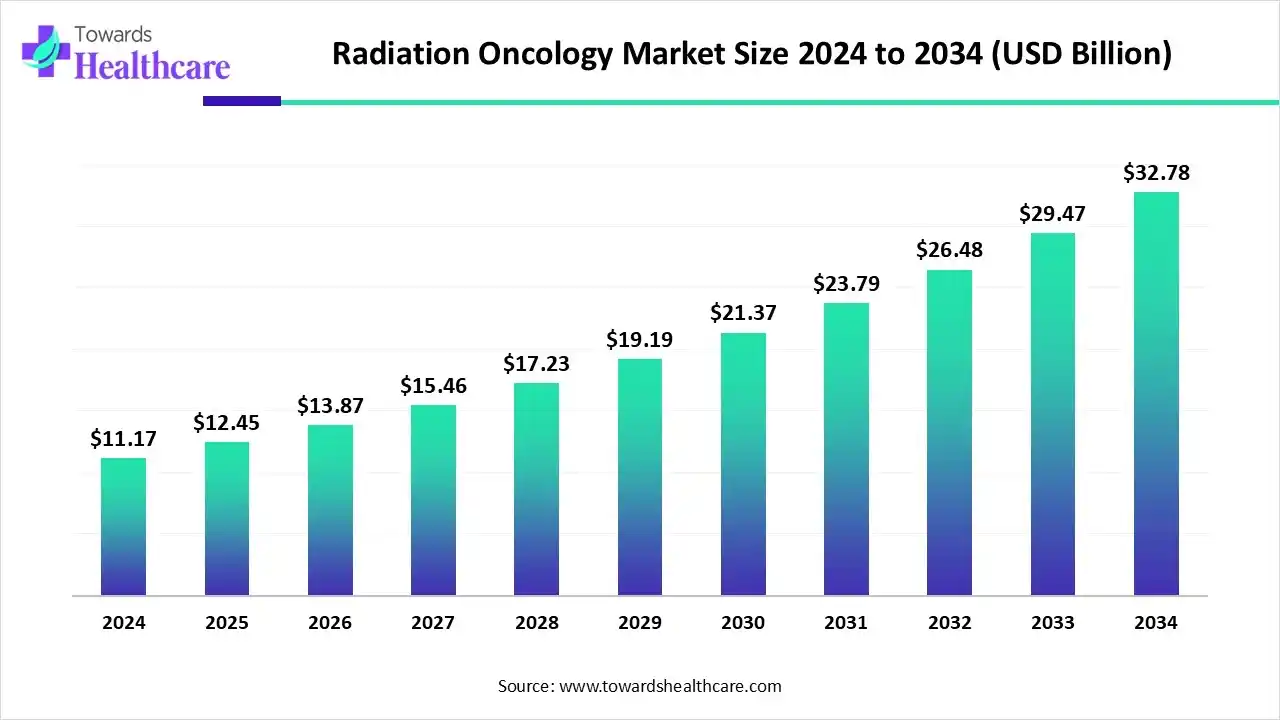

The global radiation oncology market is set to surge from USD 12.45 billion in 2025 to around USD 36.78 billion by 2035, reflecting a robust CAGR of 11.44%, fueled by rising cancer incidence, technological advancements, and growing demand for precise radiation therapy.

Download Free Sample of Radiation Oncology Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/6315

Market Size

2025: Market valued at USD 12.45 billion.

2026: Estimated at USD 13.87 billion, showing early momentum as more institutions adopt radiation therapy.

2035 (Projected): Expected market size of USD 36.78 billion, indicating strong long-term growth potential.

The projected CAGR of 11.44% (2026–2035) underscores consistent expansion over the next decade driven by multiple growth levers.

Market Trends

Rising Cancer Burden: Increasing global incidence of cancer, especially in aging populations, drives demand for radiation treatments.

Greater Awareness & Early Detection: Growing awareness among patients and healthcare systems promotes radiation therapy as a key cancer treatment option.

Government & Private Funding: Support from governments and private institutions facilitates installation of radiotherapy equipment, expanding access especially in emerging markets.

Shift Toward Personalized Therapy: Demand rises for tailored treatment plans, leveraging imaging, advanced planning, and patient‑specific protocols.

Technological Innovation: Advances like proton therapy, radiopharmaceuticals, robotics, and automation enable more precise, less invasive cancer treatments.

Integration of AI & Software Solutions: Treatment‑planning software, AI‑driven dose prediction, and adaptive radiotherapy are becoming core components of modern radiation oncology.

Emergence of Specialized Oncology Centers: Beyond large hospitals, dedicated oncology centers are growing, providing focused care and newer technologies.

Increasing Penetration in Emerging Regions: Asia-Pacific and other developing regions are building infrastructure, expanding access, and fueling market expansion.

Environmental & Sustainability Considerations: A gradual shift toward energy-efficient, eco-conscious radiation therapy systems and practices.

Private Equity & Startup Activity: New investments into startups and technology development are accelerating innovation and broadening the therapy ecosystem.

AI Impact & Role in Radiation Oncology

Automated Treatment Planning — AI tools enable precise, patient-specific radiation dose calculation, reducing human error and speeding up workflow.

Adaptive Radiotherapy — Machine-learning algorithms adjust treatment in real time based on tumor response or patient changes, improving effectiveness.

Image‑Guided Radiotherapy (IGRT) Enhancement — AI improves imaging analysis (like tumor segmentation and location tracking), leading to higher targeting accuracy and less damage to healthy tissue.

Clinical Decision Support — AI aggregates and analyzes patient history, imaging, and tumor data to recommend optimized therapy protocols tailored to individual patients.

Predictive Analytics for Outcomes — AI models forecast patient response and potential side effects, enabling oncologists to personalize treatment intensity and scheduling.

Workflow Automation & Efficiency — Routine tasks (e.g., dose calculations, verification, documentation) are automated, freeing clinicians to focus on patient care and complex planning.

Global Accessibility via Planning Assistants — AI‑driven planning assistants enable regions lacking specialist radiotherapy expertise to access quality treatment plans.

Robotic & Precision Delivery Integration — AI guides robotic systems in delivering radiation with sub-millimetric precision, improving targeting and reducing collateral damage.

Continuous Improvement Through Data — As more patients are treated and data collected, AI systems improve over time, refining protocols and outcomes across populations.

Personalized & Adaptive Cancer Care — AI makes it feasible to move away from one‑size‑fits‑all treatment to personalized, adaptive, evolving cancer therapy regimens per patient.

Regional Insights

North America

Holds a major share (~40–45% in 2024), driven by advanced infrastructure, high healthcare spending, and wide adoption of cutting‑edge radiation technologies.

Strong presence of leading equipment manufacturers and healthcare systems ensures early access to innovations like AI‑guided radiotherapy and proton therapy.

Well-established reimbursement models and regulatory support encourage hospitals and oncology centers to upgrade or install new radiation therapy platforms.

High concentration of cancer research centers and training institutions supports ongoing innovation and deployment of newer modalities.

Asia-Pacific (Including India, China, Australia, etc.)

Fastest growth region projected, due to rising cancer incidence, expanding healthcare infrastructure, and improving access to advanced therapies.

Governments and public-private partnerships investing heavily in radiotherapy centers and awareness campaigns, broadening the patient base.

Adoption of modern technologies (AI planning tools, proton therapy, robotics) gradually increasing, enabling leapfrogging from older radiation therapy standards.

In countries like India — with hundreds of radiotherapy centers and linear accelerators — improved affordability and government-backed programs widen therapy access.

Emerging middle-class populations, increasing screening and detection, and rising health consciousness further amplify demand in coming years.

Europe, Middle East, Latin America & Others

Moderate but steady growth as developed markets upgrade legacy equipment and emerging markets build capacity.

Governments in some European countries investing in advanced research projects (e.g., flash radiation therapy), signaling future-ready oncology care.

Middle Eastern countries and developing nations investing in healthcare infrastructure — offering new markets for radiation oncology equipment and services.

Market Dynamics

Major Drivers: Growing global cancer prevalence, technological advances, increased awareness, and rising healthcare spending.

Restraints/Challenges: High capital costs for advanced radiotherapy equipment; limited access in low-income regions; need for skilled personnel and regulatory compliance.

Opportunities: Integration of AI and automation, expansion in emerging markets, development of novel modalities (proton therapy, radiopharmaceuticals), and rise of specialized oncology centers.

Risks: Cost barriers, uneven access, potential regulatory and safety hurdles, and slow infrastructure development in certain regions.

Investment & Funding Dynamics: Private equity, venture capital, and public-private initiatives fuel startups and product innovation, accelerating market growth.

Competitive Innovation Pressure: Leading companies continually develop new systems and software (multi-modality platforms, AI-based planning, precision delivery) to stay ahead.

Accessibility & Equity Focus: Efforts to democratize radiation therapy — via AI planning assistants, government funding, and infrastructure expansion — especially in underserved regions.

Sustainability & Efficiency Considerations: Growing environmental awareness leads to demand for energy-efficient equipment and resource-conscious therapy protocols.

Patient-Centric Care Shift: Toward personalized, adaptive, precise radiation therapy rather than one-size-fits-all — improving outcomes and reducing side effects.

Healthcare Ecosystem Integration: Collaboration between equipment manufacturers, hospitals, oncology centers, governments, and startups ensures holistic growth and innovation.

Top Radiation‑Oncology Companies: Product Overview & Strength

1. Siemens Healthineers

Product Overview: Siemens provides advanced medical imaging systems (e.g. CT, MRI, molecular imaging) and associated software platforms that support radiation therapy planning and guidance. Their offerings help in diagnostic imaging and in integrating imaging with radiotherapy workflows.

Strength: Their global footprint and long-standing reputation in diagnostic imaging give them an edge in delivering integrated imaging + therapy planning solutions. This helps ensure high accuracy in tumor imaging, planning and follow-up — making radiation therapy more precise and widely adoptable.

2. Elekta AB

Product Overview: Elekta develops and produces radiation therapy and radiosurgery equipment. Their solutions cover clinical management systems, radiation delivery units, and radiosurgery suites for a variety of cancer types.

Strength: Known for a comprehensive, end-to-end radiosurgery and radiotherapy package — from planning and management software to delivery hardware — Elekta’s strength lies in offering mature, reliable systems trusted by many oncology centers globally.

3. Accuray Incorporated

Product Overview: Accuray offers advanced radiotherapy platforms, including their “Radixact” system and the recently launched “Stellar Solution” — a multi-modality radiotherapy platform that supports real-time motion tracking, adaptive protocols, and training and evaluation features.

Strength: Their technology emphasizes precision and flexibility — especially for complex or moving tumors — by combining real-time motion tracking and adaptive protocols. This makes their solutions particularly suited for advanced radiosurgery and high-precision treatments.

4. GE Healthcare

Product Overview: GE Healthcare provides imaging solutions (e.g. radiotherapy CT simulation) and radiopharmaceutical tools to support therapy planning and guidance for radiation oncology. Their “Revolution RT” solution enhances CT simulation accuracy and simplifies workflow for radiotherapy planning.

Strength: Their dual capability — combining diagnostic imaging and radiopharmaceutical solutions — gives GE an advantage in integrated diagnostic + therapy pipelines, leading to more accurate simulations and better-prepared radiation treatments.

5. Canon Medical Systems Corporation

Product Overview: Canon supplies CT-based simulation systems for radiation therapy planning (e.g. “Aquilion Exceed LB” and other simulation tools) that help configure therapy beams, map patient anatomy, and plan radiation delivery accurately.

Strength: Their strength lies in high-quality, accurate simulation imaging — a critical early step that ensures radiation therapy is planned precisely, minimizing damage to surrounding healthy tissue and improving treatment outcomes.

6. Hitachi Ltd.

Product Overview: Hitachi offers radiation therapy and medical imaging equipment, contributing to the hardware and infrastructure used for radiotherapy in hospitals and cancer centers.

Strength: With a global distribution network and backing as an established engineering and medical equipment company, Hitachi provides reliable, widely available radiotherapy infrastructure — enabling broader adoption in diverse geographical markets.

7. ViewRay Inc.

Product Overview: ViewRay specializes in MR-guided radiation therapy systems — combining real-time magnetic resonance imaging with radiation delivery to allow therapists to visualize tumors during treatment and adapt therapy as needed.

Strength: Their MR-guided approach enables dynamic tumor tracking and adaptive therapy — improving targeting accuracy, reducing damage to healthy tissue, and enabling treatment of tumors in challenging or moving locations (e.g. near organs that shift).

8. Mevion Medical Systems

Product Overview: Mevion develops compact and efficient proton therapy systems — delivering particle-based radiotherapy that offers high precision and reduced collateral damage compared to conventional radiation beams.

Strength: Their compact proton therapy solutions make advanced particle therapy more accessible and less infrastructure-intensive — lowering the barrier to proton therapy adoption, especially for centers with limited space or budget for massive installations.

9. Ion Beam Applications (IBA)

Product Overview: IBA is a leading provider of proton therapy systems and related radiation oncology solutions — offering hardware, clinical support, and therapy planning for proton-based cancer treatments.

Strength: With specialization in proton therapy and strong research and clinical collaborations, IBA brings advanced particle therapy capabilities — ideal for tumors requiring highly precise targeting, especially near critical structures.

10. Isoray Inc.

Product Overview: Isoray supplies brachytherapy solutions — internal beam radiation therapy — by providing radioactive seeds, pellets or implants that can be placed inside or near tumors for localized radiation over time.

Strength: Their focus on brachytherapy gives a targeted, localized treatment option for cancers where internal implantation is preferable (e.g. prostate, gynecological cancers), offering high precision with minimal impact on surrounding healthy tissues.

Latest Announcements

September 2025: Launch of Stellar Solution by Accuray — a multi‑modality radiotherapy platform featuring real-time motion tracking, offline adaptive protocols, and integrated treatment and training capabilities — marking a significant step in modular, versatile radiotherapy solutions.

September 2025: Introduction of ExacTrac Dynamic System at SMJC (Malaysia) — provides continuous patient positioning tracking using surface guidance, thermal imaging, and X‑ray monitoring — enabling sub-millimetric precision, critical for moving tumors or sensitive organs.

May 2025: Release of RayStation v2025 by RaySearch Laboratories — automates generation of multiple treatment plans and includes liver ablation guidance — streamlining complex treatment planning and reducing clinician workload.

May 2024: Launch of Revolution RT by GE Healthcare in the U.S. and France — a radiotherapy CT solution designed to improve simulation accuracy and simplify workflow during therapy planning, enhancing precision and treatment readiness.

Recent Developments

Researchers at major cancer centers developed AI models that improve tumor targeting while sparing healthy tissue — advancing the precision and safety of radiation therapy.

Collaboration between Integrated Theranostics Solutions (ITS) and Bridge Oncology to offer end-to-end nuclear medicine and radiation oncology services — broadening access to combined diagnostics and treatment programs.

Rising adoption of robotics and automation in therapy delivery — enabling more consistent, precise, and adaptive radiation treatments, especially for complex or moving tumors.

Growing use of AI-based dose prediction software (like MVisionAI Dose+) for personalized therapy planning — improving outcomes and minimizing over- or under-dosing.

Expansion of global access to radiation therapy via AI planning assistants — especially beneficial in regions with limited radiotherapy specialists, thus democratizing cancer care.

Segments Covered

By Type of Radiation Therapy

External Beam Radiation Therapy (EBRT): Non-invasive therapy delivering radiation externally; widely adopted due to precision, flexibility, and suitability for many cancer types.

Internal Beam Radiation Therapy (Brachytherapy): Involves placing radioactive sources inside or near tumors — enabling highly localized radiation; expected to grow rapidly due to demand for targeted therapy.

Proton Therapy: Advanced particle therapy offering high precision with minimal damage to surrounding tissue — key for tumors near sensitive organs or in pediatric cases.

Radiopharmaceuticals: Involves use of radioactive drugs for therapy — merging nuclear medicine with radiotherapy; offers new modalities for treatment.

By End‑User

Hospitals: The backbone of radiation oncology services, with wide infrastructure, multidisciplinary teams, and high capital investment capability.

Oncology Centers: Specialized centers focusing exclusively on cancer care — likely to grow fastest due to their specialization, newer equipment, and personalized care models.

Ambulatory Surgical Centers (ASCs): Smaller, often outpatient-focused centers that can provide certain radiotherapy services, improving accessibility.

Research & Others: Institutions that contribute to innovation, clinical trials, and development of newer radiation therapy modalities and protocols.

By Region

North America: Mature, high‑capacity infrastructure, early adopters of advanced radiation technologies and AI-driven therapy planning.

Asia-Pacific: Rapidly growing due to increasing healthcare investments, rising cancer incidence, and expansion of radiotherapy access, especially in emerging economies.

Europe, Middle East, Latin America, Africa: Growing steadily as legacy systems are upgraded, newer modalities are introduced, and infrastructure expands; especially relevant where governments prioritize healthcare spending.

Top 5 FAQs

Q1: What defines Radiation Oncology?

Radiation oncology refers to the medical specialty that uses ionizing radiation — via external beams, internal implants (brachytherapy), proton therapy, or radiopharmaceuticals — to treat cancer, aiming to destroy tumor cells, shrink tumors, or relieve symptoms, with precision and minimal damage to healthy tissue.

Q2: How big is the radiation oncology market now and what is its projected growth?

As of 2025, the market is valued at USD 12.45 billion; it’s expected to grow to USD 13.87 billion in 2026 and reach approximately USD 36.78 billion by 2035, representing a CAGR of 11.44%.

Q3: What are the major drivers fueling this market growth?

Key drivers include rising global cancer incidence, increasing awareness and early detection, growth of healthcare infrastructure (especially in emerging markets), technological advancements (AI, proton therapy, radiopharmaceuticals), and growing demand for personalized, precise cancer treatment.

Q4: What types of radiation therapy are covered under this market analysis?

The analysis covers: External Beam Radiation Therapy (EBRT), Internal Beam Therapy (brachytherapy), Proton Therapy, and Radiopharmaceutical-based therapies — addressing a broad spectrum of therapeutic modalities.

Q5: Who are the leading companies and what strengths do they bring?

Leading companies include Siemens Healthineers (imaging + therapy planning), Elekta AB (radiosurgery & therapy equipment), Accuray (multi-modality radiotherapy platforms), GE Healthcare (imaging + radiopharmaceuticals), Canon Medical (simulation CT systems), Hitachi, ViewRay (MR-guided therapy), Mevion and IBA (proton therapy), and Isoray (brachytherapy solutions). Their strengths lie in advanced technology, precision, global distribution, and comprehensive therapy offerings.

Access our exclusive, data-rich dashboard dedicated to the life science industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Radiation Oncology Market Report Now at: https://www.towardshealthcare.com/checkout/6315

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest