Image Credit: News-Medical

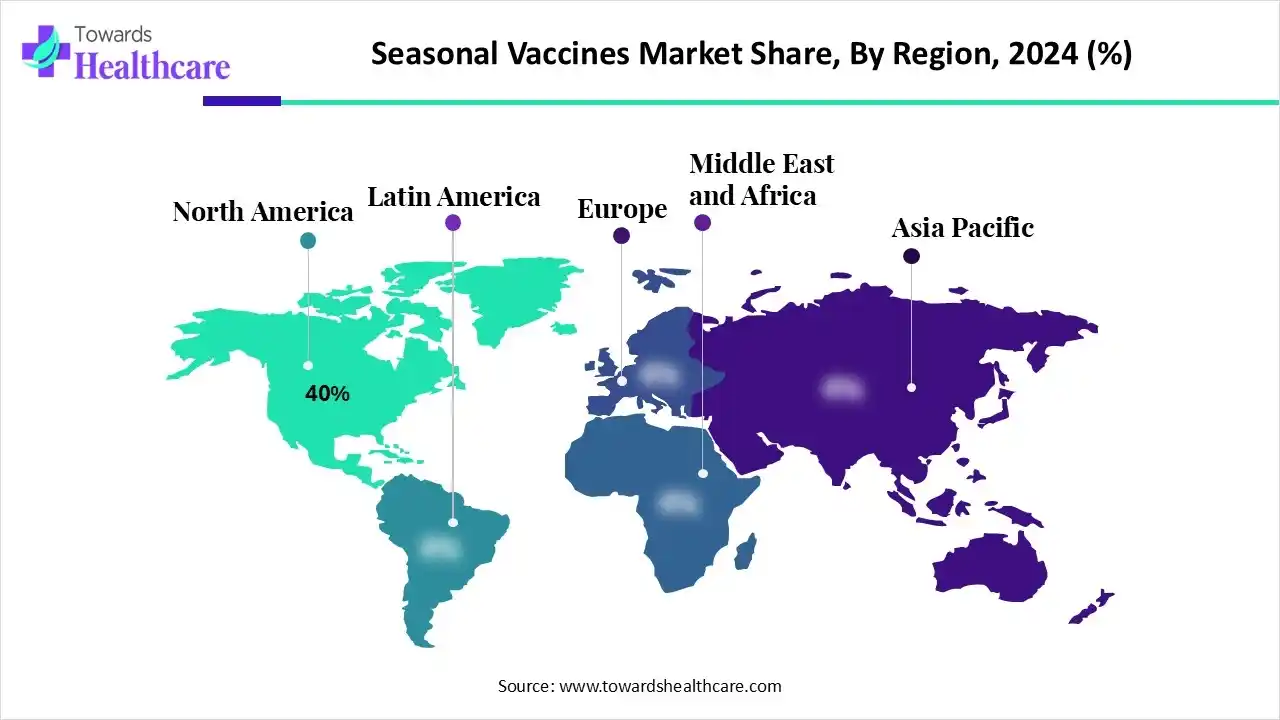

The Seasonal Vaccines Market added hundreds of millions of dollars in revenue (2025–2034) on top of a mature base, led by North America (40% share, 2024), influenza vaccines (60%), intramuscular delivery (70%), and rapid uptake of mRNA platforms across high-need geographies.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6347

Market Size

➤2024 market mix (by major levers):

➤Region: North America 40%; Asia Pacific fastest growth through 2034.

➤Vaccine Type: Influenza 60%; RSV = fastest-growing.

➤Platform: Inactivated/split virion 35% (2024 lead); mRNA = fastest-growing.

➤Route: Intramuscular 70% (2024 lead); Intranasal = fastest-growing.

➤End-user: Public health agencies 45% (2024 lead); Pharmacies/retail = fastest-growing.

Revenue trajectory (2025–2034):

➤Incremental addition: “hundreds of millions” over 2025–2034, driven by RSV launches, annualized COVID-19 boosters, and broader retail vaccination.

➤Volume drivers: Larger eligible cohorts (aging, risk-comorbidities), expanded pediatric/older-adult indications, and combo-vaccine pipelines.

Mix shift implications:

➤Platform tilt to mRNA (speed, strain agility) gradually dilutes inactivated share from 35% as multivalent and combo mRNA programs scale.

➤Channel shift: Retail pharmacies capture a rising share from public programs, compressing administration costs and improving convenience.

Seasonality math checks (demand signals):

➤U.S. 2024–2025 flu testing: 3,978,954 specimens; 489,579 positives (Influenza A: 434,985; B: 54,594), underscoring recurring vaccination need.

Recent commercial catalysts (2025):

➤Zydus VaxiFlu™ trivalent launch (India) aligned with WHO recommendations.

➤Pfizer PCV20 adult launch (India) expanding pneumococcal protection.

Market Trends

➤Annual influenza backbone: Persistent 60% share supported by quadrivalent coverage, strain refresh, and employer/retail campaigns.

➤RSV breakout: Fastest growth on older-adult and maternal strategies; increased disease awareness post-pandemic.

➤mRNA acceleration: Fastest-growing platform for strain-agile updates, combo candidates (e.g., flu+COVID+RSV), and rapid scale-up.

➤Intranasal momentum: Fastest-growing route for pediatric/needle-phobic groups; mucosal immunity appeal.

➤Sustainability pivot: Shift away from egg-based processes; biodegradable/recyclable packaging and greener supply chains.

➤Retailization of vaccines: Pharmacies/retail centers = fastest-growing end-user, widening access and offloading clinics.

➤AI-assisted R&D: Antigen/adjuvant optimization; epitope prediction; synthetic biology + single-cell integration for precision design.

➤Policy tailwinds: Government-funded campaigns, faster seasonal approvals when manufacturing consistency is maintained.

➤Quality & real-world evidence (RWE): Season-specific effectiveness readouts (e.g., Germany interim VE 31% primary care / 69% secondary) guide updates.

➤Emerging-market scaling: Asia Pacific outpaces on population scale, program funding, and local manufacturing expansions.

10 Deep AI Roles & Impacts

➤Strain Forecasting & Antigen Selection: Models predict dominant strains earlier (e.g., VaxSeer concept), reducing mismatch risk and boosting VE.

➤Epitope & Adjuvant Discovery: Protein-structure + omics models prioritize B/T-cell epitopes and adjuvant pairings to raise immunogenicity.

➤mRNA Sequence Optimization: AI tunes coding regions, UTRs, codons for expression, stability, and manufacturability—shortening design-to-clinic cycles.

➤Formulation Design Space Search: Multivariate AI explores stabilizers/buffers to enhance cold-chain robustness and shelf life.

➤In-silico Toxicology & Safety Flags: Predictive safety screens shrink attrition, refining dose ranges and schedule before FIH trials.

➤Trial Site & Cohort Selection: ML targets hot-spots (season timing, positivity rates) to accelerate enrollment and capture attack rates efficiently.

➤Adaptive Trial Ops: Bayesian/AI engines re-weight arms mid-season, compressing time to interim efficacy decisions.

➤Manufacturing Yield Prediction: Predictive maintenance + process analytics stabilize fill-finish and antigen yields, cutting batch failures.

➤Real-time Pharmacovigilance: NLP on EHR/AE streams detects rare signals sooner; dynamic benefit-risk dashboards for regulators.

➤Programmatic Targeting for Uptake: Propensity models route reminders via pharmacies/retail to boost coverage in high-risk cohorts.

Regional Insights

North America – 40% share (2024)

➤Access & Funding: Strong payer coverage and public stockpiles sustain high uptake; retail chains widen reach.

➤Innovation Hub: Early adoption of mRNA and RSV adult/maternal programs; combo vaccine trials active.

➤Epidemiology signals: High testing volume (4.0M specimens; 490k positives) validates recurring seasonal demand.

United States

➤Campaigns & Logistics: National flu/RSV/COVID pushes; faster approvals for strain updates maintain timely supply.

➤Channel shift: Pharmacy-led vaccinations reduce clinic burden; analytics target seniors and chronic-disease clusters.

Asia Pacific – Fastest growth

➤Scale economics: Large populations in China/India/Japan drive dose volumes; expanding domestic capacity lowers costs.

➤Program expansion: Government-backed immunization and local launches (e.g., VaxiFlu™, PCV20) accelerate adoption.

➤India signal: NCDC reports 2,400 influenza cases / 13 deaths by June 2025, prompting awareness and pediatric focus.

Europe – Robust healthcare, steady growth

➤Coverage & Policy: Insurance and public programs cover geriatric/HCW/chronic cohorts; strong cold-chain and clinic networks.

➤Effectiveness feedback: Germany 2024/25 co-circulation of A & B with 31% VE (primary care) / 69% (secondary) guides season updates.

Latin America & MEA – Emerging access

➤LATAM: Brazil/Mexico scale up public campaigns; local finishing improves availability pre-season.

➤MEA: Saudi/UAE fund adult and Hajj-related respiratory programs; South Africa strengthens lab surveillance for timing.

Market Dynamics

Drivers

➤High disease burden & aging: Recurrent influenza and rising geriatric share expand annual eligible populations.

➤Awareness & public programs: Public health agencies (45% share, 2024) fund high-risk cohorts; campaigns lift coverage.

➤Platform agility: mRNA = fastest-growing enables rapid strain refresh and combo development (flu/RSV/COVID).

Restraints

➤Seasonal mismatch risk: Antigenic drift can undercut VE despite strong coverage (e.g., Germany interim VE split).

➤Cold-chain & last-mile: Intramuscular 70% reliance demands reliable logistics; intranasal options still scaling.

➤Hesitancy pockets: Misinformation depresses uptake; uneven retail legalization limits pharmacy growth in parts of APAC/MEA.

Opportunities

➤RSV runway: Fastest-growing vaccine type (older adults, maternal/pediatric strategies).

➤Retail vaccination scale: Pharmacies/retail = fastest-growing end-user—shorter queues, evening/weekend access.

➤Sustainable manufacturing: Move off egg-based; adopt recyclable packaging; lower footprint attracts tenders.

Challenges

➤Manufacturing switchover cadence: Scaling mRNA while maintaining inactivated (35%) supply parity.

➤Regulatory timing: Tight strain-decision → release windows each year.

➤Equity & affordability: Ensuring Asia Pacific and LATAM/MEA access during peak seasons.

Recent Developments

➤Zydus Lifesciences (Sep 2025): VaxiFlu™ TIV launched in India, aligned to WHO seasonal guidance.

➤Pfizer (Aug 2025): PCV20 launch for adults in India broadens pneumococcal protection.

➤AI milestone (Aug 2025): VaxSeer (MIT CSAIL + Jameel Clinic) showcases AI-driven protective candidate and flu-strain prediction.

Top Leading Companies 2025

1. AstraZeneca plc

Strengths:

Strong R&D pipeline in viral vector and intranasal vaccines (e.g., AZD1222 platform).

Global distribution network across >100 countries.

Strategic collaborations with Oxford University and emerging-market manufacturers.

Weaknesses:

Limited presence in mRNA platforms compared to Pfizer and Moderna.

Past supply and safety perception issues during early COVID-19 vaccine rollouts.

Over-reliance on contract manufacturing partnerships.

Opportunities:

Expansion into RSV and next-gen flu boosters.

Potential to combine adenoviral and protein-based technologies.

Demand in low- and middle-income countries for affordable vaccines.

Threats:

Competition from mRNA-based developers.

Regulatory scrutiny over viral vector technologies.

Supply chain dependencies on third-party manufacturers.

2. CSL Seqirus

Strengths:

One of the world’s largest influenza vaccine producers.

Advanced cell-based and adjuvanted vaccine technologies (e.g., Flucelvax, Fluad).

Strong presence in U.S., Europe, and Asia-Pacific seasonal vaccine markets.

Weaknesses:

Product line mainly focused on influenza, limited diversification.

Dependence on seasonal demand cycles.

High manufacturing cost of cell-based vaccines.

Opportunities:

Growing adoption of cell-based production for improved strain matching.

Expansion into mRNA and combination respiratory vaccines.

Partnerships with AI developers for strain selection optimization.

Threats:

Fierce competition from Sanofi, GSK, and Pfizer.

Price pressures from public health procurement programs.

Supply fluctuations due to egg shortages or pandemic disruption.

3. Novavax Inc.

Strengths:

Proprietary Matrix-M adjuvant technology enhances immunogenicity.

Expertise in recombinant nanoparticle vaccines.

Strong R&D progress in COVID-19 and RSV combination candidates.

Weaknesses:

Limited global manufacturing network compared to larger peers.

Financial instability and high dependency on government funding.

Delayed regulatory approvals for certain markets.

Opportunities:

Potential breakthrough with flu-RSV-COVID combination vaccines.

Strategic licensing or partnerships with large pharma firms.

Expanding footprint in low-income countries through technology transfer.

Threats:

Competition from mRNA players with faster platform adaptability.

Market consolidation reducing standalone opportunities.

Investor skepticism affecting long-term R&D funding.

4. Johnson & Johnson (Janssen Pharmaceuticals)

Strengths:

Established adenovirus vector vaccine platform (Ad26).

Broad global manufacturing footprint and logistics.

Robust financial stability and diversified pharma portfolio.

Weaknesses:

Limited ongoing innovation in influenza and RSV vaccines.

Declining public confidence post-COVID-19 vaccine phase-out.

Smaller vaccine business compared to pharma segment.

Opportunities:

Expansion into combination respiratory vaccines.

Potential application of Ad26 platform for future seasonal variants.

Strategic collaborations with AI partners for vaccine design.

Threats:

Intense competition in respiratory vaccine segment.

Shifting regulatory priorities toward mRNA-based products.

Reduced revenue visibility post-pandemic.

5. Bharat Biotech

Strengths:

Strong presence in emerging markets with cost-effective vaccines.

Proven manufacturing capabilities (e.g., Covaxin, influenza formulations).

Government collaborations for public immunization programs in India.

Weaknesses:

Limited presence in Western markets due to slower regulatory approvals.

R&D resources lower than multinational competitors.

Relatively smaller marketing and distribution network.

Opportunities:

Expansion into global seasonal influenza and pediatric RSV vaccines.

Export potential through WHO prequalification.

Investment in nasal and intradermal vaccine innovations.

Threats:

Competition from Serum Institute of India and multinational players.

Volatile raw material pricing and cold-chain challenges.

Regulatory and compliance hurdles in developed markets.

6. Serum Institute of India Pvt. Ltd.

Strengths:

World’s largest vaccine manufacturer by volume.

High production capacity for influenza, pneumococcal, and COVID-19 vaccines.

Strategic partnerships with AstraZeneca, Novavax, and WHO.

Weaknesses:

Dependence on licensing and technology transfer from global innovators.

Limited original R&D pipeline.

Heavy reliance on low-margin public sector contracts.

Opportunities:

Expansion into mRNA and next-gen RSV vaccines.

Growth in Africa and Southeast Asia through GAVI and UNICEF programs.

Vertical integration in cold-chain logistics and packaging.

Threats:

Increasing competition from Chinese and Korean manufacturers.

Regulatory delays in developed market entries.

Supply chain volatility affecting exports.

7. Sinovac Biotech Ltd.

Strengths:

Proven expertise in inactivated vaccine technology.

Strong domestic market share in China.

Rapid scalability and cost-effective production.

Weaknesses:

Limited innovation in advanced platforms like mRNA or recombinant proteins.

Geopolitical and trade-related barriers in Western markets.

Transparency and data credibility concerns.

Opportunities:

Expansion into developing markets in Asia, Latin America, and Africa.

Development of inactivated RSV and influenza boosters.

Collaboration with biotech firms for new delivery systems.

Threats:

Competition from Sinopharm and international vaccine leaders.

Decreasing demand for inactivated COVID-19 vaccines.

Regulatory scrutiny in foreign markets.

8. Sinopharm Group Co. Ltd.

Strengths:

Backed by Chinese government; robust funding and infrastructure.

Broad vaccine portfolio and advanced R&D network.

High-volume production of COVID-19 and influenza vaccines.

Weaknesses:

Dependence on domestic market for revenue.

Limited adoption in Western countries.

Slower innovation compared to mRNA competitors.

Opportunities:

Expansion through Belt and Road vaccine diplomacy.

Entry into Africa and Latin America via supply partnerships.

Investment in next-gen technologies (mRNA and recombinant platforms).

Threats:

Political tensions restricting global access.

Global competition in low-cost vaccine supply.

Rising domestic competition from emerging Chinese biotech firms.

9. Daiichi Sankyo Company, Limited

Strengths:

Strong research capabilities in adjuvanted and recombinant vaccines.

Strategic presence in Japan and international collaborations.

Long-term investment in mRNA technology platforms.

Weaknesses:

Smaller vaccine division compared to its pharmaceutical arm.

High production cost structure.

Limited exports beyond Asia.

Opportunities:

Development of universal flu and mRNA-based RSV vaccines.

Joint ventures with Western partners to globalize portfolio.

Growth from government immunization funding in Japan.

Threats:

Competitive pressure from GSK, Sanofi, and CSL in Asia-Pacific.

Regulatory hurdles for novel vaccine approvals.

Market saturation in Japan’s domestic vaccine sector.

10. Mitsubishi Tanabe Pharma Corporation

Strengths:

Strong presence in Japanese immunization programs.

Expertise in biotechnology and cell culture-based vaccine production.

Strategic alliances with research universities and biotech startups.

Weaknesses:

Limited global market footprint.

Narrow vaccine product portfolio.

Lower production capacity compared to global peers.

Opportunities:

Expansion into Asia-Pacific with influenza and COVID-19 boosters.

Collaborations in AI-driven vaccine optimization.

Entry into pediatric and geriatric vaccine segments.

Threats:

Domestic competition from Daiichi Sankyo and foreign entrants.

Pricing pressure in Japan’s government-controlled health system.

Rapid innovation in mRNA space threatening traditional platforms.

11. Bavarian Nordic

Strengths:

Specialization in viral vector and recombinant vaccines.

Strong reputation in smallpox and monkeypox immunization.

Expanding portfolio into influenza and RSV using proprietary MVA-BN platform.

Weaknesses:

Relatively small-scale production capacity.

High manufacturing costs for vector-based vaccines.

Limited penetration outside Europe and North America.

Opportunities:

Development of multivalent respiratory vaccines.

EU funding support for pandemic preparedness.

Partnerships for large-scale seasonal vaccine rollout.

Threats:

Strong competition from mRNA and recombinant platforms.

High R&D expenses with uncertain commercial returns.

Complex regulatory landscape for novel viral vector technologies.

12. Valneva SE

Strengths:

Diverse vaccine portfolio including Lyme disease, chikungunya, and flu candidates.

Proven expertise in inactivated and adjuvanted vaccines.

Strong R&D collaborations with Pfizer and CEPI.

Weaknesses:

Limited commercial infrastructure outside Europe.

Financial dependence on licensing and grants.

Smaller pipeline compared to top-tier peers.

Opportunities:

Entry into seasonal influenza and travel-related vaccines.

Potential EU and U.S. approvals for new candidates.

Co-development opportunities with pharma giants.

Threats:

Competitive intensity in emerging vaccine fields.

Regulatory delays impacting revenue timelines.

Manufacturing scale-up risks.

13. BioNTech SE

Strengths:

Pioneer in mRNA technology; co-developed Comirnaty with Pfizer.

Strong AI and bioinformatics capabilities for vaccine optimization.

Expanding pipeline in flu, RSV, malaria, and shingles.

Weaknesses:

Heavy dependence on Pfizer collaboration for manufacturing and distribution.

Limited independent global infrastructure.

High R&D expenditure with short-term profit volatility.

Opportunities:

Development of multi-pathogen mRNA vaccines (flu + RSV + COVID).

Penetration into oncology and infectious disease cross-platform synergies.

Partnerships with developing nations for localized production.

Threats:

Competitive innovation race with Moderna and GSK.

Market saturation in post-pandemic COVID-19 boosters.

Regulatory complexities in multi-pathogen vaccine trials.

14. Vaxine Pty Ltd

Strengths:

Australian biotech specializing in recombinant and adjuvanted vaccines.

Proprietary Advax adjuvant platform enhances immune response.

Recognized for rapid-response vaccine development capacity.

Weaknesses:

Small-scale manufacturer with limited commercialization channels.

Low brand recognition globally.

Funding constraints limiting expansion.

Opportunities:

Licensing of Advax adjuvant to global partners.

Entry into influenza and RSV vaccine collaborations.

Government and CEPI grants for pandemic preparedness.

Threats:

Dependence on grant-based funding.

Competition from large biotech firms with mRNA platforms.

Regulatory and logistical challenges in scaling production.

15. SK Bioscience Co., Ltd.

Strengths:

Strong South Korean manufacturer with advanced cell culture and recombinant platforms.

Partnerships with AstraZeneca, GSK, and Novavax.

Robust government support and domestic vaccination infrastructure.

Weaknesses:

Limited brand visibility outside Asia.

Reliance on contract manufacturing for global partners.

Still expanding independent R&D capabilities.

Opportunities:

Development of self-branded influenza and RSV vaccines.

Expansion into ASEAN and Middle East markets.

Collaboration with AI firms for vaccine design optimization.

Threats:

Pricing competition with Indian and Chinese suppliers.

Volatile global demand post-pandemic.

Dependency on licensing agreements for key revenue streams.

Segments Covered in the Seasonal Vaccines Market (In-depth)

1. By Vaccine Type

Influenza Vaccines (60% share, 2024):

➤Dominant segment driven by annual flu prevention programs and WHO-recommended strain updates.

➤Includes Trivalent (TIV) and Quadrivalent (QIV) formulations for broader strain coverage.

➤Rising production capacity and public awareness boost seasonal uptake.

RSV (Respiratory Syncytial Virus) Vaccines (Fastest-growing):

➤Strong demand among older adults, infants, and maternal health programs.

➤Boosted by newly approved vaccines and ongoing global rollout campaigns.

Pneumococcal Vaccines:

➤Seasonal/annual boosters for adults; protection against pneumonia and invasive disease.

➤Driven by rising geriatric immunization coverage and newer 20-valent (PCV20) formulations.

COVID-19 Booster/Annualized Vaccines:

➤Integrated into seasonal vaccination schedules for high-risk groups.

➤mRNA-based combinations with flu and RSV are under development.

Others (e.g., Meningococcal, Tick-borne Encephalitis):

➤Address niche or regional pathogens with cyclical infection patterns.

2. By Technology Platform

Inactivated/Split Virion Vaccines (35% share, 2024):

➤Most widely used for influenza; safe for geriatric, pediatric, and pregnant populations.

➤Stable storage, long shelf life, and established manufacturing infrastructure.

Live Attenuated Vaccines:

➤Nasal formulations gaining popularity for children and needle-averse adults.

➤Stimulate mucosal immunity and strong antibody response.

Recombinant Protein Vaccines:

➤Egg-free production and improved antigenic match increase acceptance.

➤Lower allergenic risks and faster scalability.

mRNA-based Vaccines (Fastest-growing):

➤Enable rapid strain updates, multi-pathogen combinations, and high efficacy.

➤Central to next-generation influenza, RSV, and COVID-19 programs.

DNA-based Vaccines:

➤Early-stage innovations offering easy manufacturing and thermostability.

Vector-based Vaccines:

➤Use viral vectors for durable immunity; under trial for RSV and COVID boosters.

Others:

➤Include nanoparticle, peptide, and self-amplifying RNA (saRNA) technologies in development.

3. By Route of Administration

Intramuscular (IM) – 70% share, 2024:

➤Gold-standard method offering consistent absorption and strong systemic immunity.

➤Widely used across hospitals, clinics, and retail pharmacies.

Subcutaneous:

➤Used for select live vaccines; preferred in pediatrics due to lower injection pain.

Intranasal (Fastest-growing):

➤Needle-free delivery improving compliance; targets mucosal immunity in respiratory infections.

Oral:

➤Under development for next-gen polio and rotavirus formulations; convenient but stability-sensitive.

Others (e.g., Transdermal Patches):

➤Innovative, self-administered systems improving accessibility and logistics in remote areas.

4. By End User

Public Health Agencies (45% share, 2024):

➤Bulk procurement and subsidized programs for mass immunization campaigns.

➤Focus on high-risk populations, including elderly, infants, and healthcare workers.

Hospitals & Immunization Clinics:

➤Core administration centers for influenza, pneumococcal, and RSV vaccines.

➤Equipped for cold-chain management and large-volume storage.

Pharmacies & Retail Vaccination Centers (Fastest-growing):

➤Expansion driven by convenience, extended hours, and walk-in services.

➤Increasingly integrated into national immunization systems.

Ambulatory Care Centers:

➤Growing role in outpatient vaccination; connected with digital scheduling and reminders.

Others (Corporate/Institutional Programs):

➤Workplace vaccination drives enhancing employee safety and compliance.

5. By Region

North America (40% share, 2024):

➤Mature infrastructure, high awareness, and strong retail distribution network.

➤U.S. leads global vaccine R&D, manufacturing, and adoption.

Europe:

➤Advanced public health programs, strong insurance support, and high vaccination rates.

➤Notable focus on elderly and healthcare worker immunization.

Asia Pacific (Fastest-growing):

➤Expanding population base, government immunization programs, and affordable vaccine launches.

➤India and China lead regional volume growth.

Latin America:

➤Emerging adoption, supported by WHO and PAHO immunization initiatives.

➤Brazil and Mexico focus on universal flu and COVID-19 boosters.

Middle East & Africa (MEA):

➤Strengthening through adult immunization campaigns and regional disease surveillance.

➤Increasing investments in cold-chain infrastructure and vaccine manufacturing.

Top 5 Searched FAQs

1) What is driving the Seasonal Vaccines Market growth (2025–2034)?

●Rising influenza and RSV incidence.

●Expansion of public vaccination programs.

●Growing use of mRNA technology for faster updates.

●Increased retail and pharmacy vaccination access.

●Aging population and broader immunization coverage.

2) Which segments led the market in 2024?

●Region: North America – 40% share.

●Vaccine Type: Influenza – 60% share.

●Platform: Inactivated/Split Virion – 35% share.

●Route: Intramuscular – 70% share.

●End User: Public Health Agencies – 45% share.

3) Which segments are growing fastest?

●Vaccine Type: RSV vaccines.

●Platform: mRNA-based vaccines.

●Route: Intranasal delivery.

●End User: Pharmacies & Retail Centers.

●Region: Asia Pacific.

4) How is AI transforming the Seasonal Vaccines Market?

●Predicts dominant flu strains.

●Optimizes antigen and adjuvant design.

●Enhances mRNA sequence and formulation.

●Improves trial design and manufacturing efficiency.

●Enables real-time safety monitoring and coverage targeting.

5) What are the key recent developments in 2025?

●Zydus Lifesciences: Launched VaxiFlu™ trivalent flu vaccine in India.

●Pfizer: Released PCV20 for adult pneumococcal protection.

●MIT & Jameel Clinic: Introduced AI tool VaxSeer for flu strain prediction.

Access our exclusive, data-rich dashboard dedicated to the pharmaceuticals sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6347

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest