The Ventricular Assist Device (VAD) market is quietly reshaping the future of cardiac care. As heart failure cases continue to rise globally, demand for advanced mechanical circulatory support is growing faster than ever.

From hospitals to specialized cardiac centers, clinicians are increasingly relying on VADs to extend life and improve quality of care in critical patients. This shift is not just clinical; it is strongly reflected in market numbers.

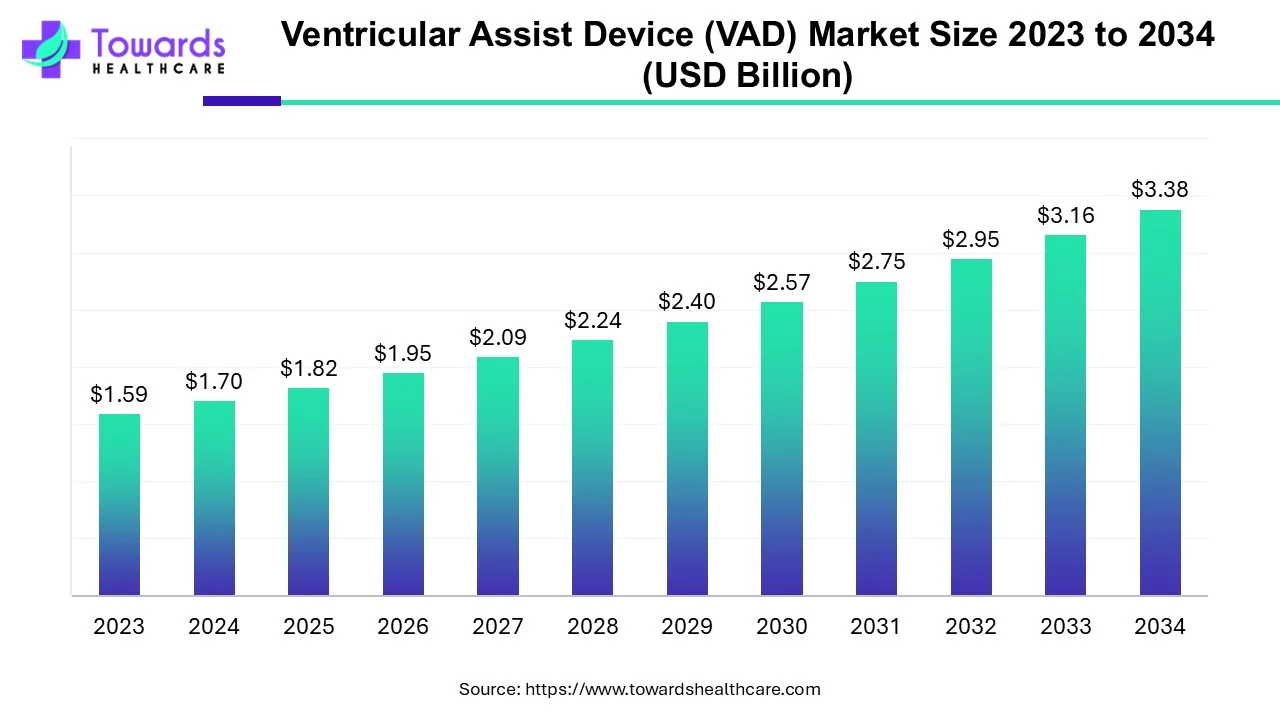

The Ventricular Assist Device (VAD) market size is projected to grow from USD 1.82 billion in 2025 to USD 3.38 billion by 2034, at a compound annual growth rate (CAGR) of 7.1%.

Confused by too much market data? Our experts simplify it with a free customized vad market sample (segments,regions,stats,company data,compititors and more): https://www.towardshealthcare.com/download-sample/5151

This steady growth highlights both rising disease burden and increasing trust in device-based cardiac support systems.

A Market Driven by Urgency, Not Choice

Heart failure is no longer a rare condition. It is becoming a widespread health challenge, especially among aging populations and patients with lifestyle-related diseases.

As transplant availability remains limited, VADs are stepping in as a critical alternative, either as a bridge to transplant or as long-term therapy.

What makes this market unique is its necessity-driven demand. Patients often do not have multiple treatment options, making VAD adoption less about preference and more about survival.

Segment Spotlight: Left Ventricular Assist Devices Lead the Race

When we break down the market by product type, one segment clearly dominates—Left Ventricular Assist Devices (LVADs).

LVADs account for approximately 75% of the total market share, making them the backbone of the VAD industry.

This dominance comes from the fact that left ventricular failure is the most common type of heart failure. As a result, LVADs are used more frequently than right or biventricular devices.

Other segments include:

- Right Ventricular Assist Devices (RVADs), contributing around 15% share

- Biventricular Assist Devices (BiVADs), holding roughly 10% share

Despite smaller shares, these segments are essential in complex cardiac cases where multiple chambers are affected.

Stop switching between reports — manage your entire VAD Market data in one smart hub. Access the dashboard: https://www.towardshealthcare.com/access-dashboard

By Design: Implantable Devices Take Control

Another critical segmentation lies in device design—implantable versus external VADs.

Implantable VADs dominate the market with over 80% share, driven by better patient mobility, longer usage duration, and improved survival outcomes.

External VADs, though limited in share, still play a role in temporary support scenarios and emergency settings.

Key factors driving implantable device growth include:

- Advancements in miniaturization and battery life

- Reduced risk of infection and complications

- Increasing patient preference for long-term solutions

Therapy Type Segmentation: Destination Therapy Gains Momentum

VADs are used across different therapy types, but the landscape is shifting rapidly.

Traditionally, “bridge to transplant” held the largest share. However, “destination therapy” is now emerging as a strong contender, accounting for nearly 43% of the market.

This shift is happening because many patients are not eligible for heart transplants. For them, VADs are no longer temporary—they are the final treatment solution.

Other therapy segments include:

- Bridge to transplant: around 38% share

- Bridge to recovery: approximately 12% share

This evolving segmentation reflects a deeper change in how clinicians approach long-term cardiac care.

End-User Insights: Hospitals Dominate Usage

Hospitals remain the primary end-users of VADs, holding more than 70% market share.

This is largely due to the complexity of implantation procedures and the need for specialized post-operative care.

Cardiac centers and specialty clinics are also growing in importance, especially in urban regions with advanced healthcare infrastructure.

The demand is particularly strong in developed markets, but emerging economies are catching up quickly due to improving healthcare access.

Regional Trends Add Another Layer to Segmentation

Geographically, North America leads the VAD market with over 41% share, driven by high healthcare spending and early adoption of advanced technologies.

Europe follows with around 25%–30% share, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR higher than the global average.

India and China are key contributors to this growth, supported by rising awareness and increasing cardiac disease prevalence.

What Shapes the Future of VAD Segments?

The segmentation of the VAD market is not static—it is evolving with technology, patient needs, and healthcare systems.

Artificial intelligence integration, remote monitoring, and improved device durability are expected to reshape segment shares in the coming years.

At the same time, cost and accessibility will play a major role in determining how quickly emerging markets adopt these devices.

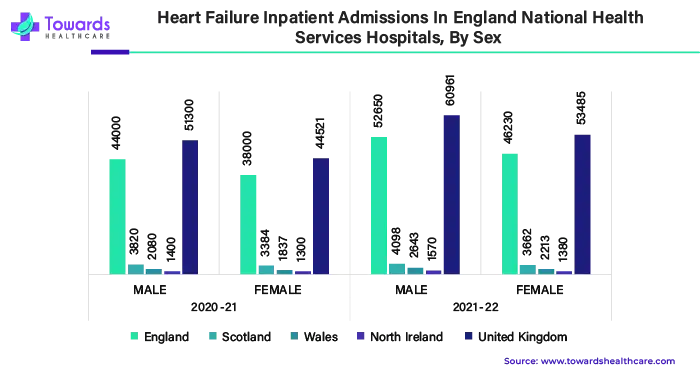

Rising Heart Failure Prevalence Fosters VAD Market Growth

Heart failure admissions in NHS hospitals show a clear gender gap, with males consistently recording higher numbers than females across both years.

This indicates a higher clinical burden or earlier onset of cardiovascular complications among men.

Let’s talk for Free; our experts will guide you through the market in full detail, from competitors to opportunities: https://www.towardshealthcare.com/schedule-meeting

In 2020–21, England reported around 44,400 male admissions compared to nearly 36,000 for females.

The difference highlights a significant disparity, suggesting targeted prevention strategies may be needed for male populations.

By 2021–22, admissions increased noticeably, with male cases in England rising to approximately 52,600.

Female admissions also grew to about 46,200, reflecting an overall upward trend in heart failure cases.

Across smaller regions like Scotland and Wales, admission numbers remained relatively low compared to England.

However, the upward trend is still visible, indicating that the issue is widespread, not region-specific.

Northern Ireland and the UK totals follow a similar pattern, with males consistently leading in admission counts.

This consistency across regions strengthens the observation of gender-based differences in heart health outcomes.

Overall, the data suggests a rising burden of heart failure admissions from 2020–21 to 2021–22.

It also reinforces the need for early diagnosis, lifestyle interventions, and gender-focused healthcare strategies.

Contact us for more info:

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium