidance for minimally invasive placement:

• ML assists fluoroscopy/ultrasound interpretation to guide percutaneous lead placement or subcutaneous implant insertion, improving accuracy and shortening procedures.

Cost-effectiveness & reimbursement analytics:

• Health-economic models using AI estimate long-term cost offsets (reduced opioid use, fewer hospitalizations) to strengthen reimbursement submissions and payer discussions.

Regional Insights

1. North America — Market Leader (48% Share in 2024)

Key Drivers

Mature reimbursement environment:

➣U.S. Medicare and private insurers increasingly reimburse for spinal cord stimulation (SCS), radiofrequency ablation (RFA), and peripheral nerve stimulation (PNS).

➣Widespread coding and coverage pathways lower economic barriers for providers and patients.

High R&D intensity and innovation ecosystem:

➣Concentration of leading companies (Abbott, Boston Scientific, Nevro, Stryker) drives continuous technological upgrades.

➣Universities and pain research centers maintain a strong clinical innovation pipeline.

Rapid adoption of neuromodulation & RFA systems:

➣Clinicians have early access to advanced closed-loop and high-frequency devices, accelerating adoption in both chronic and acute pain management.

Clinical Pipeline

Dense trial activity:

➣North America leads in pain device clinical trials, accounting for nearly half of ongoing global neuromodulation studies.

➣Continuous trial outcomes accelerate evidence-based device adoption and FDA clearances.

Commercial Dynamics

Presence of strong medtech incumbents:

➣Established players with robust distribution networks ensure wide market coverage.

Venture capital flow and startup activity:

➣Venture-backed innovators (e.g., Saluda Medical, Mainstay Medical) drive niche solutions for specific pain disorders.

➣Active M&A landscape integrates early-stage neurotech startups with large medtech firms, speeding commercialization.

2. Europe — Stable but Fragmented Market

Key Drivers

Extensive hospital and rehabilitation networks:

➣Large public hospital systems and integrated pain clinics facilitate access to device-based therapies.

Public payer support for proven technologies:

➣Cost-effectiveness and quality-of-life data drive reimbursement for established interventions like SCS and RFA.

Barriers

Heterogeneous reimbursement systems:

➣Each EU country maintains distinct payer frameworks, complicating cross-border pricing and adoption.

➣Some regions (e.g., Southern and Eastern Europe) lag in funding compared to Western Europe.

Procurement complexity:

➣Public tender systems can delay new technology introduction.

Market Landscape

Localized ecosystem:

➣Mid-size and local players (e.g., Polar Medical, GBUK in the UK) focus on niche products and procedural consumables.

➣EU MDR regulations tighten device certification but ensure quality and safety compliance.

3. Asia-Pacific — Fastest-Growing Market (Highest CAGR)

Key Drivers

Expanding healthcare infrastructure:

➣Rapid modernization of hospitals in China, India, and Southeast Asia enables broader adoption of advanced pain therapies.

Large patient population:

➣High prevalence of back pain, osteoarthritis, and diabetic neuropathy drives sustained clinical demand.

Supportive regulatory momentum:

➣Streamlined approval processes in Japan, Australia, and India shorten device entry timelines.

Emerging medtech hubs:

➣Local manufacturing and innovation clusters in China and Singapore enhance accessibility and affordability.

Opportunities

Cost-effective device adoption:

➣Lower per-procedure costs encourage adoption of RFA and TENS in mid-tier hospitals.

Home-based and remote care expansion:

➣Growing digital penetration supports portable and connected device use for home physiotherapy.

Physiotherapy network expansion:

➣Rapidly growing rehabilitation centers in India and Southeast Asia drive distributed demand for non-invasive pain devices.

Challenges

Uneven reimbursement landscape:

➣Reimbursement remains limited or inconsistent in low- and middle-income countries (LMICs).

Affordability gaps:

➣High-end neuromodulation systems remain inaccessible for large segments of the population.

4. Latin America — Emerging but Constrained Growth

Key Drivers

Rising burden of chronic pain:

➣Increasing incidence of back and musculoskeletal pain, particularly in aging urban populations.

Investment from global medtech players:

➣Multinational firms (Abbott, Boston Scientific) are expanding local assembly and distribution networks in Brazil and Mexico.

Barriers

Healthcare infrastructure gaps:

➣Limited access to advanced surgical pain procedures outside major cities.

Reimbursement constraints:

➣Public insurance coverage remains narrow, and private care affordability limits patient volumes.

Regional Outlook

➣Gradual improvement expected through partnerships between global firms and local distributors to expand product access.

5. Middle East & Africa (MEA) — Niche but Growing Market

Key Drivers

Expansion of private healthcare infrastructure:

➣Rapid growth in urban centers such as Dubai, Riyadh, and Johannesburg supports adoption of advanced pain devices.

Centers of excellence:

➣Select tertiary hospitals are introducing neuromodulation and RFA systems for chronic pain and oncology-related conditions.

Barriers

Limited access outside metropolitan regions:

➣Rural and lower-income areas have minimal exposure to advanced therapies.

Regulatory variability:

➣Inconsistent import policies and slow product registration processes extend commercialization timelines.

Market Dynamics

Primary Drivers

1. Rising Prevalence of Acute and Chronic Pain

Expanding patient base: Aging populations, sedentary lifestyles, and obesity are contributing to a sharp rise in chronic musculoskeletal and neuropathic pain cases.

Comorbidity link: Conditions such as diabetes, osteoarthritis, and spinal disorders significantly increase the chronic pain burden.

Epidemiological evidence: Global back pain remains one of the top causes of disability, with the WHO estimating that nearly 1 in 6 adults experience chronic pain lasting over three months.

Sustained device demand: The persistent nature of pain management needs drives steady adoption of implantable and external pain relief systems such as SCS, RFA, and TENS.

2. Technological Advancements in Neuromodulation and Closed-Loop Systems

Closed-loop feedback systems: Innovations like Evoke and other adaptive SCS technologies automatically adjust stimulation based on real-time feedback from the spinal cord, improving outcomes.

Next-generation RF generators: New platforms (e.g., OneRF by NeuroOne) offer precision ablation and shorter recovery times.

Integration of AI and remote programming: Enables clinicians to fine-tune therapies remotely, improving therapy personalization and adherence.

Result: Higher efficacy and patient satisfaction are accelerating both device replacement cycles and new patient adoption rates.

3. Economic and Policy Shift from Opioid to Device-Based Therapies

Policy pressure: Global and national health authorities are promoting non-opioid pain management due to the opioid misuse epidemic.

Clinical preference: Physicians increasingly prefer interventional or device-based treatments that minimize dependency risks.

Payer acceptance: Gradual expansion of reimbursement frameworks for non-pharmacological pain solutions in the U.S. and Europe.

Outcome: Device-based pain therapies (SCS, RFA, PNS) are becoming mainstream for chronic pain management.

Restraints

4. High Procedural and Device Cost

Upfront cost barrier: Advanced implants and ablation systems can cost thousands per unit; combined with surgical procedure expenses, this limits initial uptake.

Reimbursement gaps: Inconsistent or partial coverage across regions (especially in emerging markets) restricts market expansion.

Economic impact: Hospitals and clinics face cost-containment pressures, often delaying technology upgrades or replacements.

5. Technical Complexity and Training Requirements

Skill-intensive procedures: Implanting neurostimulation or RF systems requires trained specialists—often pain physicians, neurosurgeons, or anesthesiologists.

Programming expertise: Effective therapy delivery depends on post-implant programming and monitoring, which adds complexity.

Workforce limitation: Shortage of trained clinicians, particularly in Asia-Pacific and Latin America, slows the adoption curve.

Opportunities

6. Rise of Minimally Invasive and Outpatient Procedures

Procedure shift: Growing adoption of radiofrequency ablation (RFA), TENS, and peripheral nerve stimulation (PNS) devices in outpatient settings.

Economic benefit: Reduced hospital stay and lower per-case costs make these attractive for both patients and payers.

Accessibility: Portable and wearable devices are expanding access to non-invasive pain relief, especially in ambulatory and home-care settings.

7. Digital Therapeutics and Connected Care Integration

Technology convergence: Pairing neuromodulation devices with mobile apps, wearable sensors, and AI-driven analytics for real-time feedback.

Enhanced engagement: Digital platforms (e.g., JOGO Health) improve patient adherence and enable remote therapy adjustments.

Value-based models: Enables new payer partnerships where reimbursement ties to patient outcomes and engagement metrics.

8. Emerging Markets and Physiotherapy Channel Expansion

Market penetration: Rapid growth in physiotherapy and rehabilitation networks in Asia-Pacific, Latin America, and the Middle East.

Decentralized care: Adoption of TENS and portable nerve stimulation devices supports at-home and clinic-based pain management.

Volume opportunity: Expanding healthcare access and awareness campaigns boost demand for cost-effective, non-invasive devices.

Regulatory Dynamics

9. Positive Regulatory Momentum

Accelerated approvals: U.S. FDA 510(k) and European CE mark pathways remain supportive of iterative innovations in pain devices.

Recent clearances:

Zynex TensWave (FDA-cleared, Sep 2024)

NeuroOne OneRF ablation platform (FDA-cleared, 2025)

Impact: Encourages continuous R&D investment and faster commercialization cycles, particularly for digital and energy-based devices.

Consolidation and Strategic Partnerships

10. Industry Consolidation and Cross-Sector Collaborations

M&A trend: Larger medtech firms are acquiring or partnering with digital health and neurotech startups to expand portfolios (e.g., Abbott, Boston Scientific).

Strategic intent: Combines scale, distribution reach, and niche innovation for competitive advantage.

Emerging alliances: Pharma companies (e.g., Novartis) are collaborating with device makers for combination therapies targeting chronic pain and neurological conditions.

Outcome: Ecosystem convergence between traditional medtech and digital health accelerates integrated care delivery.

Top 10 companies

Abbott Laboratories

Product Focus: Implantable neuromodulation systems, spinal cord stimulation (SCS).

Overview: Diversified medtech leader with a strong neuromodulation and diagnostics portfolio.

Strength: Global footprint, established payer relationships, and broad R&D capabilities.

Avanos Medical

Product Focus: Pain therapy disposables and infusion systems.

Overview: Focuses on procedure-adjacent medical devices, especially in pain management.

Strength: Deep penetration in operating rooms and hospital channels.

Boston Scientific Corporation

Product Focus: Spinal cord stimulation and peripheral nerve stimulation systems.

Overview: Established player in electrophysiology and neurostimulation markets.

Strength: Backed by strong clinical evidence and a robust global sales network.

Endo International plc

Product Focus: Analgesic infusion pumps and interventional pain therapies.

Overview: Offers interventional pain management solutions, transitioning from a pharma-driven portfolio.

Strength: Expertise in specialty pain markets and chronic pain interventions.

JOGO Health

Product Focus: Digital therapeutics integrated with connected medical devices.

Overview: Emerging player blending technology and care delivery for pain and rehab management.

Strength: Agility in digital patient engagement and personalized therapy platforms.

LivaNova

Product Focus: Neuromodulation platforms for neuro and cardiac applications.

Overview: Specialized in neurotechnology and stimulation-based treatment systems.

Strength: Strong engineering depth and extensive regulatory experience.

NeuroOne Medical Technologies Corporation

Product Focus: OneRF ablation platform for trigeminal and other nerve ablations.

Overview: Developer focused on targeted ablation technology for complex pain conditions.

Strength: Platform aimed at hard-to-treat facial pain; OneRF recently received FDA clearance.

Nevro Corp

Product Focus: High-frequency spinal cord stimulation systems.

Overview: Pioneer in high-frequency therapy for chronic pain management.

Strength: Proprietary HF10 waveform technology with proven superior clinical outcomes.

Novartis AG

Product Focus: Device-drug combination therapies (emerging focus).

Overview: Global pharma giant exploring medical device partnerships to enhance therapeutic delivery.

Strength: Vast commercialization infrastructure and strategic investment capability.

SPR Therapeutics, Inc. / Zynex, Inc. / Stryker Corporation

Product Focus:

SPR Therapeutics: Peripheral nerve stimulation.

Zynex: TENS and TensWave therapy devices.

Stryker: Radiofrequency ablation (RFA) generators.

Overview: Each focuses on specialized pain management technologies with rapid go-to-market models.

Strength: Niche product expertise and fast commercialization; Zynex’s TensWave received FDA clearance (Sep 2024).

Latest announcements

NeuroOne — OneRF Trigeminal Nerve Ablation (FDA activity): NeuroOne filed for/received FDA 510(k) clearance for its OneRF Trigeminal Nerve Ablation System which enables minimally invasive RF lesioning for trigeminal neuralgia / facial pain. The clearance validates the OneRF RF generator platform and supports late-2025 limited commercial launches for a targeted facial-pain indication (offers an alternative to more invasive surgical options).Zynex — TensWave FDA clearance (Sept 2024): TensWave — a portable prescription-only TENS device — obtained FDA clearance, supporting non-pharmacologic chronic and acute pain management at home or clinic. This expands non-invasive device offerings and outpatient options.

Saluda Medical — $100M financing (Jan 2025): Saluda closed a $100M financing to commercialize its Evoke closed-loop spinal cord stimulation system (Evoke senses neural responses and auto-adjusts dosing), accelerating closed-loop SCS adoption. This capital supports scale-up and commercial footprint expansion.

Stryker India — MultiGen 2 RFA launch commentary: Stryker announced MultiGen 2 radiofrequency generator as its next-gen RFA platform focused on control and customization for chronic facet-joint pain — aiming at higher efficiency and clinician confidence (regional launch emphasis noted). (supplier commentary referenced in your content.)

Recent developments

Regulatory green lights for new modalities (Zynex, NeuroOne): FDA clearances for devices across the spectrum (portable TENS to targeted nerve ablation) expand the clinical toolkit and validate non-drug / minimally invasive approaches — which should boost clinician confidence and payer consideration.

Venture & growth capital fueling commercialization (Saluda $100M): significant financing rounds let startups scale sales, training, and post-market evidence gathering — accelerating clinician awareness and uptake of closed-loop neuromodulation.

Platform convergence (neurostimulation + AI + sensors): device vendors are layering software intelligence, remote monitoring and objective biomarkers into devices to differentiate value propositions and support reimbursement.

More outpatient & home-based device options: approvals for portable devices and better peri-procedure workflows enable de-hospitalization of many pain interventions (cost and access benefits).

Clinical evidence maturing: randomized and long-term follow-up data for closed-loop SCS and high-frequency SCS strengthen clinical guidelines and payer dossiers.

Segments covered

1. By Product (Major Groupings)

a) Neurostimulation

Types:

➣Spinal Cord Stimulators (SCS)

➣Deep Brain Stimulators

➣Sacral Neurostimulators

➣Peripheral Nerve Stimulators (PNS)

Explanation:

➣These devices use implantable or external electrodes to modulate neural pathways and interfere with pain signaling.

➣Provide targeted relief for chronic neuropathic pain, failed back surgery syndrome, and complex regional pain syndromes.

Key Advantage: Minimally invasive compared to surgery; avoids long-term opioid dependence.

Market Relevance:

➣Dominated the global pain management device market in 2024 due to clinical efficacy and technological advancements such as closed-loop SCS systems.

b) Radiofrequency Ablation (RFA)

Components:

➣RF generators

➣Lesioning probes

Explanation:

➣Uses controlled heat energy to ablate or interrupt nerve conduction.

➣Commonly used for facet joint pain, osteoarthritis-related pain, and peripheral neuropathic conditions.

Key Advantage: Durable relief with minimal recovery time; outpatient applicability.

Market Relevance:

➣Expected to witness the fastest growth among product segments due to simplicity, effectiveness, and increasing adoption in minimally invasive procedures.

c) Electrical Stimulators / TENS

Types:

➣Portable home-use TENS units

➣Clinic-based prescription stimulators (e.g., TensWave)

Explanation:

➣Non-invasive devices apply electrical pulses to nerves to reduce pain perception.

➣Suitable for musculoskeletal pain, post-surgical pain, and rehabilitation programs.

Key Advantage: Safe, drug-free analgesia; ideal for outpatient and home-care settings.

Market Relevance:

➣Increasing preference for non-invasive pain solutions and rising awareness of home-care interventions drive adoption.

d) Analgesic Infusion Pumps

Types:

➣Intrathecal infusion pumps (implantable)

➣External infusion pumps

Explanation:

➣Deliver continuous localized analgesics or opioids to manage refractory chronic or cancer-related pain.

Key Advantage: Provides steady pain relief, reduces systemic drug exposure, and is suitable for severe or intractable pain.

Market Relevance:

➣Targeted for specialized hospitals and clinics; adoption is driven by oncology care and advanced pain management programs.

2. By End-Use

a) Hospitals & Clinics

Explanation:

➣Account for the largest revenue share globally.

➣Offer multidisciplinary expertise, surgical capabilities, and infrastructure for advanced procedures like SCS implantation and RFA.

➣Provide access to clinical trials for novel devices and AI-enabled therapies.

Market Insight:

➣Favorable reimbursement policies in North America and Europe further support adoption in hospitals.

b) Physiotherapy & Rehabilitation Centers

Explanation:

➣Serve as outpatient hubs for non-invasive or wearable device therapies.

➣Growing adoption of TENS, portable neurostimulators, and digital therapeutics integrated with apps.

Market Insight:

➣Projected to exhibit the fastest CAGR due to expanding physiotherapy networks, rising home-care adoption, and patient preference for minimally invasive solutions.

c) Others

Includes: Ambulatory surgical centers, home care setups, and specialty clinics.

Explanation:

➣Provide decentralized access to non-invasive pain devices and short-stay interventions.

➣Play a crucial role in increasing patient convenience and reducing hospital load.

3. By Region

a) North America

Market Share: 48% in 2024 (dominant).

Drivers:

➣Advanced reimbursement frameworks, high R&D intensity, early adoption of neuromodulation and RFA.

Insights:

➣High clinical trial activity ensures evidence generation and rapid adoption.

➣Strong medtech incumbents support commercialization, supplemented by venture-backed startups like Saluda Medical.

b) Europe

Drivers:

➣Extensive hospital networks and public payer support for cost-effective therapies.

Barriers:

➣Fragmented reimbursement across countries; reliance on local suppliers (Polar Medical, GBUK) for niche markets.

c) Asia-Pacific

Growth Potential: Fastest CAGR expected.

Drivers:

➣Rising healthcare spend, large patient population, improved regulatory pathways, emerging medtech hubs.

Opportunities:

➣Adoption of home-based monitoring, wearable devices, and physiotherapy network expansion.

Challenges:

➣Variable reimbursement, affordability constraints in LMICs.

d) Latin America

Drivers:

➣Rising chronic pain prevalence and investment by global firms establishing local manufacturing.

Barriers:

➣Infrastructure gaps and limited reimbursement.

e) Middle East & Africa (MEA)

Drivers:

➣Growth in private urban healthcare centers, adoption of high-end neuromodulation.

Barriers:

➣Limited access outside major urban centers; inconsistent regulatory pathways.

Top 5 FAQs

-

Q: What was the market size in 2024 and the forecast for 2034?

A: The market was USD 7.68B in 2024 and is forecast to reach ≈ USD 19.1B by 2034 (CAGR 9.54% between 2025–2034). -

Q: Which region led the market in 2024?

A: North America held the largest share in 2024 (48%). -

Q: Which product segment dominated in 2024?

A: Neurostimulation led in 2024 due to both implantable and non-implantable device adoption. -

Q: What are the fastest-growing segments?

A: Radiofrequency ablation (RFA) and physiotherapy center end-use are projected to grow fastest, reflecting demand for minimally invasive outpatient treatments. -

Q: Any notable recent FDA/regulatory actions?

A: Yes — Zynex’s TensWave received FDA clearance (Sept 2024) and NeuroOne’s OneRF trigeminal ablation system received FDA 510(k) clearance (2025/2025 filings → clearance). These approvals expand non-opioid device options.

Access our exclusive, data-rich dashboard dedicated to the medical devices – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5742

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest