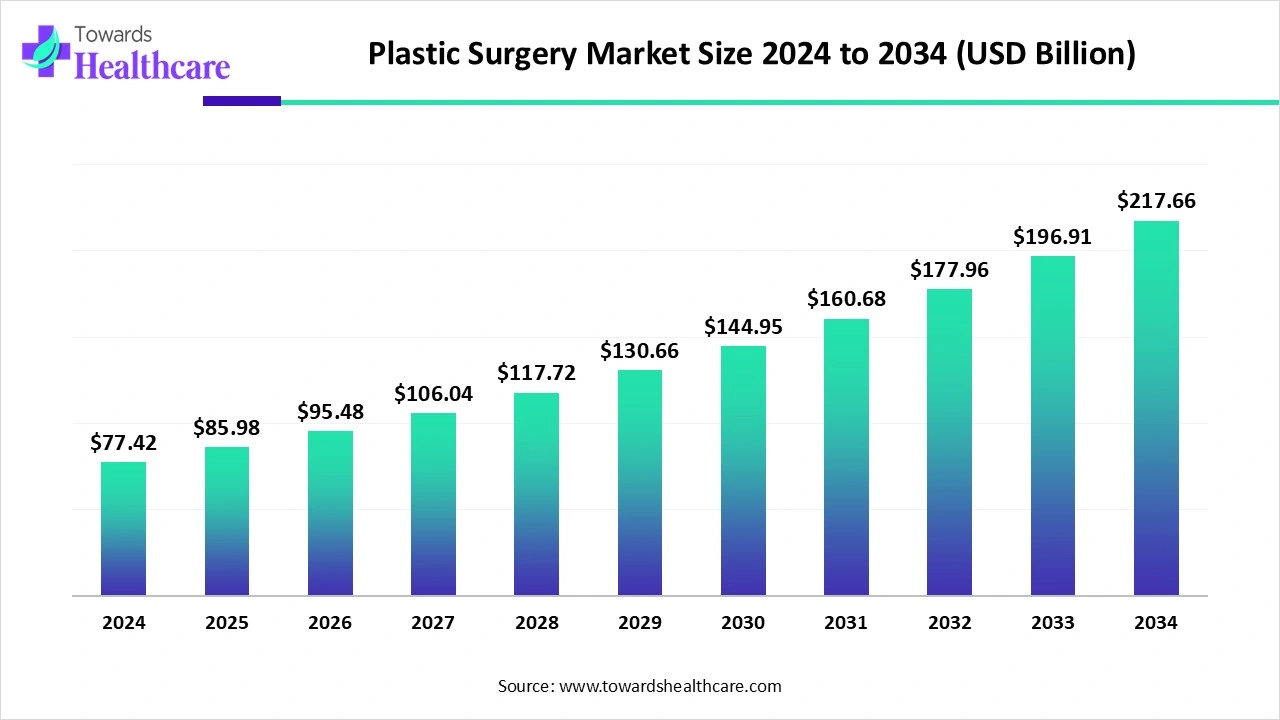

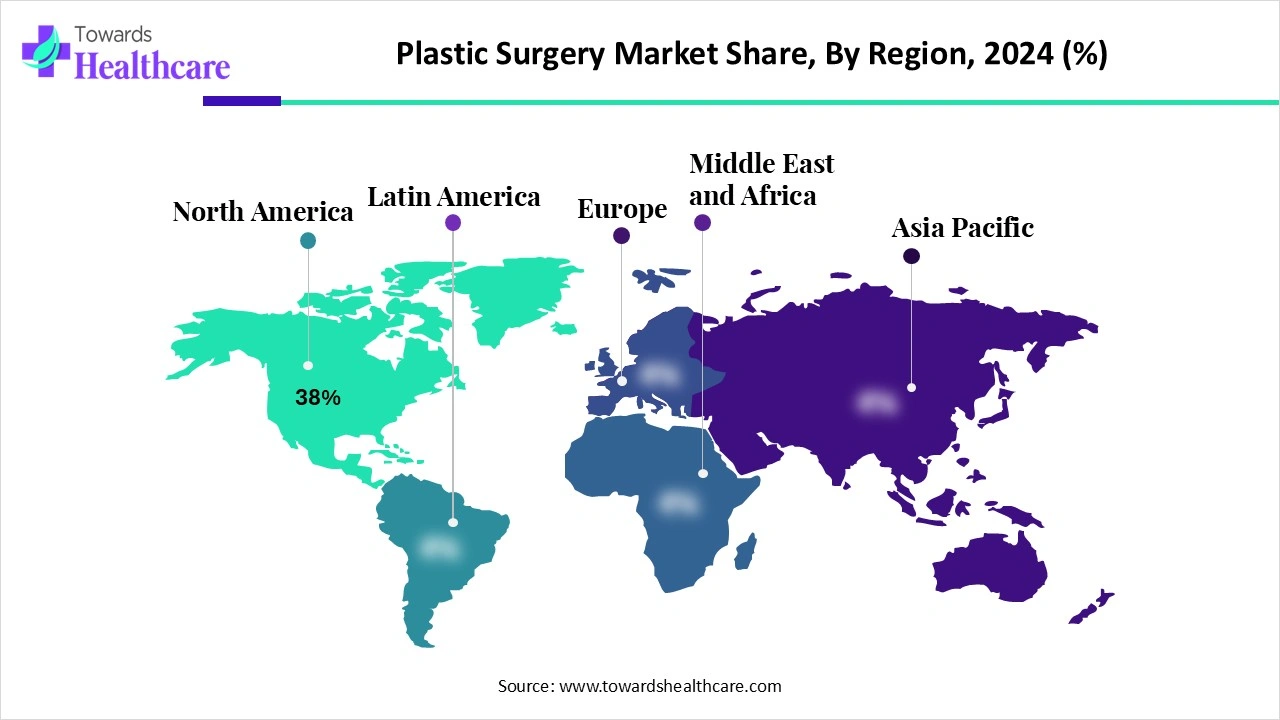

The global plastic surgery market stands at USD 77.42B in 2024, climbs to USD 85.98B in 2025, and is projected to reach USD 217.66B by 2034 (11.06% CAGR, 2025–2034), led by North America (38% share, 2024) and rapid Asia Pacific expansion.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5913

Market size

Total size & trajectory

●2024: USD 77.42B

●2025: USD 85.98B

●2034: USD 217.66B

CAGR (2025–2034): 11.06%

By procedure type

●Surgical procedures: 62% share (2024); durable outcome demand in rhinoplasty, liposuction, body contouring sustains revenue base.

●Non-surgical procedures: fastest growth through 2034; injectables (toxins/fillers), lasers, skin tightening expand patient base with low downtime.

By end user

●Specialty aesthetic clinics: 55% share (2024); specialization, privacy, advanced devices concentrate spend.

●Ambulatory surgical centers (ASCs): fastest growth; same-day surgeries, cost efficiency, reduced infection risk.

By technology

●Traditional surgical techniques: 60% revenue (2024); gold-standard for complex corrections.

●Minimally invasive & energy-based tech: fastest growth; RF/ultrasound/laser/cryolipolysis/endoscopic systems compress recovery times.

Regional scale

●North America: 38% share (2024) with high spend, KOLs, early tech adoption.

●Asia Pacific: fastest CAGR on rising incomes, medical tourism, and K-beauty influence.

●Europe, Latin America, MEA: steady growth via aging demographics, tourism corridors, and improving access.

Market trends

Shift to minimally invasive: Botox/fillers/laser therapies surge; ISAPS reports ~19.1M non-surgical procedures in 2023 alongside 15.8M surgical (+5.5% YoY).

Procedure mix pivot: Liposuction leads surgical volume (2.2M cases, 2023); breast augmentation, blepharoplasty, rhinoplasty, abdominoplasty follow.

Regulatory-backed product flow: FDA approvals—Restylane Eyelight (June 2023) for tear troughs; SKINVIVE by JUVÉDERM (May 2023) for cheek smoothness—expand indications and refresh injector pipelines.

Energy-based platforms upgrade: RF microneedling + lasers (e.g., Cutera Secret DUO, 2023) deliver texture/tone improvements with modular, stackable protocols.

Demographic broadening: Rising male and millennial adoption; growing acceptance reduces stigma; social media filters/selfie culture amplify demand.

Clinic format evolution: Specialty clinics (55% share) and ASCs lead with concierge workflows, bundled pricing, and shorter stays.

Digital front doors: Virtual consults, 3D/AR visualization, and mobile post-op check-ins improve conversion and adherence.

Medical tourism corridors: Korea, Thailand, Mexico, Turkey, and India attract price-sensitive patients for standardized procedures.

Implant innovation: Biocompatible, form-stable implants and IDEAL/“structured” options emphasize safety and natural feel.

Combination therapy protocols: Toxin + filler + energy devices + skincare sequences offer incremental, natural results with fewer downtimes.

10 deep AI roles & impacts

●Outcome simulation: AI-powered 2D/3D morphing personalizes expectations, improving consent quality and conversion.

●Treatment planning: ML models optimize incision placement, implant sizing, lipo volumes, and sequence timing to reduce revisions.

●Risk stratification: Predictive analytics flag DVT/infection/anesthesia risk using EHR + imaging + lifestyle inputs.

●Imaging triage: AI reads facial/body scans to quantify symmetry, texture, laxity, and fat distribution for objective baselines.

●Intra-op guidance: Computer vision assists with plane identification and device energy dosing; robotic aids stabilize motions.

●Inventory intelligence: Forecasts toxin/filler turns, laser tips, and implant SKUs to cut stockouts and write-offs.

●Revenue cycle optimization: NLP automates documentation, coding for reconstructive indications, and denial analytics.

●Patient acquisition: Look-alike modeling and sentiment analysis refine marketing, lowering cost per booked consult.

●Post-op monitoring: App-based photo checks with AI wound assessment detect seroma/infection early, prompting tele-follow-ups.

●Quality benchmarking: De-identified multi-center data trains models comparing techniques, devices, and providers for continuous improvement.

Regional insights

North America (38% share, 2024)

Drivers: High disposable income, insurer financing for reconstructive needs, dense KOL networks, and device availability.

Procedure mix: Strong injectables and body contouring; breast aesthetics and mommy makeovers remain core.

Channel dynamics: Corporate DSOs/MSOs scale specialty clinics; ASCs expand block time for high-throughput surgeons.

Asia Pacific (fastest CAGR)

Demand engines: K-beauty, social media aesthetic ideals, and rising middle-class spend.

Tourism: Korea/Thailand hub for facial contouring, rhinoplasty, and skin lasers; competitive pricing + high quality.

Localization: Preference for subtler, natural results; fast adoption of energy-based devices and skincare maintenance cycles.

Europe

Mature standards: Strong regulation, board certification clarity; steady growth in anti-aging injectables.

Tourism & access: Spain, Germany, Italy active in cross-border care; clinic clusters with multilingual staff.

Demographics: Aging population sustains eyelid, face/neck lifts; prevention-focused toxin/filler regimens rise.

Latin America

Cultural affinity: Brazil and Mexico anchor high surgical volumes (body contouring, gluteal shaping).

Price arbitrage: International patients blend tourism with procedures; branded surgeons elevate destination appeal.

Device adoption: Growing RF/laser use in premium urban clinics; financing plans widen access.

Middle East & Africa

Premium hubs: UAE/Saudi premium centers emphasize privacy, bundled post-op hotel recovery.

Patient profile: Younger, high-spend consumers; non-surgical first, surgical upgrades later.

Capacity build-out: Import reliance for devices; training partnerships expand certified provider base.

Market dynamics (integrating given data)

Drivers

Rising aesthetic focus & anti-aging demand: Social media + celebrity influence lift volumes; ISAPS +5.5% in 2023.

Tech advances: Minimally invasive & energy-based tech accelerating; FDA approvals (2023) feed injector pipelines.

Access models: Specialty clinics (55% share) and ASCs streamline care, reduce cost/time, and improve experience.

Restraints

High procedure costs: Limited reimbursement for cosmetic procedures restricts lower-income adoption.

Workforce & training gaps: Skilled surgeon/device-operator availability varies by region.

Regulatory heterogeneity: Cross-border differences in product approvals and advertising rules add friction.

Opportunities

AI, robotics, 3D simulation: Precision + personalization reduce revisions and elevate satisfaction.

APAC & tourism: Fastest regional CAGR via rising incomes, K-beauty pull, and destination clinics.

New indications/devices: Tear trough (Restylane Eyelight) and skin quality (SKINVIVE) expand recurring revenue.

Risks

Safety & ethics: Over-treating, counterfeit products, and unqualified providers can erode trust.

Macroeconomics: Elective spend is sensitive to interest rates and consumer confidence.

Top 10 companies

Allergan Aesthetics (AbbVie)

Products: BOTOX, JUVÉDERM family incl. SKINVIVE, CoolSculpting.

Overview: Global aesthetics leader across toxins, fillers, body contouring.

Strength: Broadest injector portfolio, training ecosystems, strong brand equity.

Johnson & Johnson (Mentor & Codman Neuroscience)

Products: Mentor breast implants/expanders; adjunct surgical tools.

Overview: Tier-1 surgical presence; standardized implant systems.

Strength: Quality reputation, surgeon trust, global supply reliability.

Galderma

Products: Dysport (toxin), Restylane fillers incl. Eyelight, skincare adjacencies.

Overview: Pure-play dermatology/aesthetics with hyaluronic acid leadership.

Strength: Continuous line extensions, indication breadth, injector education.

Merz Aesthetics

Products: Xeomin (toxin), Belotero, Radiesse; energy devices in select markets.

Overview: Neuromodulator + biostimulatory filler expertise.

Strength: Natural-look positioning, longevity data, clinic partnerships.

Sientra, Inc.

Products: Breast implants, reconstructive solutions.

Overview: Focused breast aesthetics platform in the U.S.

Strength: Patient-safety messaging, surgeon-centric service.

GC Aesthetics

Products: Implants/expanders; surgical accessories.

Overview: Europe-anchored implant vendor with multi-brand reach.

Strength: Portfolio depth across sizes/shapes; competitive pricing.

Teoxane Laboratories

Products: Teosyal HA fillers; skincare synergy.

Overview: Swiss R&D-driven filler specialist.

Strength: Gel rheology expertise; natural outcomes; injector training.

Sinclair Pharma

Products: Ellansé (biostimulatory), Silhouette Soft (threads).

Overview: Collagen-stimulating portfolio for longer-lasting lift/volume.

Strength: Differentiated, longevity-focused solutions.

InMode Ltd.

Products: RF platforms (BodyTite, FaceTite, Morpheus8).

Overview: Minimally invasive RF contouring and skin tightening.

Strength: Procedure economics for clinics; celebrity awareness.

Cynosure (Hologic)

Products: Laser/energy devices (Picosure, TempSure, Icon).

Overview: Multi-application platforms for pigment, hair removal, texture.

Strength: Diverse indications; service footprint; strong capital-equipment brand.

Latest announcements

Modern Plastic Surgery (2025): Nationally recognized clinic launched a Monthly Event Series (kickoff during Women’s Month, co-hosted with Only in Dade Cares), signaling brand building, community engagement, and pipeline generation via education-led marketing.

AirSculpt Technologies (Aug 2024): Opened Columbus center with two ORs enabling parallel cases; added AirSculpt skin tightening, expanding from fat removal to comprehensive contouring—raises revenue per patient and cross-sell rates.

Cutera (Sep 2023): Rolled out Secret DUO combining two non-ablative fractional technologies usable independently or together; modularity lets clinics tailor downtime vs. results and address multiple concerns in one session.

Recent developments

FDA fillers momentum (2023): Restylane Eyelight targets under-eye volume loss with NASHA HA; SKINVIVE by JUVÉDERM brings microdroplet HA for cheek smoothness up to ~6 months—both expand “skin quality” and tear-trough niches.

Procedure volume growth: ISAPS +5.5% in 2023; lipo #1 surgical procedure (2.2M cases), reflecting body-contouring priority and synergy with RF tightening.

Facility model upgrades (2024): New ASC/clinic openings (e.g., AirSculpt) show scale economics, standardized protocols, and higher throughput for elective demand surges.

Segments covered

Top 5 FAQs

-

What is the market size now and in the future?

USD 77.42B (2024) → USD 85.98B (2025) → USD 217.66B (2034) at 11.06% CAGR (2025–2034). -

Which region leads and which grows fastest?

North America leads with 38% (2024); Asia Pacific grows fastest on incomes, beauty culture, and tourism. -

Which procedures dominate revenue?

Surgical (62% share, 2024) dominate revenue; non-surgical grow fastest due to low downtime and repeatability. -

Which care settings are most important?

Specialty aesthetic clinics (55% share, 2024) lead; ASCs expand quickest for cost-efficient same-day surgeries. -

What innovations are shaping demand?

FDA-cleared fillers (Restylane Eyelight, SKINVIVE), energy devices (e.g., Secret DUO), AI planning/monitoring, and RF/ultrasound tightening.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/5913

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest