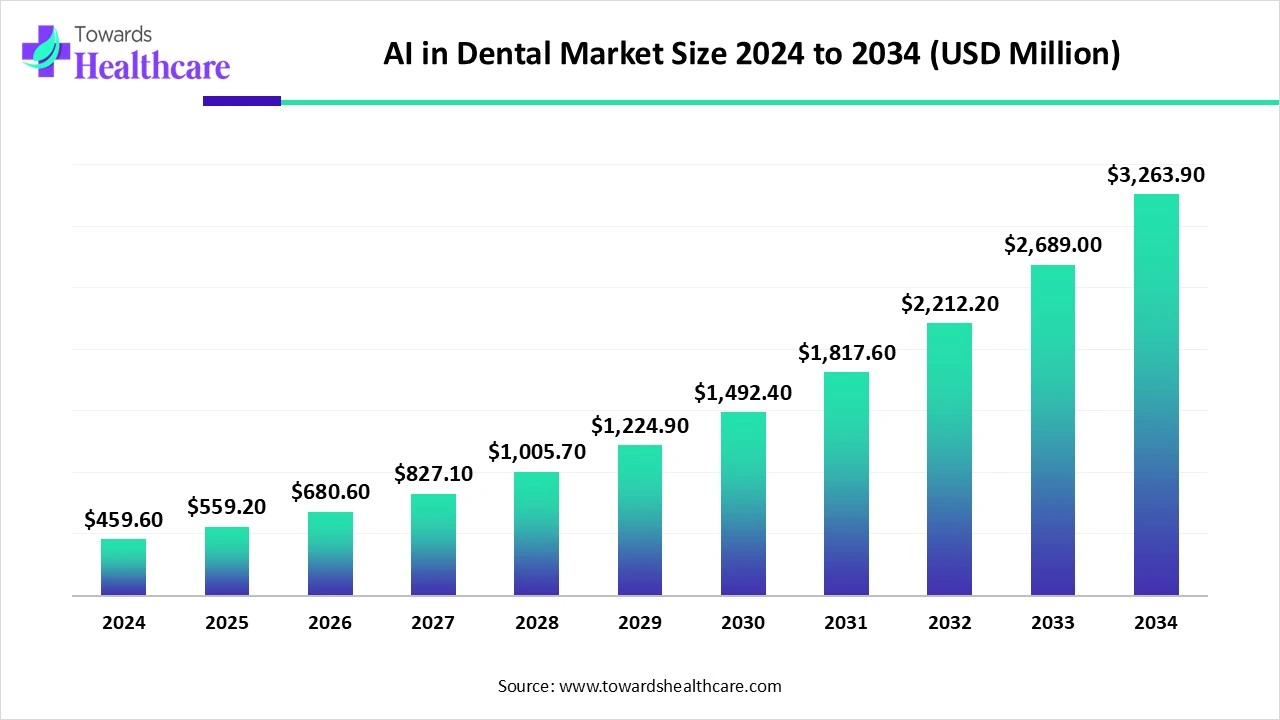

The global AI in dental market is US$ 459.6 Mn (2024), US$ 559.2 Mn (2025), and is set to hit US$ 3,263.9 Mn by 2034—a 7.1× scale-up, compounding at 21.78% (2025–2034).

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6142

Market Size

Current & Near-term Levels

●2024: US$ 459.6 Mn (base year).

●2025: US$ 559.2 Mn; +US$ 99.6 Mn vs. 2024 (21.7% YoY).

Long-term Trajectory

●2034: US$ 3,263.9 Mn; +US$ 2,804.3 Mn absolute increase vs. 2024.

Growth multiple: 7.1× (2034 vs. 2024).

●Incremental opportunity (2025→2034): US$ 2,704.7 Mn.

●Milestones (implied by CAGR 21.78%)

●Crosses US$ 1 Bn: 2028.

●Acceleration drivers: digitization of imaging, cloud deployments, DSO standardization, payer/claims AI.

Price/Value Mix

●Rapid software subscription adoption (cloud) outpacing one-time licenses (on-prem), lifting recurring revenue share.

Customer Mix Trend

●DSOs/Group practices expand faster than solo clinics, concentrating demand for enterprise-grade AI.

Market Trends

●Diagnostic precision mainstreams: AI boosts detection of caries, perio issues, and pathologies from 2D/3D images, improving case acceptance and outcomes.

●Cloud-first orchestration: Cloud dominates deployments in 2024 and remains fastest-growing, enabling real-time analysis, centralized data, and scalable multi-site rollouts.

●Revenue cycle automation: AI enters claims/RCM, cutting denials and documentation gaps (e.g., ClaimsAI launches) and unlocking lost revenue.

●Training & adoption flywheel: Credentialed AI training for dental professionals (e.g., VA series) accelerates responsible adoption.

●Chairside decision support: Real-time CADe on radiographs and integrated treatment insights increase productivity and reduce variability.

●Virtual consults & patient engagement: AI enhances remote triage, case presentation, and follow-ups; boosts conversion and retention.

●Predictive analytics: Risk scoring for caries/perio and recall optimization reduces emergency visits and improves scheduling yield.

●Workflow automation: From documentation to insurance narratives, AI trims admin time, letting clinicians focus on care.

●Interoperability with practice platforms: Smart dental platforms bundle imaging AI + PMS/CRM to unify operations.

●Orthodontics & prosthodontics acceleration: AI-guided simulation/design shortens treatment cycles and improves fit/esthetics—fastest-growing solution cluster through 2034.

10 Deep AI Roles/Impacts in Dental

●Early lesion detection: Finds incipient caries/periodontal changes missed by the naked eye; elevates preventive care.

●Consistency & quality control: Reduces diagnostic variability across providers/locations, aiding DSOs in standardizing care.

●Treatment planning optimization: AI simulates tooth movement/prosthetic fit, minimizing refinements and remakes.

●Chairside time compression: Instant reads on radiographs and auto-charting reduce appointment lengths.

●Case acceptance uplift: Visual AI annotations improve patient understanding, boosting acceptance of recommended care.

●Insurance readiness: Auto-generated narratives and annotated evidence cut denials and resubmissions.

●Throughput & revenue lift: More accurate scheduling, fewer no-shows, and better hygiene recall via predictive analytics.

●Training & upskilling: Structured AI curricula (ADA-accredited examples) help clinicians adopt new workflows safely.

●Data-driven DSOs: Centralized cloud data enables benchmarking across hundreds of operatories; informs procurement and training.

●Tele-dentistry & access: Remote triage + AI review expand access in underserved areas, especially across APAC and rural North America.

Regional Insights

North America (dominant, 2024)

Drivers

●High digital dentistry adoption; chronic tooth decay prevalence in children/adults.

●Mature DSO landscape seeking standardized AI across multi-site networks.

●Robust health IT investment and payer pressures driving RCM AI.

Illustrative move

Guardian Dentistry Partners selecting cloud PMS and Pearl’s AI to modernize 160+ practices.

Asia Pacific (fastest growth, 2025–2034)

Why fastest

●Rising dental caries/periodontal disease, large aging base; expanding healthcare spend.

●Government support for digital health; clinics leapfrog to cloud.

Country notes

●China: Policy push for quality dental care; caries/periodontal disease remain major burdens.

●India: Low awareness/infrastructure gaps create demand for AI triage and efficient care pathways.

Europe (notably growing)

Context

●High tooth loss prevalence; strong insurance/Govt programs improve affordability of AI-enhanced care.

●Country note

●Germany: Strong prevention outcomes in youth; high prosthetic costs make AI-optimized planning attractive.

U.S. & Canada snapshots

●U.S.: Workforce shortages in dental health areas → tele-dentistry + AI scale access; education platforms expand.

●Canada: Rising dental care utilization with higher incomes/education; emphasis on affordable access supports AI adoption.

Latin America & MEA (emerging)

Focus

●Private chains/urban centers pilot AI first; cloud reduces capex barriers; gradual regulatory clarity to follow.

Market Dynamics

Drivers

●Rising prevalence of caries, perio disease, tooth loss, and oral cancers; earlier detection benefits are significant.

●Cloud scalability enables real-time analysis and multi-location standardization; DSOs drive procurement.

●Evidence-based dentistry & patient experience expectations push adoption of CADe and simulation tools.

Restraints

●Upfront costs and budget constraints for small clinics; change management and training needs.

●Data governance and integration complexity with legacy PMS and imaging stacks.

Opportunities

●Robotic/AI-assisted workflows (prep/design/education) show major time gains.

●RCM/claims AI can recapture sizeable lost revenue in U.S. dentistry.

●Education & accreditation programs lower adoption friction, expanding the addressable base.

Top 10 Leading Innovators

Align Technology, Inc.

Products: Invisalign® clear aligners, iTero® scanners, exocad CAD/CAM; Align X-ray Insights (CADe).

Overview: Digital orthodontics leader expanding into restorative decision support.

Strengths: Massive case dataset, robust hardware–software ecosystem, global brand.

Dentsply Sirona Inc.

Products: Imaging (orthopanoramic/CBCT), SureSmile®, CAD/CAM (CEREC), software suites.

Overview: End-to-end digital dentistry portfolio across clinics and labs.

Strengths: Installed base, integrated workflows, training footprint.

Envista Holdings Corporation

Products: DEXIS imaging & software, Nobel Biocare, Ormco orthodontics.

Overview: Multi-brand platform spanning implants, ortho, imaging.

Strengths: Cross-sell breadth, DSO relationships, upgrade path to AI tools.

Carestream Dental LLC

Products: CS Imaging, intraoral/extraoral/CBCT systems; software integrations.

Overview: Imaging specialist modernizing with AI-ready pipelines.

Strengths: Imaging heritage, broad modality coverage, channel reach.

Planmeca Oy

Products: ProMax®/Viso® imaging, Romexis® software platform, chairside units.

Overview: Premium integrated hardware + software vendor.

Strengths: Seamless ecosystem, clinic ergonomics, R&D cadence.

Henry Schein One

Products: Dentrix®, Denticon (cloud PMS), practice analytics, patient comms.

Overview: Practice management leader embedding AI into ops and engagement.

Strengths: Massive PMS footprint, partner marketplace, DSO contracts.

3Shape A/S

Products: TRIOS® intraoral scanners, Dental System™, ortho/prostho design tools.

Overview: Digital impressions & design pioneer integrating AI features.

Strengths: Scan accuracy, software usability, lab–clinic connectivity.

Overjet Inc.

Products: FDA-cleared radiograph AI, practice & DSO analytics, claims support.

Overview: Clinical + business intelligence on top of imaging AI.

Strengths: Regulatory wins, real-time chairside overlays, DSO scaleouts.

Pearl AI

Products: Second Opinion® (radiograph AI), Practice Intelligence.

Overview: Global dental AI provider, strong cloud integrations.

Strengths: Generalizable models, PMS partnerships, international clearances.

VideaHealth

Products: FDA-cleared caries/perio detection; ClaimsAI (RCM).

Overview: Clinical AI expanding into revenue cycle automation.

Strengths: DSO penetration, enterprise analytics, payer/claims ROI.

Latest Announcements

Align Technology (Mar 2025): Launched Align X-ray Insights (AI CADe) across EU/UK to auto-analyze 2D radiographs, extending beyond orthodontics into restorative insights.

VideaHealth (Jul 2025): Unveiled ClaimsAI, targeting ~US$ 15 Bn in annual U.S. dental revenue leakage via AI-driven documentation/denial reduction.

VA + Partners (Jun 2025): Rolled out an ADA-accredited AI training series for dental professionals—on-demand and free, accelerating clinician readiness.

Guardian Dentistry Partners (Mar 2025): Adopted Denticon (cloud PMS) + Pearl AI across 160+ practices to modernize workflows.

Recent Developments

CareStack × Overjet (Mar 2025): Introduced Smart Dental Platform—unifying patient care, operations, and growth with embedded AI.

Archy (Jun 2025): Launched Archy Intelligence—AI agents tackling top practice pain points (scheduling, comms, ops).

RevenueWell × Mila Health (May 2025): Brought human-like AI assistants to automate up to 90% of patient care management tasks.

RipeGlobal (Jul 2025): Entered U.S. market with cloud-based, hands-on education; 10,000+ professionals, spanning 35 countries.

Laxmi Dental (Aug 2025): Investment in IDBG AI Dent Global to advance AI imaging/diagnostics in India.

ANTECH (May 2025): RapidRead Dental AI for veterinary radiographs (10-minute reads; tooth-by-tooth analysis) showcases cross-domain momentum into human workflows.

Segments Covered

By Solution Type

AI-Powered Imaging & Radiology (dominant in 2024)

Core value: Real-time CADe on 2D/3D (bitewings, periapicals, pano, CBCT) to flag caries, perio bone loss, apical lesions, margin defects.

Primary buyers: DSOs, imaging-heavy clinics, academic centers; secondary—solo practices upgrading sensors/CBCT.

Workflow fit: Auto-ingests DICOMs, overlays findings in the viewer, exports annotated images into clinical notes and insurance narratives.

KPI impact: +5–15% case acceptance, −2–5 min per exam, fewer missed pathologies; improved audit/QA.

Integration stack: PACS/VNA, PMS, claims; SSO, role-based access; cloud analytics across locations.

Pricing norms: Per-op or per-site SaaS; volume tiers for DSOs; occasional imaging-bundle discounts.

Adoption frictions: Radiology liability concerns, model generalizability across sensors/CBCT brands, data privacy reviews.

2034 outlook: Stays the largest revenue pool as AI becomes standard on every radiograph; expansion into 3D segmentation and longitudinal change-tracking.

AI Diagnosis & Treatment Planning

Scope: Multi-modal risk scoring, decision support, and evidence-linked recommendations across caries, perio, endo, surgery.

Who buys: Clinicians focused on comprehensive care plans; DSOs seeking standardized protocols.

Workflow: Pulls chart + images, proposes plan options, estimates time/visits, generates consent and financing alternatives.

KPI impact: Fewer treatment revisions, better chair utilization, higher patient acceptance due to visual explanations.

Risks/controls: Guardrails to maintain clinician authority; transparent rationale and editable outputs.

2034 outlook: Deep links to lab and insurance pre-auth; widespread in mid/large practices.

AI Workflow & Practice Management

Scope: Scheduling automation, no-show prediction, clinical note drafting, eligibility checks, claim scrubbing, analytics.

Economic lever: Converts administrative time into clinical chairtime; mitigates revenue leakage.

Typical wins: −10–30% no-shows in at-risk cohorts; faster claim throughput; standardized SOAP notes.

Data needs: PMS + comms + limited imaging context; benefits from cloud to benchmark across sites.

2034 outlook: Bundled within cloud PMS; “autopilot” back office for DSOs and growing groups.

AI for Orthodontics & Prosthodontics Design (fastest-growing)

What it does: Tooth movement simulation, aligner staging, attachment/force optimization; crown/bridge/implant-prosthesis design with margin detection and occlusal tuning.

Clinical payoffs: Fewer refinements/remakes, shorter chairtime, better fit/esthetics; faster lab cycles.

Dependencies: High-quality scans (IOS/CBCT), calibrated photos, lab/print workflows.

Risk guards: Rule-based constraints to avoid biologically unsafe movements or occlusal interferences.

2034 outlook: AI-first design becomes default; human QA remains, but design cycles compress dramatically.

Predictive Analytics & Risk

Focus: Caries/perio risk, recall timing, peri-implantitis watchlists, patient churn risk, demand forecasting by provider/location.

Value: Right-sized hygiene intervals, smarter outreach, and accurate supply/staffing plans.

Data stack: PMS + imaging metadata + comms history; longitudinal models benefit from cloud.

2034 outlook: Moves from dashboarding to closed-loop automation (auto-recall scheduling, inventory triggers).

By Deployment Mode

Cloud-Based Solutions (dominant & fastest)

Why it wins: Elastic scaling for multi-site DSOs, instant model updates, centralized analytics, easier security posture (managed SOC2/ISO).

Ops advantages: Lower IT overhead, rapid rollout to new operatories, safe model versioning, disaster recovery.

Security/compliance: Encrypted at rest/in transit, fine-grained RBAC, detailed audit logs; regional data residency options.

2034 outlook: Default choice for new deployments; near-real-time benchmarking across hundreds of locations becomes standard.

On-Premise Solutions (steady niche growth)

Who prefers: Clinics with strict data-locality rules, patchy internet, or capex budgeting; imaging rooms needing offline continuity.

Strengths: Deterministic performance on local GPUs/CPUs; operation during outages.

Trade-offs: Slower model updates, heavier IT management, less cross-site analytics.

2034 outlook: Remains important for specific compliance/continuity needs, often in hybrid setups.

By Dental Specialty

Orthodontics (dominant, 2024)

Why: Clear aligner planning, tooth-movement prediction, progress assessment, appointment interval optimization.

Gains: Fewer refinements; clearer patient communication via visual simulations; tighter inventory of attachments/auxiliaries.

Prosthodontics (fastest-growing)

AI roles: Margin detection, emergence profile/occlusion optimization, implant-prosthesis design, esthetic harmonization.

Payoff: Lower remake rates, better first-time fit, reduced chairside adjustments.

Endodontics

Use cases: Periapical radiolucency detection, canal morphology hints on CBCT, case triage.

Outcome: Better case selection, more predictable outcomes, fewer undetected lesions.

Periodontics

Use cases: Automated bone-level measurements, longitudinal change tracking, peri-implantitis surveillance.

Outcome: Objective staging over time; targeted maintenance scheduling.

Oral Surgery

Use cases: 3D segmentation for nerve/sinus proximity, implant planning, graft volume estimation.

Outcome: Safer placement, reduced complications, shorter OR time.

General Dentistry

Use cases: Chairside CADe, automated documentation, recall/risk analytics, claims support.

Outcome: Time savings for clinicians; improved acceptance of comprehensive care plans.

By Distribution Channel

Direct Sales (dominant, 2024)

Why clinics choose it: Solution consulting, enterprise contracting, implementation support, bundled training/validation, and SLA-backed uptime.

DSO angle: Standardized contracts across dozens/hundreds of practices; faster security/legal review cycles.

Online Platforms & Digital Marketplaces (fastest ahead)

Why growing: Self-serve trials, transparent pricing, instant provisioning, rich education (demos, reviews, webinars).

Best fit: Tech-forward solo/mini-groups; add-on modules to existing cloud PMS without long sales cycles.

By Region

North America (lead, 2024)

Market shape: High digital adoption, strong DSO presence, heavy imaging volumes, and active push into AI-assisted RCM/claims.

Execution notes: Frequent cloud rollouts, strong emphasis on compliance, training/credentialing programs accelerate uptake.

Revenue profile: Largest absolute spend; early adopters of integrated “smart platform” stacks.

Asia Pacific (fastest growth, 2025–2034)

Drivers: High disease burden, rapid clinic modernization, government digital-health momentum, and cloud leapfrogging.

Country contours:

China: Policy-led quality upgrades; CBCT/IOS penetration rising; AI aids throughput in urban centers.

India: Access gaps and workforce constraints make AI triage/decision support attractive; strong interest in affordable cloud tools.

Japan/Korea: High imaging standards; precision-driven practices receptive to AI QA and design automation.

Go-to-market: Price-sensitive tiers, multilingual UX, low-IT installs; training and clinical validation localized.

Europe (notably growing)

Context: High tooth-loss prevalence and strong insurance/Gov schemes; rigorous data protection requires clear compliance postures.

Adoption: Imaging AI + prostho design popular; emphasis on auditable, explainable outputs and CE-marked pathways.

Latin America

Pattern: Urban private chains lead adoption; cloud reduces capex barriers; growing interest in AI-assisted aligner planning and claims support.

Needs: Spanish/Portuguese workflows, flexible pricing, offline-tolerant features.

Middle East & Africa (MEA)

Hotspots: GCC private groups and teaching hospitals piloting AI imaging/CBCT analytics; Africa early but mobile-first tele-triage shows promise.

Key asks: Vendor training, local partner support, hybrid cloud/on-prem options.

Top 5 FAQs

-

What is the market size and growth outlook?

US$ 459.6 Mn (2024) → US$ 559.2 Mn (2025) → US$ 3,263.9 Mn (2034) at 21.78% CAGR. -

Which region leads and which grows fastest?

North America leads (2024) on digital adoption/DSOs; Asia Pacific grows fastest (2025–2034) on population needs and policy support. -

What solutions dominate today?

AI-powered imaging/diagnostics dominate 2024; AI in orthodontics & prosthodontics grows fastest through 2034. -

Which deployment wins?

Cloud dominates and expands fastest; on-prem remains relevant for offline continuity and one-time licensing models. -

When does the market cross US$ 1 Bn?

Around 2028, consistent with the 21.78% growth path from US$ 559.2 Mn (2025).

Access our exclusive, data-rich dashboard dedicated to the dental market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6142

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest