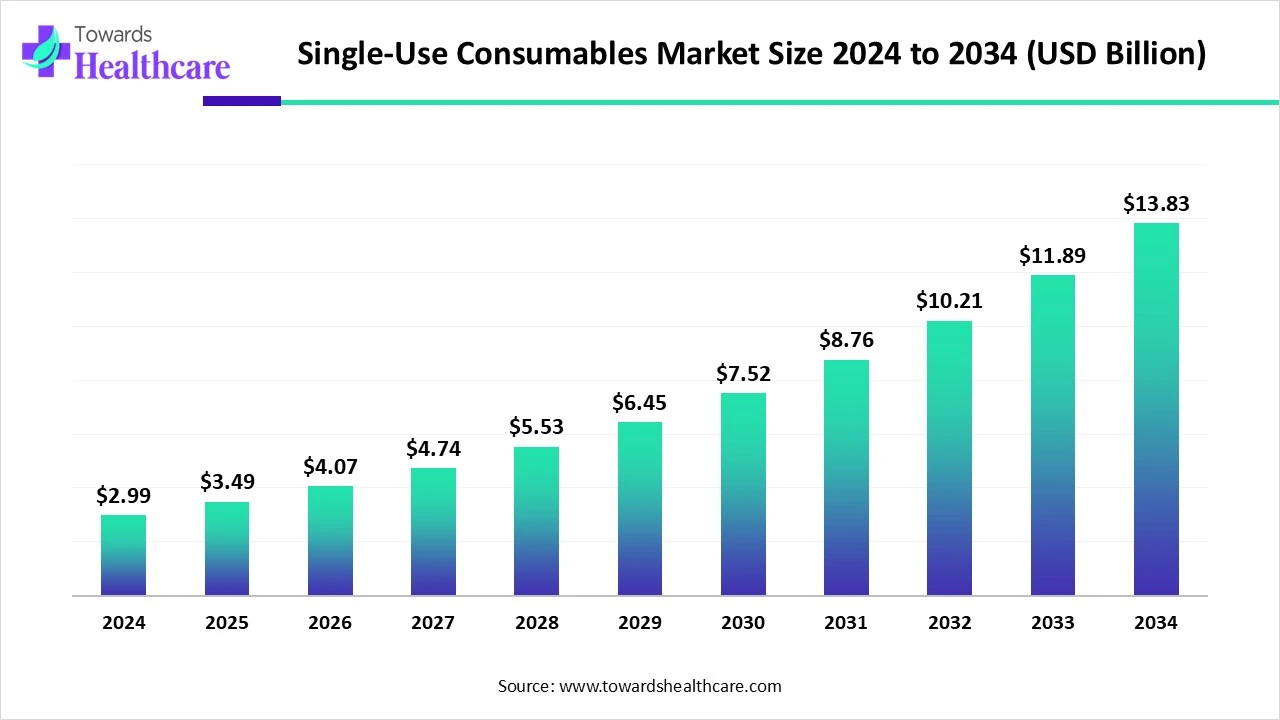

The global single-use consumables market, valued at USD 2.99 billion in 2024, is projected to grow to USD 13.83 billion by 2034 at a robust CAGR of 16.56%, driven by infection control needs, biopharma expansion, and demand for sterile, disposable medical products.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6070

Market Size

◉2024 → USD 2.99 billion (baseline year).

◉2025 → USD 3.49 billion, early acceleration.

◉2030 (Mid-Term Projection) → ~USD 8.09 billion (strong growth as biopharma capacity expands).

◉2034 (Forecast Horizon) → USD 13.83 billion, over 4.6x expansion from 2024.

◉CAGR → 16.56% (2025–2034), one of the fastest growth rates in the medtech consumables sector.

Revenue Contribution by Region (2024):

◉North America → 36–40%

◉Europe → ~25–28%

◉Asia-Pacific → ~22–25% (fastest-growing)

◉Latin America & MEA → ~10–15% combined.

High-Growth Product Segments (2034 projection):

◉Catheters & vascular access → fastest CAGR.

◉Infection control & PPE → largest share in 2024, steady growth.

Material Share (2024):

◉Plastics & polymers → 55% (dominant).

◉Advanced dressings → fastest CAGR.

Market trends

Infection prevention institutionalized

◉PPE & infection-control products held 30% share in 2024—now embedded into routine clinical ops beyond pandemic spikes, reinforced by strict regulatory standards and HAI mitigation mandates.

Biologics & vaccines reshape throughput

◉The biopharma build-out (vaccines, mAbs, cell & gene therapies) favors single-use sterility and fast changeovers (e.g., tubing sets, bags, filters, preassembled kits), lifting recurring consumable demand.

Material innovation—pragmatic sustainability

◉Plastics & polymers remain dominant (55% in 2024) for sterility, cost, and manufacturability.

◉Biodegradable/compostable and low-allergen innovations (e.g., accelerator-free nitrile) gain traction as waste and skin-safety pressures rise.

Provider purchasing is unbundling

◉Direct & GPO contracts (55%) still anchor volume in 2024, but online/B2B marketplaces are the fastest-growing, enabling price transparency, long-tail SKUs, and JIT replenishment.

Pricing models modernize

◉Per-unit purchasing dominates today; subscription & managed inventory models accelerate to reduce stockouts, smooth cashflow, and tie replenishment to actual procedure volumes.

Network scale matters

◉Regional DC expansion (e.g., Cardinal Health’s 2024 Ohio distribution center intent) underscores the premium on fill-rate reliability, last-mile speed, and GxP-compliant traceability.

North America leads; APAC scales fastest

◉NA’s 36–40% share stems from advanced infrastructure and regulatory rigor; APAC outpaces on growth via capex in biomanufacturing and an expanding CMO/CDMO base.

AI impact/role

Demand & procedure forecasting

◉ML models forecast SKU-level demand (gloves, masks, syringes, catheters) from surgical schedules, census data, seasonality, and outbreak signals—reducing stockouts and costly overstock.

Smart inventory & PAR optimization

◉AI tunes PAR levels by unit/ward, maps ABC/XYZ item criticality, and triggers auto-replenishment; aligns consignment and trunk-stock to real utilization.

Computer vision quality control

◉Real-time vision models flag micro-defects (microtears, lumen occlusion, tip deformities, contamination) in catheters, IV sets, and gloves, tightening AQL and sterility assurance.

Lot genealogy & traceability

◉AI reconciles batch/lot/device identifiers across ERP + WMS + MES, improving recall readiness, expiry control, and UDI compliance.

Supply-chain risk sensing

◉Models detect upstream resin/film/tubing risks, DC bottlenecks, and carrier disruptions; autonomously re-routes POs, shifts demand to approved alternates, and rebalances safety stock.

Dynamic pricing & contracting

◉AI simulates per-unit vs. subscription cost curves by historical burn rates; proposes tiered bundles (e.g., procedure kits) to lower total cost per case while meeting compliance.

Sustainability analytics

◉Lifecycle and waste analytics pinpoint swap-in SKUs (e.g., biodegradable drapes in non-critical settings), quantify waste-disposal savings, and model CO₂e reductions.

Regulatory document automation

◉NLP agents classify sterility/biocompatibility dossiers, map them to FDA/EMA/ISO sections, and flag gaps for faster audit readiness.

E-commerce personalization

◉Recommenders build facility-specific catalogs, auto-substitute equivalent SKUs during backorders, and pre-build procedure packs tuned to case-mix.

Workforce enablement

◉Copilots surface IFUs, donning/doffing checklists, and lot/expiry alerts at POC (point of care), improving compliance and reducing errors.

Regional insights

North America (Leading, 36–40% in 2024)

Why it leads

◉Advanced hospital networks, high surgical volumes, mature GPO ecosystems, and strict infection-control enforcement.

Market energy

◉Strong CMO/CDMO presence and biologics pipelines → high pull for sterile, single-use components.

Distribution muscle

◉Ongoing DC expansions to tighten lead times and inventory reliability; direct & GPO contracts dominate today.

Europe

Compliance-driven steadiness

◉Stringent HAI standards and procurement oversight sustain demand for PPE, sterile drapes, vascular access, and safety syringes.

Material shift

◉Elevated interest in sustainable textiles and polymers in non-critical settings; plastic-reduction initiatives shape SKU choices.

Asia-Pacific (Fastest growth)

Industrial build-out

◉Accelerating biopharma manufacturing (China, India, South Korea, Japan) drives sterile single-use adoption across upstream/downstream steps.

Domestic champions

◉Growth of local manufacturing (e.g., gloves, dressings, tubing) shortens supply lines and lowers landed cost.

Care delivery

◉Rapid expansion of ASCs/outpatient care boosts demand for procedure-specific kits and non-sterile patient-care consumables.

Latin America & Middle East/Africa

LatAm

◉Brazil/Mexico lead on hospital capacity growth; uptake paced by budget cycles and import dynamics.

MEA

◉KSA/UAE invest in advanced care (oncology, CV), lifting sterile consumable usage; South Africa anchors regional adoption.

Market dynamics

Drivers

◉CMO/CDMO expansion → multiproduct, small-batch agility needs sterile, fast-changeover single-use (no cleaning validation burden).

◉Example: Akums Drugs & Pharmaceuticals (2025): new sterile lyophilized/injectables facility in India → high reliance on single-use to ensure sterility and adaptability.

◉Vaccine & biologics pipelines → mRNA, viral-vector, protein vaccines scale faster with single-use assemblies.

◉Example: Pfizer (2025) mRNA expansion (influenza, RSV), leveraging single-use intensive bioprocessing.

◉Infection control engrained in policy & practice → PPE, sterile drapes, safety syringes remain structural demand.

Restraints

◉Environmental impact & disposal costs → regulatory and financial pressure to curb plastic waste; push for greener materials.

◉Medical waste management capacity → incineration and segregation constraints elevate total cost of ownership for disposables.

Opportunities

◉Sustainable polymers & advanced dressings → growth runway for biodegradable/compostable options and bioactive/antimicrobial dressings.

◉Digitized procurement → fastest growth via online/B2B marketplaces and integrated inventory services.

◉Commercial innovation → managed inventory / subscription bundles reduce stockouts and smooth budgeting; high appeal to ASCs/OPDs.

Top companies

3M

◉Products: Infection-control/PPE (masks, respirators), surgical drapes & barrier materials.

◉Overview: Global materials & medical solutions leader.

◉Strengths: Filtration/barrier science, large-scale manufacturing, brand trust in infection control.

Medline Industries

◉Products: Broad single-use portfolio—PPE, drapes, trays, patient-care disposables.

◉Overview: Vertically integrated manufacturer/distributor to providers.

◉Strengths: Depth of catalog, private-label scale, logistics reach in U.S. hospitals.

Cardinal Health

◉Products: PPE, surgical consumables; large medical distribution.

◉Overview: Major U.S. med-surg distributor with owned brands.

◉Strengths: GPO relationships, DC network efficiency; 2024 plan for Walton Hills, OH distribution expansion underscores fulfillment muscle.

Becton, Dickinson & Co. (BD)

◉Products: Syringes, needles, safety devices; vascular access.

◉Overview: Leader in medication delivery & safety.

◉Strengths: Safety IP, manufacturing scale, clinical workflow integration.

Baxter International

◉Products: IV sets, infusion consumables, sterile solutions.

◉Overview: Hospital therapy & infusion specialist.

◉Strengths: Installed base in acute care, therapy-set standardization.

B. Braun Melsungen

◉Products: Catheters, infusion, vascular access systems.

◉Overview: Procedural & infusion therapy focus.

◉Strengths: Vascular expertise, clinician trust, EU footprint.

Kimberly-Clark Health / Kimtech

◉Products: Gloves, masks, gowns, lab apparel.

◉Overview: PPE & hygiene specialist.

◉Strengths: Non-woven know-how, comfort/fit innovation, sustainability initiatives.

Ansell

◉Products: Medical & surgical gloves.

◉Overview: Hand-protection leader.

◉Strengths: Material science, allergy-reduction focus, breadth of glove portfolio.

Terumo Corporation

◉Products: IV/infusion sets, catheters, access devices.

◉Overview: Vascular & interventional specialist.

◉Strengths: Precision manufacturing, cardiovascular credibility.

Smiths Medical

◉Products: Catheters, infusion disposables, airway management items.

◉Overview: Acute care & critical-care disposables.

◉Strengths: Clinical breadth, integration with monitoring/therapy workflows.

ConvaTec / Coloplast / Mölnlycke Health Care

◉Products: Advanced wound dressings, ostomy & continence care; surgical drapes/gowns.

◉Strengths: Wound-healing science, skin integrity, OR barrier systems.

Owens & Minor / Henry Schein

◉Products: Wide med-surg disposables; dental/clinic channels (H. Schein).

◉Strengths: Distribution depth, practice-level relationships.

Fresenius Kabi / Teleflex / Cook Medical / Nipro Medical

◉Products: IV therapy sets, vascular access, specialty catheters and kits.

◉Strengths: Therapy specialization, kit customization, global reach.

Investment & Funding Insights In Single-Use Consumables Market

Market funding thesis — why investors care

◉Large, recurring demand: Consumables are repeat-purchase products with predictable recurring revenue (P/RR), driven by routine procedures, PPE use, and steady hospital throughput.

◉High gross margins on specialty items: Advanced dressings, procedure kits, and specialty catheters often command higher margins than commodity plastics.

◉Resilience to economic cycles: Clinical necessity (infection control, surgeries, chronic-care consumables) makes cashflows relatively inelastic.

◉Scalability via CMOs/CDMOs & contract manufacturing: Manufacturers can scale capacity quickly via contract partners, reducing time-to-market.

◉Regulatory and quality moat: Proven sterility, biocompatibility testing and approvals (GMP, ISO, CE, FDA) create barriers to entry.

◉Innovation pathways: Sustainable polymers, accelerator-free gloves, single-use endoscopes, and systemized procedure kits create product differentiation and premium positioning.

◉Tech-enabled operational uplift: AI for demand forecasting, QA, and inventory management reduces working capital and shrinkage — attractive to investors seeking operational leverage.

Who invests and typical instruments

Strategic corporate investors (corporates & PE-backed strategics)

◉Motive: market share, proprietary SKUs, supply-chain control, fill capacity (e.g., 3M, Cardinal Health initiatives).

◉Instrument: M&A, bolt-on acquisitions, JV, equity stakes.

Private Equity (buyout / growth)

◉Motive: consolidate fragmented regional manufacturers/distributors, optimize operations, roll-up strategies, scale distribution (GPO access).

◉Instrument: Majority buyouts, growth equity, earn-outs.

Venture Capital / Growth Equity

◉Motive: early-stage material innovation (biodegradable polymers), advanced dressings, single-use endoscope startups, AI-enabled supply platforms.

◉Instrument: Series A–C equity, convertible notes, SAFE (early-stage).

Debt / Project Finance

◉Motive: capex for high-speed manufacturing lines, plant expansions (e.g., mask lines).

◉Instrument: Term loans, vendor financing, asset-backed loans, export credit for cross-border capex.

Public markets / PIPEs

◉Motive: Established manufacturers may access public equity for large capex or M&A. PIPEs used for growth-stage raises.

Government grants & concessional finance

◉Motive: local manufacturing incentives (vaccine/biopharma capacity building), supply-chain resilience funds.

◉Instrument: Grants, subsidized loans, capex rebates (relevant in NA/APAC policy pushes).

Typical capital requirements / use of proceeds (by stage)

Early-stage (R&D / material tech / prototypes)

◉Use: lab R&D, polymer formulation, biocompatibility testing, first ISO/FDA compliance tests.

◉Typical raise: seed to Series A (small relative to manufacturing).

Scale-up (commercialization / market entry)

◉Use: pilot production, clinical evaluations, sales & limited distribution, regulatory submissions.

◉Typical raise: Series A–B or growth equity.

Manufacturing & distribution expansion (capex heavy)

◉Use: high-speed lines, cleanrooms, packaging automation, DCs. Example: USMGC mask lines; Akums sterile facility.

◉Typical raise: large growth equity ± debt, project finance.

Consolidation / M&A

◉Use: roll-up, integrating distribution networks, systems harmonization. Typically PE-led.

Valuation drivers & value levers investors watch

◉Recurring revenue share & renewal rates (per-unit purchases vs subscriptions) — subscription/managed inventory increases enterprise value multiples.

◉Gross margin by SKU — advanced dressings, specialty catheters > commodity gloves.

◉Customer concentration (GPO & direct contracts) — long-term GPO deals reduce revenue risk and support higher valuation.

◉Regulatory clearances & quality systems — FDA/CE/ISO create defensibility.

◉Manufacturing footprint & capacity utilization — higher utilization materially boosts cashflow.

◉Proprietary IP / differentiated materials — patents on polymers/coatings or exclusive supplier contracts.

◉Geographic revenue diversification — NA + APAC presence reduces single-market risk.

◉Supply-chain resilience — dual sourcing, local DCs, vertical integration (reduces input risk).

◉Data & tech stack — AI-enabled forecasting, lot traceability and e-commerce storefronts improve margins and reduce WC.

Key financial metrics and KPIs investors track

◉Annual Recurring Revenue (ARR) for subscription models.

◉Revenue retention: gross & net (cohort analysis for hospital/ASC customers).

◉SKU churn & SKU rationalization benefit (concentration of top 20 SKUs).

◉Gross margin % by product family (PPE vs advanced dressings vs catheters).

◉Contribution margin per procedure/kit.

◉Working capital days (inventory days, payables days).

◉Capacity utilization (% of installed lines in operation).

Order fill rate & on-time delivery %.

◉Cost per sterile unit (manufacturing overhead allocation).

◉R&D / regulatory spend as % revenue (for innovators).

◉Customer concentration (top 5 customers % of revenue).

◉EBITDA margin and free cash flow (for PE/strategic buyers).

Risk factors investors must quantify

◉Regulatory risk: delayed approvals or product non-compliance (FDA/EMA/PMDA) → revenue impact.

◉Environmental/regulatory pushback: plastic bans or costly disposal rules may compress margins or require capital to switch materials.

◉Commodity input volatility: resin/resin derivatives price swings materially affect low-margin plastics SKUs.

◉Customer concentration & GPO dependence — contract loss is high-impact.

◉Supplier single-sourcing & geo-political risk (e.g., import dependence).

◉Capex intensiveness: overbuilding capacity before demand can drive underutilization.

◉Reprocessing/reusable competitor cost-parity: if reuse models or sterilization tech materially reduce TCO for hospitals, unit demand may decline.

◉Reputational/product safety: contamination or failure incidents can lead to recalls and large liabilities.

◉Region-specific funding considerations & signals

North America

◉Strong private capital availability (PE/strategic). Expect larger multipliers for companies with GPO contracts and robust QA. Government incentives for reshoring (supply-chain resilience) can co-finance capex.

Asia-Pacific

◉Growth capital focused on local manufacturing scale-up and export capacity. National biotech & vaccine funding accelerates demand for single-use upstream consumables (bags, tubing sets). Investors should expect faster volume ramp potential but also price competition.

Europe

◉Funding appetite for sustainability-focused innovations is high (grants & green loans). Compliance with EU environmental directives influences capex for greener lines.

LatAm / MEA

◉Risk-adjusted returns higher; investors prefer distributors or asset-light plays rather than heavy manufacturing until demand and reimbursement structures stabilize.

Latest announcement

May 2025 — U.S. Medical Glove Company (USMGC)

◉What: Full-scale opening of a U.S. face-mask manufacturing facility with six high-speed lines for 3-ply disposable masks.

Why it matters:

◉Strengthens domestic PPE self-reliance, diversifying away from import shocks.

◉Adds redundant capacity for surge scenarios; shortens replenishment lead times.

◉Enhances supply-chain resiliency for U.S. healthcare networks and GPOs.

Recent developments

April 2025 — INTCO Medical

◉Launch: Syntex Synthetic Disposable Latex Gloves (patented).

◉Compliance: Passed EN455 / EN374; aligned to FDA and EU CE requirements.

Implications:

◉Raises quality/safety bar for latex alternatives; pushes performance parity with natural latex.

◉Broad cross-industry relevance (healthcare, food processing, industrial)—expands addressable demand.

May 2025 — Wadi Surgicals (India)

◉Launch: Enliva accelerator-free nitrile gloves (India’s first).

◉Clinical value: Minimizes accelerator-induced dermatitis/allergies; improves clinician comfort for prolonged use.

◉Strategic angle: Positions India as a specialty glove innovation hub; supports Asia’s fastest growth profile.

Segments covered

A) By Product Category

Infection Control & PPE (Gloves, Masks, Gowns)

◉Largest 2024 share (30%). Essential for HAI reduction and perioperative safety.

IV & Infusion Consumables (sets, tubing, connectors, filters)

◉Core for medication delivery; high volume, standardized SKUs.

Syringes, Needles & Safety Devices

◉Safety-engineered designs reduce sharps injuries; crucial for vaccines/biologics.

Catheters & Vascular Access (Peripheral & Central)

◉Fastest-growing product set; incidence of chronic disease and ICU use drives demand.

Surgical Disposables & Drapes

◉Maintains sterile field; customization via procedure packs.

Diagnostic & Sample Collection Kits

◉Swabs, tubes, POC consumables; standard in labs and outreach testing.

Wound Care Single-Use Dressings & NPWT Interfaces

◉Advanced dressings improve moisture management and healing trajectories.

Single-Use Endoscopes & Accessories

◉Reduces cross-contamination concerns; procedure-specific economics.

Urinary & Ostomy Consumables

◉Chronic care consumables with stable recurring use.

Other (feeding sets, nebulizer kits, sterilization pouches, trays)

◉Long-tail, essential support SKUs across wards.

B) By Material / Technology

Single-Use Plastics & Polymers (55% in 2024)

◉Dominant for cost/sterility/formability; compatible with multiple sterilization modes.

Non-woven Textiles

◉Foundation for gowns/drapes; comfort and barrier balance.

Advanced Dressings (hydrogel, alginate, foams)

◉Fastest-growing for wound complexity and aging populations.

Prefilled Glass/Plastic Syringes & Molded Components

◉Dose accuracy and aseptic handling benefits.

Biodegradable/Compostable Polymers

◉Emerging—addresses disposal cost and environmental pressure.

C) By Sterility / Use Case

Sterile Surgical & Procedural Consumables (45% in 2024)

◉OR/ICU critical supplies; stringent barrier and packaging needs.

Non-Sterile Patient Care Consumables (fastest-growing)

◉High-throughput, convenience-led, expanding in home care and general wards.

Single-Use Preloaded/Prefilled Systems

◉Reduces prep time, error risk; improves workflow standardization.

D) By End User / Care Setting

Hospitals & Acute Care (60% in 2024)

◉Largest concentration of procedures and critical care.

Ambulatory Surgery Centers & Outpatient Clinics (fastest-growing)

◉Minimally invasive & same-day care expand SKU turnover.

Long-Term Care & Nursing Homes / Home Healthcare / Diagnostic Labs & Reference Centers

◉Stable demand for non-sterile patient-care items and collection kits.

E) By Distribution Channel

Direct Sales & GPO Contracts (55% in 2024)

◉Pricing leverage, compliance, fill-rate SLAs.

Medical Distributors & Wholesalers

◉Breadth and regional reach.

Online / E-commerce & B2B Marketplaces (fastest-growing)

◉JIT ordering, SKU discoverability, analytics.

Retail Pharmacies

◉Outpatient & home-care consumables access point.

F) By Commercial Model / Pricing

Per-Unit Purchase / Consumable Sales (dominant)

◉Budget transparency; pay-as-used.

Managed Inventory / Subscription Bundles (fastest-growing)

◉Automated replenishment; lower stockouts and carrying cost.

Private-Label & Contract Manufacturing

◉Cost control and formulary standardization for large networks.

G) By Region

◉North America (leading share), Europe (steady), Asia-Pacific (fastest growth), Latin America & MEA (developing but rising)

◉Align product/price/channel to each region’s regulatory rigor, care-setting mix, and local manufacturing maturity.

Top-5 FAQs

1 What’s the market size now and by 2034?

US$ 2.99B (2024) → US$ 3.49B (2025) → US$ 13.83B (2034), CAGR 16.56% (2025–2034).

2 Which region leads and which grows fastest?

North America leads with 36–40% (2024); Asia-Pacific is fastest-growing.

3 Which product categories are largest vs. fastest?

Largest (2024): Infection-control & PPE (30%)

Fastest: Catheters & vascular access.

4 Which channels and models dominate?

Direct & GPO (55%) dominate; online/B2B grows fastest. Per-unit purchase dominates; managed inventory/subscriptions grow fastest.

5 What are the main headwinds?

Environmental impact & high disposal costs (waste handling/regulatory pressure), balanced by innovation in sustainable materials and AI-enabled efficiency.

Access our exclusive, data-rich dashboard dedicated to the Life Science Sector built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/6070

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest