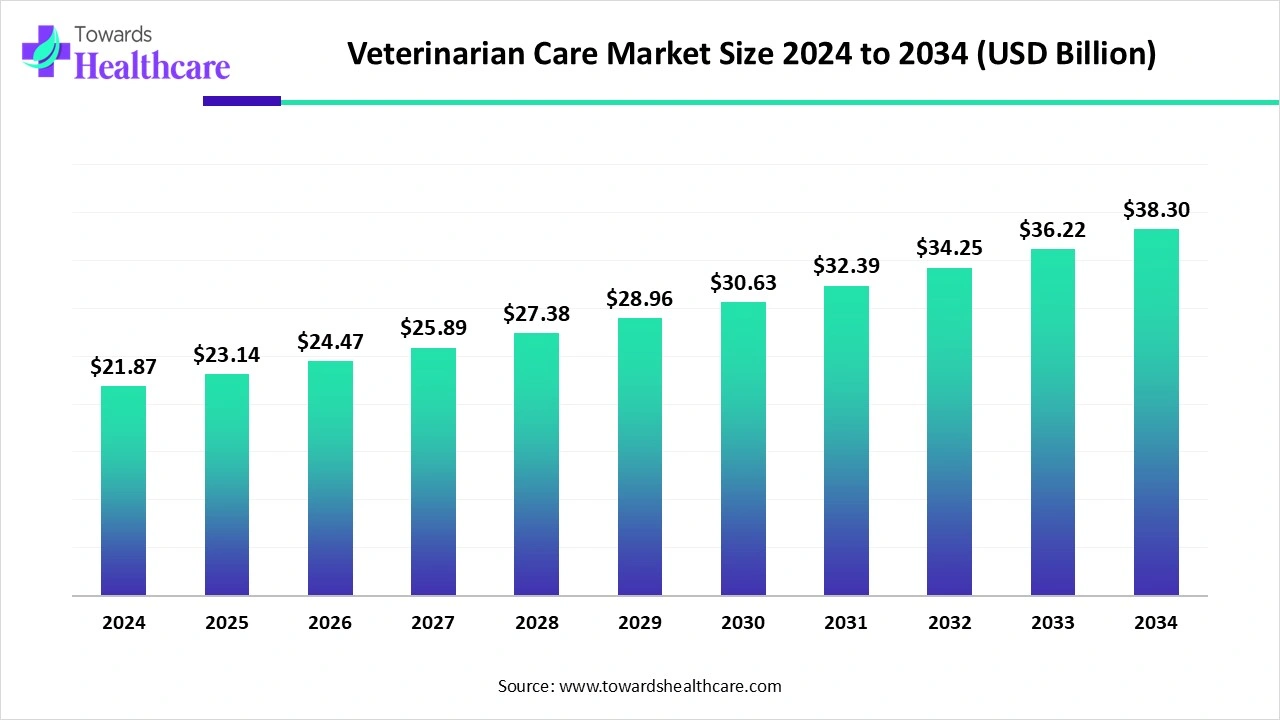

Veterinarian Care Market 2024–2034: US$21.87Bn → US$38.3Bn (5.75% CAGR)

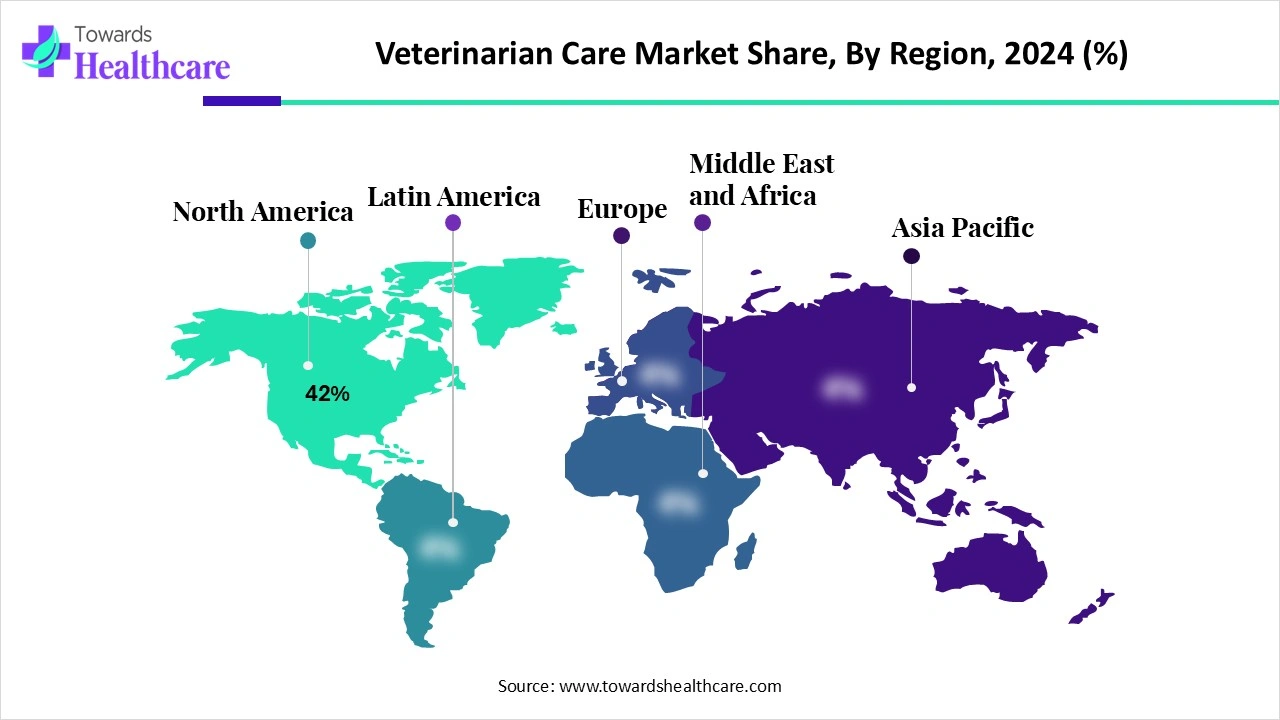

The global veterinarian care market was US$21.87 billion in 2024, is set to reach US$23.14 billion in 2025, and is forecast to hit US$38.3 billion by 2034 at a 5.75% CAGR (2025–2034), led by North America (42% share, 2024), with APAC growing fastest; preventive & wellness (36% share), companion animals (61% share), private clinics (48% share) and in-clinic care are today’s revenue anchors, while specialty services, equine, mobile and home/on-site care scale quickest.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6158

Table of Contents

ToggleMarket size

Baseline & horizon

●2024: US$21.87Bn

●2025: US$23.14Bn

●2034: US$38.3Bn

●Absolute value creation (2024→2034): US$16.4Bn

●Annual trajectory (from 2025 base @ 5.75% CAGR)

●2026: US$24.47Bn

●2027: US$25.88Bn

●2028: US$27.37Bn

●2029: US$28.94Bn

●2030: US$30.60Bn

●2031: US$32.36Bn

●2032: US$34.22Bn

●2033: US$36.19Bn

●2034: US$38.30Bn

Current revenue anchors (2024 mix indicators)

●Preventive & wellness: 36%

●Companion animals: 61%

●Private veterinary clinics: 48%

●Mode: In-clinic care largest

Market trends

Telemedicine normalization

●24/7 virtual access and remote triage expanding reach and lowering stress.

●Evidence: Greencross (Sep 2025) deployed Heidi Health (AI documentation); Vetster (Oct 2024) partnered with Mella to deliver 24/7 care via app across the U.K., Canada, U.S.

AI-assisted clinical productivity

●Ambient scribing, decision support, scheduling optimization embedded into clinic workflows (e.g., Heidi Health use case above).

Regenerative & advanced therapies

●Wider adoption of PRP / stem-cell for ortho and soft-tissue cases.

●Evidence: Endurance Technologies (Aug 2025) launched Endoret PRGF PRP system for clinics, specialty centers, rehab.

Network expansion & consolidation

●New multi-specialty hospitals and urgent care nodes increase availability and case acuity handling.

●Evidence: Chewy Vet Care opened in Austin (Mar 2025); OSU announced US$250M 255k-sq-ft vet teaching hospital (May 2025); Mumbai 100-bed municipal hospital plan (Aug 2025); North Carolina US$2.5M community clinic (2025).

Humanization of pets drives premiumization

●Preventive plans, wellness subscriptions, nutrition counseling, diagnostics bundles.

Insurance uptake

●Higher coverage → greater acceptance of diagnostics/specialty procedures; supports revenue stability in North America.

Mobile & home/on-site care surge

●Doorstep vaccinations, monitoring, minor procedures; fastest growth on convenience and low-stress handling.

Specialty services outpacing general practice

●Oncology, cardiology, orthopedics, critical care rising with improved imaging and surgical capabilities.

Operational resilience focus

●Practices adopt inventory analytics, staffing tools, and standardized SOPs to mitigate regulatory/economic pressures.

Ecosystem partnerships

●Platforms and GPOs enabling independents with tech, training, pricing power (e.g., VerticalVet–Zomedica, Aug 2025).

10 ways AI impacts this market

Diagnostic decision support

●Pattern recognition on imaging/labs + longitudinal EMR context to flag early disease; reduces misdiagnosis and repeat visits.

Triage & load balancing

●AI chat/voice agents route cases to tele-consult, urgent, or specialty; cuts wait times and improves case mix.

Ambient clinical documentation

●Real-time scribe auto-generates SOAP notes, codes, discharge summaries; frees 15–30% clinician time for care.

Predictive care plans

●Risk scores from breed/age/lab history → proactive screenings, vaccine schedules, diet plans; boosts wellness plan adherence.

Imaging automation

●Auto-measurements (e.g., cardiac indices), lesion detection on radiographs/ultrasound; standardizes quality across sites.

Inventory & procurement optimization

●Demand forecasting for meds/consumables reduces stockouts, shrink, and working capital.

Revenue cycle intelligence

●Eligibility checks, code suggestions, denial prediction; higher clean-claim rates and faster cash conversion.

Staffing & rota optimization

●Schedule models align surgeon/ER availability with forecasted case loads; lowers overtime and burnout.

Client engagement & retention

●Personalized reminders, AI chat follow-ups, adherence nudges; lifts revisit rates and preventive compliance.

Quality & outcomes benchmarking

●Cross-clinic analytics (complication rates, LOS, readmits) surface best practices; feeds continuous improvement.

Regional insights

North America (2024 share 42%)

Demand drivers: High companion animal ownership, strong pet insurance penetration, willingness to pay for premium care.

Infrastructure: Dense networks of clinics/hospitals and specialty ERs; integrated diagnostics and tele-vet platforms.

Ecosystem moves: New nodes like Chewy Vet Care (Mar 2025); academic expansion (OSU US$250M hospital).

Outlook: Mature but still expanding via specialty, urgent care, and AI-enabled efficiency.

Asia Pacific (fastest growth)

Macro: Rising disposable income, urban pet adoption, growing welfare awareness.

Access expansion: New hospitals in metros (e.g., Mumbai 100-bed plan), mobile/tele-vet to penetrate peri-urban/rural.

Capability lift: Investment in vet education, gradual insurance introduction; strong runway in diagnostics and specialty.

Europe

Market shape: Consolidated chains alongside strong independent clinics; high standards of welfare and regulation.

Focus: Specialty referrals, preventive programs, and cross-border diagnostic platforms; AniCura and others scale ER/specialty.

Latin America

Trajectory: Growing companion animal spend; opportunity in wellness plans, vaccinations, and diagnostics access.

Middle East & Africa

Build-out: Emerging specialty and referral facilities in GCC; mobile/tele-vet to extend reach; import-heavy diagnostics.

Market Dynamics

DRIVERS

1) Pet ownership & humanization → durable preventive revenue

Commercial effect: With preventive & wellness at 36% of 2024 revenue, clinics lock in predictable, high-margin, subscription-like flows (vaccines, parasite control, checkups).

Unit economics: Preventive plans lower cost per visit (standardized protocols) and lift lifetime value via earlier diagnostics referrals (lab + imaging uplift).

Pricing power: Humanization supports premium offerings (nutrition consults, dental, dermatology), improving mix even when visit volumes plateau.

Execution plays:

●Bundle wellness + diagnostics (annual CBC/Chem/UA + dental screening).

●Loyalty & reminders to lift adherence (vaccination windows, parasite seasonality).

●Breed/age risk stratification to personalize plans.

2) Capacity build-out & network effects (OSU US$250M, NC US$2.5M, Mumbai 100-bed, Chewy Vet Care Austin)

Supply expansion: New nodes add clinical throughput and case acuity capacity (ER, surgery, specialty) → higher average revenue per case (ARPC).

Referral flywheel: Teaching/research hospitals (OSU) and large municipal/retail-linked sites (Mumbai, Chewy) become regional gravity wells, increasing downstream imaging, surgery, and rehab volumes.

Talent magnet: Flagship facilities attract specialists (oncology, cardio, ortho), enabling service-line growth (your data: specialty services fastest-growing).

Execution plays:

Design spoke-to-hub pathways (GP → ER/Specialty) with shared EMR and SOPs.

Co-locate diagnostics to compress “order-to-result” times and lift conversion.

3) Technology adoption at the point of care (tele-vet, AI documentation at Greencross)

Throughput & access: Tele-triage + virtual follow-ups decongest clinics, preserve in-clinic slots for procedures (your data: in-clinic is largest mode).

Admin relief: AI scribing (e.g., Heidi Health) shrinks documentation time, enabling more consults per clinician/day without eroding quality.

Care continuity: Tele-vet + remote monitoring (e.g., app-based vitals) reduce lapses between visits, reinforcing preventive plan adherence.

Execution plays:

Route routine follow-ups/behavior/nutrition to tele-tracks.

Standardize AI-assisted SOAP templates; audit for compliance and coding accuracy.

RESTRAINTS

1) Regulatory complexity & welfare compliance → higher non-clinical load

Cost centers: Licensing, facility standards, controlled drug handling, data privacy, and welfare audits increase overhead per site.

Operational drag: Variability across jurisdictions complicates multi-region SOPs; slows rollouts of mobile/home services (fastest-growing mode).

Mitigations:

Central compliance PMO; unified policy library and training cadence.

Pre-deployment checklists for mobile/home units (cold-chain, biohazard, consent).

EMR audit trails + AI prompts to enforce documentation completeness.

2) Economic cyclicality → deferral of discretionary procedures

Demand sensitivity: Elective and non-urgent specialty work (dentals, ortho fixes, oncology workups) is timing-sensitive; consumers may delay in downturns.

Cash flow: Slower approvals on larger estimates without insurance; pressure on AR and cancellations.

Mitigations:

Tiered care plans (good/better/best) + transparent estimates.

Financing/BNPL options and insurance education at point-of-care.

Protect the core: emphasize preventive (36%) to stabilize utilization.

OPPORTUNITIES

1) Untapped markets via mobile and tele-vet (fastest-growing end-user & mode)

White space unlock: Rural/peri-urban areas and dense urban micro-neighborhoods lack convenient access; mobile clinics bridge last-mile logistics.

Cost advantage: Lower fixed costs per additional catchment vs. full brick-and-mortar; route-optimized schedules maximize clinician utilization.

Execution plays:

Hub-and-route design: mobile for vaccines/parasite control + sample collection; complex cases funneled to hubs.

Bundle home/on-site wellness with tele-follow-ups to maintain continuity and upsell diagnostics.

2) Mix upgrade via specialty services (fastest-growing service) & equine (fastest animal growth)

Revenue density: Advanced procedures (oncology, cardio, ortho, dentistry, rehab) drive higher ARPC and stickier referral relationships.

Equine tailwind: Rising investment in breeding/racing/recreation boosts imaging, surgery, and rehab adoption; portability of PRP/stem-cell protocols supports field care.

Execution plays:

Build referral compacts with GP clinics; guaranteed turnaround and consult notes within 24–48h.

Equip equine field teams with portable imaging and regenerative kits (PRP) to capture high-value cases.

3) Platform & partnership leverage (e.g., VerticalVet–Zomedica)

Scale benefits for independents: Access to diagnostics platforms, training, negotiated pricing, and shared analytics raises clinical and financial performance.

Standardization: Shared SOPs and tech stacks enable network-level quality dashboards (outcomes, recheck rates, complications).

Execution plays:

Join/forge alliances for pricing power on consumables/diagnostics.

Benchmark KPIs across peers to drive continuous improvement.

WHAT THIS MEANS FOR OPERATORS

Protect the core 36%: Expand wellness-plan tiers; include annual labs + dental screening to push earlier detection and specialty referrals.

Exploit modality arbitrage: Shift routine consults to tele-vet/home to free in-clinic capacity for higher-margin procedures.

Invest where growth is fastest: Stand up specialty lines and equine field capabilities; align marketing with referral partners.

Standardize with AI: Roll out ambient scribing + coding prompts; measure note time, claim acceptance, and recheck compliance.

De-risk compliance: Centralize regulatory tracking; use EMR hard stops for consent, controlled-substance logs, and welfare checks.

KPIs & LEADING INDICATORS

Growth drivers

Wellness plan penetration (% of active clients; target steady YoY lift).

Tele-to-in-clinic conversion (triage accuracy → procedure bookings).

Specialty case mix (% of total revenue; rising share confirms mix upgrade).

Restraints control

Admin minutes per consult (post-AI target: sustained reduction).

Compliance audit pass rate (first-time pass %) and incident rate.

Cancellation/deferral rate on estimates > set thresholds during soft demand.

Opportunity capture

Mobile route yield (revenue/route/day; revisit rates).

Equine ARPC and field procedure uptake (PRP, imaging, rehab).

Referral turnaround (time to consult, report quality scores).

RISK SCENARIOS & RESPONSES

Downturn shock: Spike in deferrals → activate “value tier” care bundles, financing offers, and focus marketing on preventive ROI.

Regulatory tightening: New welfare or mobile-care rules → preempt with policy blueprints and modular compliance kits for vans/home visits.

Talent scarcity in specialty: Competes up wages → grow internal fellowships, tele-specialist overlays, and case-review programs to scale expertise.

Top 10 companies

Banfield Pet Hospital (Mars, Inc.)

Product/Focus: Preventive plans, primary care at scale across hundreds of clinics.

Overview: Largest companion-animal GP network.

Strengths: National footprint, standardized protocols, data scale.

VCA Animal Hospitals (Mars, Inc.)

Product/Focus: GP + specialty + emergency, reference labs access.

Overview: Broad U.S./Canada presence.

Strengths: Referral pathways, integrated diagnostics, training.

BluePearl Specialty & Emergency (Mars, Inc.)

Product/Focus: 24/7 ER, oncology, cardiology, surgery.

Overview: Specialty/ER leader.

Strengths: Complex case management, advanced imaging.

National Veterinary Associates (NVA)

Product/Focus: Community of independent-style hospitals.

Overview: Large multi-brand operator.

Strengths: Local practice autonomy with central ops support.

Greencross Vets

Product/Focus: Clinics across Australia; wellness and integrated retail.

Overview: Leading APAC network.

Strengths: Tech adoption (e.g., Heidi Health), preventive programs.

IDEXX Laboratories (diagnostics-focused)

Product/Focus: In-clinic analyzers, reference labs, imaging software.

Overview: Diagnostics backbone for clinics.

Strengths: Installed base, innovation cadence, data services.

CVS Group plc

Product/Focus: U.K./EU practices, referrals, labs.

Overview: Consolidated European operator.

Strengths: Integrated services, specialist centers.

MedVet Associates

Product/Focus: Specialty and ER hospitals.

Overview: U.S. referral network.

Strengths: High-acuity care, clinician depth.

Thrive Pet Healthcare (Pathway Vet Alliance)

Product/Focus: GP + specialty, membership wellness, urgent care.

Overview: U.S. multi-format provider.

Strengths: Value access models, unified CRM/EMR.

AniCura (Mars, Inc., Europe)

Product/Focus: Specialty, referral, and advanced diagnostics.

Overview: Pan-European network.

Strengths: Consistent quality standards, ER/specialty scale.

Latest announcements

VerticalVet × Zomedica (Aug 2025): Partnership to equip independent practices with advanced platforms to improve clinical outcomes and operational efficiency.

FoW Partners / Elevated Veterinary Solutions (Sep 2025): Workforce-centric, tech-powered clinic growth platform to expand access to care.

Recent developments

Elanco (Feb 2025): Launched Pet Protect—vet-designed supplements for dogs and cats to tap fast-growing pet nutraceuticals.

Greencross (Sep 2025): Expanded Heidi Health AI documentation across its network to speed consults and reduce admin.

Vetster × Mella (Oct 2024): 24/7 tele-vet via Mella app in U.K., Canada, U.S.

Endurance Technologies (Aug 2025): Endoret PRGF—advanced PRP system for clinics, specialty centers, rehab.

Chewy Vet Care (Mar 2025): New Austin clinic combining wellness, urgent care, and surgery.

Capacity build-outs (2025): OSU US$250M new vet hospital; North Carolina US$2.5M community clinic; Mumbai 100-bed municipal hospital plan.

Segments covered

By Service Type

Preventive & Wellness (36% share, 2024): Vaccinations, checkups, parasite control; recurring revenue foundation.

Diagnostics & Imaging: Lab testing; X-ray, ultrasound, MRI/CT; enables early detection and specialty referrals.

Surgery & Emergency: Acute/critical interventions; high value per case.

Specialty Services (fastest growth): Orthopedics, oncology, cardiology, dermatology, dentistry, rehab/PT—driven by tech and owner willingness to pay.

By Animal Type

Companion animals (61% share, 2024): Dogs, cats, others; highest visit frequency and spend per pet.

Livestock: Cattle, swine, poultry, small ruminants; herd health and productivity services.

Equine (fastest growth): Sports/recreation care; imaging, surgery, rehab adoption rising.

By End User

Private veterinary clinics (48% share, 2024): Accessible, relationship-centric GP care.

Veterinary hospitals: Multi-specialty and ER capabilities; referral hubs.

Mobile veterinary services (fastest growth): Doorstep convenience; vaccinations, wellness, minor procedures.

Academic & research institutions / Others: Teaching hospitals, shelters, NGOs, military services.

By Mode of Service

In-clinic care (largest): Full equipment, controlled environment for diagnostics/surgeries.

Home/on-site (fastest growth): Convenience, low-stress handling, enabled by portable diagnostics.

Tele-veterinary: Triage, follow-ups, chronic management; 24/7 access.

By Region

North America (42% share, 2024), Europe, Asia Pacific (fastest), Latin America, Middle East & Africa—see regional insights above for growth drivers.

Top 5 FAQs

-

What is the market size now and in the future?

US$21.87Bn (2024) → US$23.14Bn (2025) → US$38.3Bn (2034) at 5.75% CAGR (2025–2034). -

Which region leads today?

North America with 42% share (2024); APAC grows fastest. -

Which segments lead and which grow fastest?

Lead: Preventive & wellness (36%), companion animals (61%), private clinics (48%), in-clinic care.

Fastest: Specialty services, equine, mobile services, home/on-site care. -

What’s driving growth?

Rising pet ownership/humanization, clinic network expansion (OSU US$250M, Chewy Vet Care, Mumbai 100-bed), tele-vet normalization, AI-enabled productivity. -

How is AI changing vet care?

From diagnostic support and ambient scribing to predictive care plans, triage, inventory/RCM, and quality benchmarking—improving access, accuracy, and margins.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6158

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest