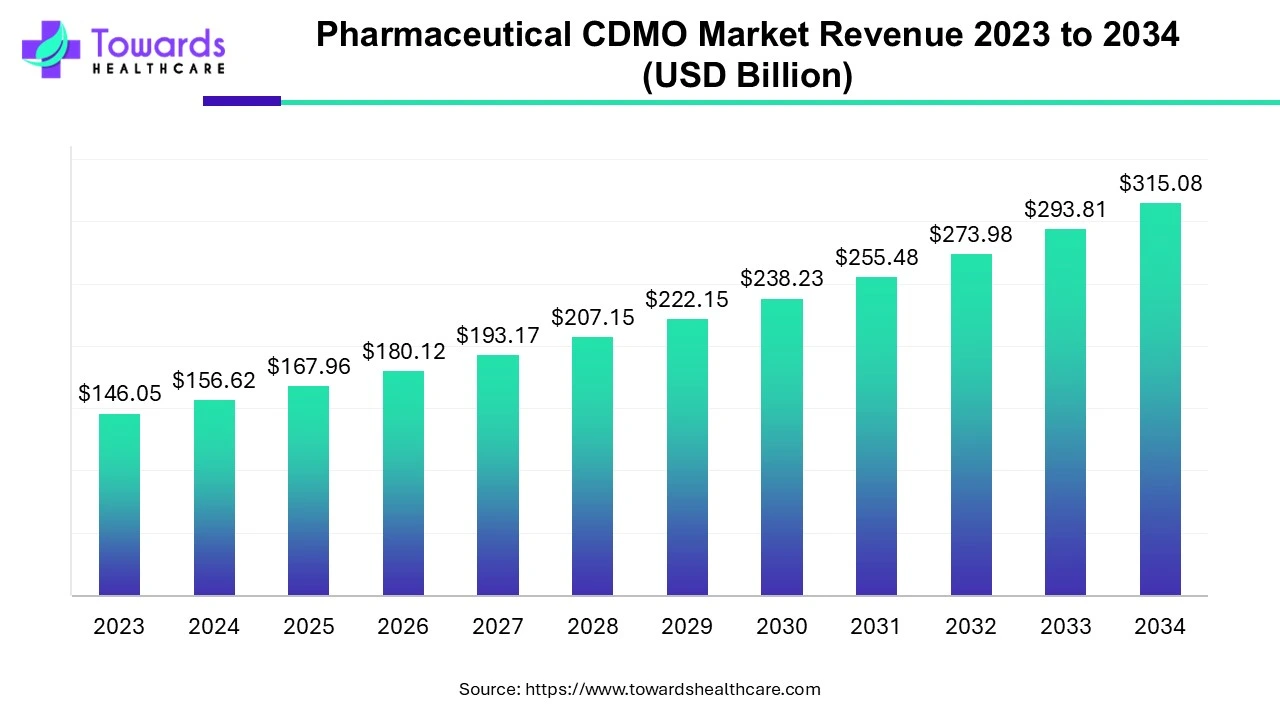

The global Pharmaceutical CDMO Market is poised for significant growth, with projections indicating an increase from USD 146.05 billion in 2023 to approximately USD 315.08 billion by 2034. This expansion represents a compound annual growth rate (CAGR) of 7.24% from 2024 to 2034. This comprehensive analysis delves into the factors driving this growth, emerging trends, regional dynamics, market segments, challenges, and key players shaping the industry.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5327

Market Overview

Market Definition and Role of CDMOs

Pharmaceutical CDMOs are specialized entities that provide comprehensive services encompassing drug development, manufacturing, and commercialization. They play a pivotal role in the pharmaceutical supply chain by offering expertise, scalability, and regulatory compliance, thereby enabling pharmaceutical companies to focus on core competencies such as research and development.

Market Growth Drivers

Several factors contribute to the robust growth of the pharmaceutical CDMO market:

Rising Demand for Pharmaceuticals: Increased global healthcare needs drive the demand for pharmaceutical products, necessitating efficient manufacturing solutions.

Advancements in Biotechnology: The surge in biologic drug development requires specialized manufacturing capabilities, positioning CDMOs as essential partners.

Cost-Efficiency and Scalability: Outsourcing to CDMOs allows pharmaceutical companies to reduce capital expenditures and scale operations effectively.

Market Trends

➤Strategic Collaborations and Investments

Strides Pharma Science: In October 2024, Strides Pharma Science reported that during the pre-listing phase, both domestic and overseas institutional investors committed Rs 801 crore in equity to its affiliate company.

Lifera Initiative: In June 2023, Saudi Arabia’s Public Investment Fund introduced Lifera, a commercial-scale CDMO aimed at enhancing the nation’s pharmaceutical manufacturing capabilities.

Pharmaron’s Expansion: In March 2023, Pharmaron invested £151 million in a UK Gene Therapy CDMO to expand its facilities for producing viral vectors and DNA by over 8,000 square meters.

➤Personalized Medicine

The growing emphasis on personalized medicine necessitates tailored manufacturing processes. CDMOs are increasingly focusing on small-scale, complex projects that maintain efficacy, safety, and reliability, catering to the individualized treatment needs of patients.

➤Technological Advancements

The integration of digital automation, continuous manufacturing processes, and advanced analytics is transforming CDMO operations. These innovations enhance efficiency, reduce lead times, and improve product quality.

Regional Insights

Asia-Pacific

➤Market Leadership: Asia-Pacific dominated the pharmaceutical CDMO market in 2023, driven by cost-effective production capabilities and a robust pharmaceutical industry in countries like China, India, and Japan.

➤China’s Dominance: In 2023, China held the largest share of the pharmaceutical CDMO market, attributed to expanding collaboration agreements between pharmaceutical firms and CDMOs.

North America

➤Market Dynamics: North America is expected to experience the fastest growth during the forecast period, fueled by increased pharmaceutical R&D expenditures and a strong presence of major market players.

➤Regulatory Environment: The stringent regulatory standards in the U.S. and Canada make CDMOs attractive partners for pharmaceutical companies seeking compliance expertise.

Europe

➤Market Characteristics: Europe accounts for a significant portion of the global CDMO market, with countries like Germany, France, and Switzerland being key contributors.

➤Biologics Focus: There is a growing emphasis on biologics and biosimilars, driving demand for specialized manufacturing services.

Latin America and Middle East & Africa

➤Emerging Markets: While currently smaller markets, regions like Latin America and the Middle East & Africa are witnessing increased investments in pharmaceutical manufacturing infrastructure, presenting opportunities for CDMOs.

Market Segmentation

Pharmaceutical CDMO markets are diverse, with segmentation based on product, workflow, application, and end-use. Each segment presents unique growth opportunities and challenges. Understanding these segments helps pharmaceutical companies and investors identify potential areas for outsourcing and collaboration.

By Product

➤The product-based segmentation of the pharmaceutical CDMO market includes Active Pharmaceutical Ingredients (APIs) and Drug Products (finished dosage forms). These categories play a pivotal role in the supply chain and influence market demand.4.1.1 Active Pharmaceutical Ingredients (APIs)

➤Market Share & Growth: APIs accounted for the largest share of the CDMO market in 2023 and are expected to maintain high growth due to increasing pharmaceutical production worldwide. APIs form the essential component of any drug, and their quality, purity, and manufacturing efficiency directly impact the final product.

Drivers of Growth:

➤Rising R&D activities in both small molecules and biologics.

➤The trend of outsourcing API manufacturing to reduce capital expenditure and operational complexity.

➤Growing demand for high-potency APIs (HP-APIs) and antibody drug conjugates (ADCs) for specialized therapies.

Sub-Segments:

➤Traditional APIs – Standard chemical compounds used in routine medications.

➤Highly Potent APIs (HP-APIs) – Targeted compounds requiring specialized containment and handling due to toxicity at low doses.

➤Antibody-Drug Conjugates (ADC) – Used in oncology, combining monoclonal antibodies with cytotoxic agents.

➤Other Specialized APIs – Niche compounds used for rare diseases or cutting-edge therapies.

Opportunities:

➤The increasing complexity of molecules and rising biologic therapies require CDMOs to provide specialized API production capabilities.

➤Geographical expansion in Asia-Pacific (China, India) enables cost-efficient API production.

Drug Products (Finished Dosage Forms)

➤Market Dynamics: Drug product CDMO services include formulation, development, and large-scale manufacturing of final products ready for patient use. This segment covers oral solids, liquids, semi-solids, and innovative dosage forms.

Drivers of Growth:

➤Rising demand for generic drugs due to patent expirations.

➤Personalized medicine and specialty drugs requiring tailored manufacturing processes.

➤Outsourcing to CDMOs for faster time-to-market.

Key Subcategories:

➤Oral Solid Dosage Forms (OSDs) – Tablets, capsules, and powders. These dominate the market due to wide usage.

➤Semi-Solid Dosage Forms – Creams, ointments, and gels; growth driven by dermatology and topical therapies.

➤Liquid Dosage Forms – Solutions, suspensions, and injectables; essential in pediatric and injectable therapies.

➤Others – Includes innovative delivery forms such as inhalers, nasal sprays, and transdermal patches.

Opportunities:

➤Expansion of biologics and personalized therapies creates demand for specialized drug product manufacturing.

➤Regulatory expertise and quality assurance by CDMOs help pharmaceutical companies meet complex compliance requirements.

By Workflow

➤Workflow segmentation reflects the stage of drug development and manufacturing handled by CDMOs. This includes clinical and commercial manufacturing, highlighting the versatility and scalability of CDMO services.

Commercial Manufacturing

➤Market Significance: Dominated the CDMO market in 2023. Commercial manufacturing involves large-scale production of drugs that have been approved and are ready for market distribution.

Drivers of Growth:

➤Rising demand for generic and biosimilar drugs globally.

➤Outsourcing allows pharmaceutical companies to scale production without investing in large facilities.

➤High-quality CDMO expertise ensures compliance with stringent regulatory requirements (FDA, EMA).

Features:

➤Full-scale production capabilities from batch manufacturing to continuous processes.

➤Integration of automation and digital monitoring to optimize efficiency.

➤Ability to produce both APIs and final dosage forms at commercial scale.

Opportunities:

➤Expansion in emerging markets such as Asia-Pacific and Latin America.

➤Collaboration with large pharmaceutical firms seeking cost-effective production solutions.

Clinical Manufacturing

➤Market Significance: Focuses on manufacturing trial materials for preclinical and clinical phases, including small batches for testing purposes.

Drivers of Growth:

➤Rising investment in new drug development and biologics research.

➤Need for specialized expertise in Good Manufacturing Practices (GMP) for clinical-grade materials.

➤Pharmaceutical companies seeking risk mitigation by outsourcing early-stage manufacturing.

Features:

➤Production of small, highly specialized batches for phase I-III clinical trials.

➤Flexibility to adjust formulations based on trial feedback.

➤Advanced quality control to ensure safety and efficacy for human testing.

Opportunities:

➤Increasing focus on orphan drugs and rare disease therapies that require small-scale, high-quality manufacturing.

➤Integration with AI-driven process optimization and digital supply chain management.

By Application

➤Pharmaceutical CDMOs serve a wide range of therapeutic areas, reflecting the diverse drug development landscape.

Oncology

➤Market Significance: Oncology dominated the application segment in 2023 due to the rising prevalence of cancer and the demand for innovative therapies.

Drivers of Growth:

➤Growth in biologics, targeted therapies, and immuno-oncology.

➤Rising incidence of cancers globally and increasing healthcare expenditure.

➤CDMOs provide specialized manufacturing of cytotoxic APIs and ADCs, ensuring safety and scalability.

Opportunities:

➤Expansion of personalized and precision oncology treatments.

➤Collaboration for gene therapy and immunotherapy development.

Other Therapeutic Areas

Small Molecules: Traditional chemical drugs, widely used for chronic and acute conditions.

Biologics: Complex macromolecule drugs, including proteins, monoclonal antibodies, and vaccines.

Infectious Diseases: Antibiotics, antivirals, and vaccines.

Neurological Disorders: Alzheimer’s, Parkinson’s, and multiple sclerosis treatments.

Cardiovascular Diseases: Blood pressure regulators, statins, and anticoagulants.

Metabolic Disorders: Diabetes, obesity, and thyroid treatments.

Autoimmune Diseases: Rheumatoid arthritis, lupus, and inflammatory bowel disease therapies.

Respiratory Diseases: Asthma, COPD, and inhaled therapies.

Ophthalmology: Eye drops, injectable treatments, and gene therapies.

Gastrointestinal Disorders: Drugs for acid reflux, IBD, and liver diseases.

Hormonal Disorders: Insulin, thyroid, and reproductive hormones.

Hematological Disorders: Anemia, clotting disorders, and rare blood conditions.

Opportunities:

➤Niche therapies and rare disease treatments are driving demand for specialized CDMO services.

➤Increasing adoption of biologics and gene therapies fuels the need for advanced manufacturing facilities.

By End-Use

➤End-use segmentation considers the size and type of pharmaceutical companies leveraging CDMO services, highlighting market dependency on company scale and resources.

Large Pharmaceutical Companies

Market Dominance: Held the largest market share in 2023.

Drivers of Growth:

➤Large R&D budgets allow extensive outsourcing.

➤Ability to manage complex global supply chains and regulatory compliance.

➤Focus on high-volume production, biosimilars, and novel therapies.

Advantages:

➤Access to cutting-edge technology through CDMO partnerships.

➤Ability to negotiate favorable contracts and pricing due to scale.

Medium and Small Pharmaceutical Companies

Market Dynamics: These companies increasingly rely on CDMOs to overcome limitations in manufacturing infrastructure, expertise, and capital.

Drivers of Growth:

➤Need to outsource to reduce costs and focus on drug discovery.

➤Smaller companies are entering niche markets, requiring small-scale, high-quality manufacturing.

Opportunities:

➤Personalized medicine and rare disease treatments provide growth avenues.

➤Partnerships with CDMOs enable faster time-to-market and reduced operational risk.

Challenges in the Pharmaceutical CDMO Market

Intense Competition

➤The proliferation of CDMOs has led to heightened competition, compelling companies to differentiate through service offerings, technological capabilities, and pricing strategies.

Regulatory Compliance

➤Navigating the complex regulatory landscapes across different regions poses challenges for CDMOs, necessitating robust compliance frameworks and continuous monitoring.

Supply Chain Disruptions

➤Global events, such as the COVID-19 pandemic, have underscored vulnerabilities in the pharmaceutical supply chain, prompting CDMOs to enhance resilience through diversified sourcing and inventory management strategies.

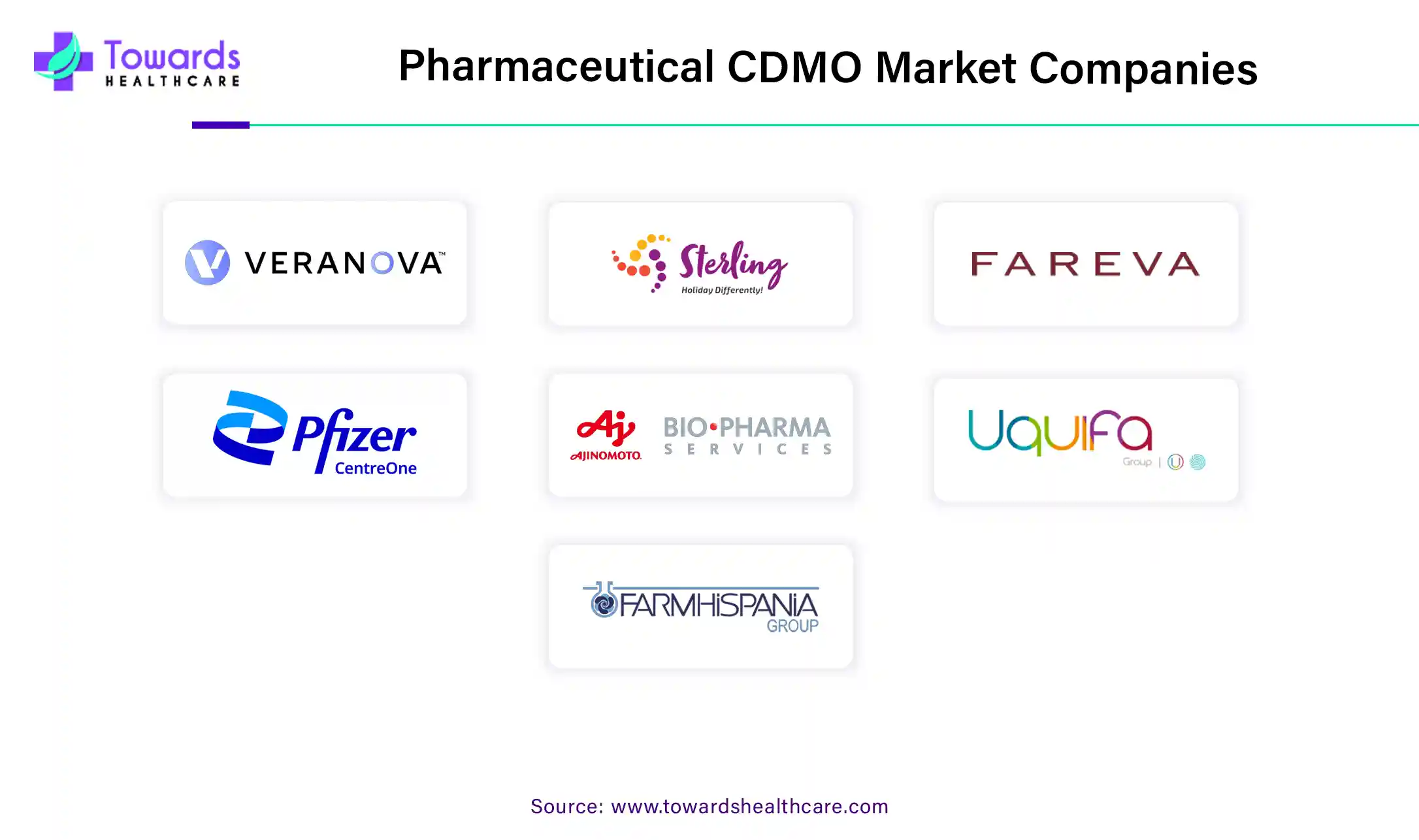

Key Players in the Pharmaceutical CDMO Market

Several companies are at the forefront of the pharmaceutical CDMO industry, driving innovation and setting industry standards:

1. Lonza Group (Switzerland)

Products: APIs, biologics, cell & gene therapies, specialty ingredients.

Role: Full-service CDMO offering end-to-end drug development and large-scale manufacturing; leader in biologics and innovative therapies.

2. WuXi AppTec (China)

Products: Small molecule APIs, biologics, gene & cell therapies, analytical services.

Role: One-stop shop for R&D and manufacturing; reduces time-to-market for pharmaceutical companies.

3. Samsung Biologics (South Korea)

Products: Monoclonal antibodies, recombinant proteins, biologics, biosimilars.

Role: Large-scale biologics manufacturing; supports global pharmaceutical companies with high-capacity production.

4. Catalent, Inc. (USA)

Products: Oral, injectable, respiratory drugs, gene & cell therapies, viral vectors.

Role: Specialized in advanced drug delivery and gene therapy; enables innovative personalized medicine.

5. Rovi (Spain)

Products: APIs, finished dosage forms, sterile injectables, complex formulations.

Role: Growing European CDMO; expanding via acquisitions and tech-driven manufacturing solutions.

Future Outlook

The pharmaceutical CDMO market is set to continue its upward trajectory, driven by:

Technological Innovations: Adoption of advanced manufacturing technologies and digital solutions to enhance efficiency and product quality.

Strategic Partnerships: Collaborations between pharmaceutical companies and CDMOs to streamline drug development and manufacturing processes.

Expansion into Emerging Markets: Increased investments in regions with growing healthcare needs, such as Latin America and the Middle East & Africa.

Recent Industry Developments

Laurus Labs’ Financial Performance

Laurus Labs reported a substantial 1,154% increase in net profit for Q1FY26, reaching ₹163 crore compared to ₹13 crore in Q1FY25. This growth was primarily driven by the robust expansion of its CDMO division, which saw 103% growth due to the execution of multiple new chemical entity (NCE) projects and new manufacturing capacities. The company also announced the commencement of new construction projects, including a gene and antibody drug conjugate facility in Hyderabad and a microbial fermentation facility in Vizag.

Torrent Pharmaceuticals’ Strategic Acquisition

Torrent Pharmaceuticals announced its acquisition of a controlling stake in JB Chemicals from the global private equity firm KKR, valued at approximately $3 billion. This strategic move is expected to strengthen Torrent Pharma’s market position significantly, enhancing its capabilities in the CDMO sector and broadening its product portfolio.

Industry News Highlights

Lonza’s Profit Surge: Swiss pharmaceutical company Lonza reported a 23% increase in its half-year core profit for 2025, surpassing market expectations due to robust performance in its contract drug manufacturing (CDMO) segment.

Rovi’s Expansion Plans: Spanish pharmaceutical company Laboratorios Rovi announced plans to double its CDMO revenues by 2030 through strategic acquisitions and investments in new business.

U.S. Tariff Impact: Shares of Asian pharmaceutical companies declined following U.S. President Donald Trump’s announcement of 100% tariffs on branded drug imports, affecting companies with U.S. exposure

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5327

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest