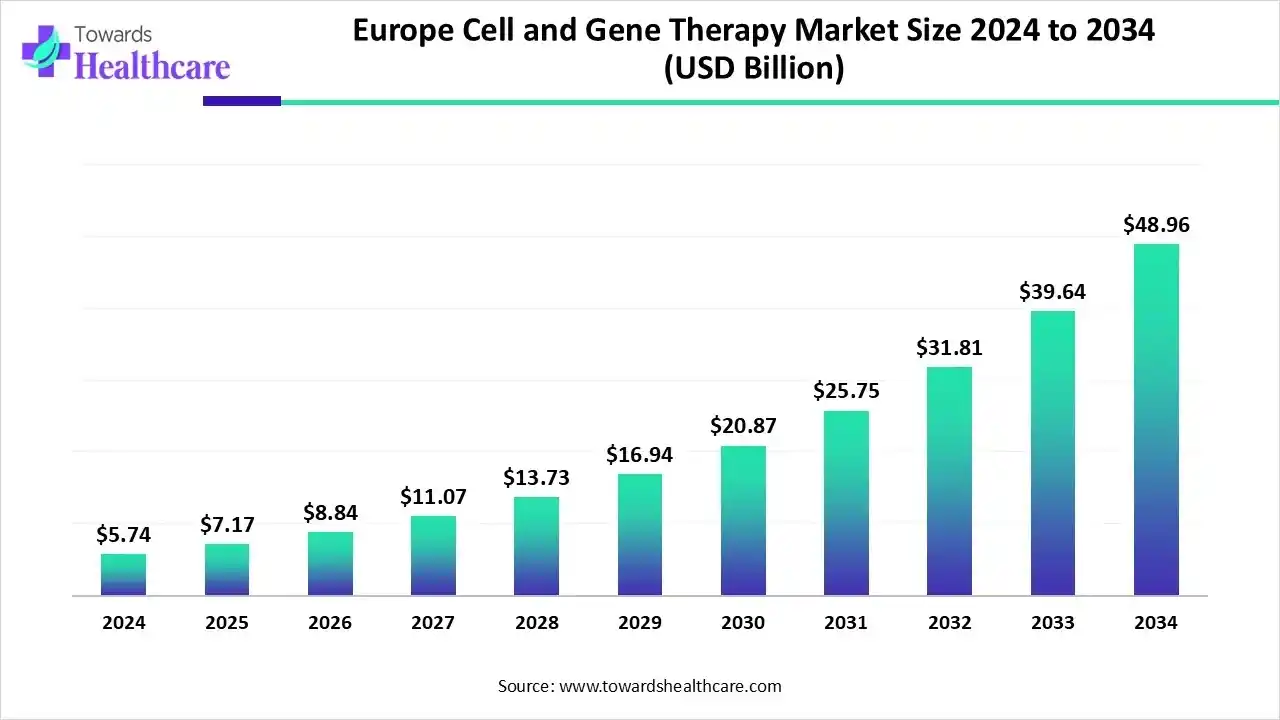

Europe cell and gene therapy market is US$2.74B in 2024, set to reach US$7.17B in 2025 and US$48.96B by 2034 at a 23.90% CAGR (2025–2034), propelled by EMA-backed approvals, Horizon Europe funding, and rapid uptake of CAR-T.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6295

Market Size (in-depth, point-wise)

●2024 base: US$2.74B; demand anchored by cell therapy (58% share), viral vectors (72%), autologous cell source (62%), clinical-scale production (67%), and biopharma/biotech end users (52%).

●Near-term step-up (2025): US$7.17B with pipeline conversions and initial scale-up of allogeneic platforms; gene therapy enters fastest-growth phase (2025–2034).

●Long-term projection (2034): US$48.96B, reflecting shift from clinical-scale → commercial-scale as closed/automated systems mature.

●Compound growth: 23.90% CAGR (2025–2034) supported by oncology dominance (~48% 2024) and rare disease acceleration.

●Regional anchor: Germany 28% share (2024); leadership reinforced by a national GCT strategy and expanding vector capacity.

●Capital flows (2025 highlights): SpliceBio US$135M Series B; HAYA Therapeutics US$65M Series A; Laverock >£20M seed+—fueling platform and pipeline build-out.

●Policy tailwinds: EMA/CHMP multi-asset positive opinions (Aug-2025); EU Green Deal and proposed EU Biotech Act lower scale-up frictions and favor greener bioprocessing.

●Modality mix shift: Autologous → Allogeneic growth for throughput and cost; non-viral vectors accelerate on safety/cost manufacturing advantages.

●Use-case concentration: Oncology remains the adoption beachhead; rare genetic disorders lead future growth via curative intent.

●Manufacturing inflection: Transition from manual, variable clinical workflows to automated, standardized commercial platforms unlocks capacity and reduces COGS.

Market Trends

●Regulatory momentum: EMA/CHMP recommended 10 new medicines + 8 biosimilars (Aug-2025); multiple label expansions—shortening time to market.

●Funding scaffolding: Horizon Europe and national programs de-risk trials, especially for CAR-T and rare disease assets.

●Green manufacturing push: EU Green Deal drives closed-loop, energy-efficient bioprocessing; vendors differentiate on sustainability metrics.

●Hospital-based manufacturing pilots: EASYGEN consortium (Aug-2025; €8M; Fresenius-led) targets few-day personalized cell therapy turnaround.

●Strategic M&A/CDMO consolidation: Formation of Minaris Advanced Therapies and vector-scale deals (e.g., SK pharmteco LVV 200L CGMP batch in Paris ecosystem).

●Vector tech bifurcation: Viral vectors (72% 2024) dominate; non-viral (LNPs, physical methods) surge on immunotoxicity and cost advantages.

●Autologous today, allogeneic tomorrow: Autologous 62% (2024) share; allogeneic pipelines scale with universal donor strategies.

●Oncology first, rare disease next: Oncology ~48% (2024); rare genetic disorders expected fastest growth on single-gene correction potential.

●AI permeation: From design → QC → release (details below) improving yields, safety, and time-to-patient.

●Commercial-scale readiness: Clinical-scale 67% (2024) now; the commercial-scale segment becomes the fastest-growing through 2034.

10 Deep Ways AI Impacts This Market

●In-silico vector design: AI optimizes AAV capsids/LVs for tropism, payload, and immunogenicity trade-offs, raising effective dose success odds.

●Promoter/construct optimization: ML models score promoters, enhancers, and UTRs for expression stability across tissues and patients.

●Manufacturing set-point control: Reinforcement learning tunes MOI, cell density, and feed strategies to maximize vector yield and CQAs.

●Automated eBR & deviation analytics: NLP on batch records detects anomaly patterns, cutting batch failure rates and CAPA cycles.

●Rapid QC release: Computer vision + ML for sterility, identity, potency proxies to accelerate lot release without compromising safety.

●Patient stratification: Multi-omics fusion models select responders for CGT, reducing trial size and improving probability of technical success.

●Safety prediction: Off-target/oncogenicity risk scoring for gene editing; immunogenicity forecasts to guide premedication/regimens.

●Digital twins for scale-up: Virtual bioreactor twins translate process from 2L→200L with fewer experiments and higher transfer fidelity.

●Hospital workflow orchestration: Scheduling/throughput AI shortens vein-to-vein times for CAR-T; predicts bed/OR and apheresis slots.

●Post-market pharmacovigilance: Signal detection on EHR/registry data identifies long-term AEs, informing label updates and REMS.

Regional Insights

Germany (28% 2024; leader)

●Policy & strategy: National GCT strategy via BMBF/BIH coordination; clear hospital-academia-industry interfaces.

●Manufacturing muscle: LVV/AAV capacity builds (e.g., 200L CGMP LVV initiatives), strong automation vendors.

●Clinical density: High trial throughput in oncology and rare disease; reimbursement pilots for ATMPs.

United Kingdom

●Company cluster: Oxford Biomedica, Orchard, Autolus, Adaptimmune, GSK, AstraZeneca drive end-to-end ecosystem.

●Translational hubs: Catapult centers expedite process development and scale-up.

●Policy continuity: MHRA/EMA alignment pathways for EU access via partnerships.

France

●Innovation nodes: Sanofi, Cellectis, GenSight; strong gene-editing pedigree.

●Public funding: Robust academic networks; expanding hospital-based production pilots.

●Therapy focus: Oncology, ophthalmology, and metabolic indications.

Italy

●Legacy strengths: MolMed heritage and hospital-linked manufacturing; expanding rare disease programs.

●CDMO linkages: Access to pan-EU vector networks; growing GMP talent pool.

●Regulatory support: Streamlined ATMP approvals via national competence centers.

Spain

●Trial growth: Rising AAV ophthalmology and hematology trials.

●Cost advantage: Competitive bioprocessing OPEX; strong academic consortia.

●Infrastructure: Upgrades to closed systems improve batch consistency.

Nordics (Sweden/Denmark/Norway)

●Precision medicine focus: Registry depth enables long-term outcomes capture.

●Bioprocess innovation: Sustainable, low-footprint facilities aligned with Green Deal.

●Access pathways: Early patient access schemes for rare diseases.

Netherlands

●uniQure anchor: AAV heritage and commercial know-how.

●Logistics: Central EU location for expedited distribution.

●Tech transfer: Strong university-industry patenting pipeline.

Market Dynamics

Drivers

●EMA/CHMP approvals and supportive CAT pathways; Horizon Europe and national grants.

●Oncology adoption (48% 2024) and CAR-T popularity; Germany 28% regional engine.

●Capital inflows (SpliceBio US$135M, HAYA US$65M, Laverock >£20M).

Restraints

●High COGS and variable yields (autologous); limited vector capacity bottlenecks.

●Complex QA/QC release and vein-to-vein logistics.

●Reimbursement uncertainties for ultra-rare indications.

Opportunities

●Allogeneic and non-viral platforms for cost/scale breakthroughs.

●Green bioprocessing differentiation; hospital-based rapid manufacturing (EASYGEN).

●AI-driven process control and safety—shorter cycles, higher success rates.

Challenges

●Talent shortages in GMP/automation; cross-border regulatory variability.

●Long-term safety surveillance requirements.

●Transition risk from clinical (67%) → commercial scale without disrupting supply.

Top 10 Companies

Oxford Biomedica (UK)

●Products: LVV development & manufacturing; platformed CAR-T/CAR-NK vectors.

●Overview: Premier EU lentiviral CDMO with end-to-end capabilities.

●Strength: Deep LVV IP, quality track record, large-scale suites.

Orchard Therapeutics (UK)

●Products: Ex vivo autologous gene therapies for rare inherited disorders.

●Overview: Focused on hematopoietic stem cell gene therapy.

●Strength: Curative intent data; pediatric rare disease expertise.

Autolus Therapeutics (UK)

●Products: Next-gen CAR-T programs for hematologic malignancies.

●Overview: Modular CAR designs with safety switches.

●Strength: Engineering sophistication; manufacturing control.

GlaxoSmithKline – GSK (UK)

●Products: Oncology/rare disease CGT portfolio; precision therapeutics expansion.

●Overview: Big pharma scale, BD-driven pipeline (e.g., 2025 precision dealmaking).

●Strength: Global development, market access, and PV infrastructure.

AstraZeneca (UK/Sweden)

●Products: In vivo cell therapy platforms; ENaBL lentiviral nanobody approach.

●Overview: Oncology-centric CGT with novel delivery.

●Strength: Broad oncology footprint; rapid clinical translation.

Sanofi (France)

●Products: Gene therapies and immunology focused programs.

●Overview: Integrated research, manufacturing, and market access.

●Strength: Late-stage development engine and global reach.

Cellectis (France)

●Products: Allogeneic gene-edited cell therapies (TALENs).

●Overview: Pioneering gene-editing platform company.

●Strength: Off-the-shelf ambition; editing know-how.

Miltenyi Biotec (Germany)

●Products: Cell processing systems (CliniMACS), reagents, and tools.

●Overview: Enabling technology leader across CGT workflows.

●Strength: Ubiquitous footprint in GMP cell processing.

Evotec (Germany)

●Products: End-to-end discovery to CMC services; RNA/cell therapy platforms.

●Overview: Partner-centric model with EU/US facilities.

●Strength: Scale, data platforms, and BD network.

uniQure (Netherlands)

●Products: AAV gene therapies targeting monogenic diseases.

●Overview: AAV pioneer with clinical and commercial experience.

●Strength: Vector platform depth; manufacturing expertise.

Latest Announcements

AstraZeneca (Mar-2025): Definitive agreement to acquire EsoBiotec to advance in vivo cell therapies using ENaBL—aims for minutes-scale delivery vs current complex workflows.

BioIVT (Oct-2025): Showcased expanded cellular solution portfolio across major CGT conferences—broader access to high-quality inputs for R&D/QC.

ABALETTA Bio (Jun-2025): Released new clinical/translational data for rese-cel in autoimmune indications (RESET programs), broadening CGT applicability.

Minaris Advanced Therapies (May-2025): Formed by combining Minaris Regenerative Medicine with WuXi AT (US/UK ops) under Altaris—global CDMO scale-up.

SK pharmteco Cell & Gene Europe / AP-HP / Imagine (Feb-2025): Contract for 200L CGMP LVV clinical batch and regulatory support—EU LVV capacity uplift.

EMA/CHMP (Aug-2025): Positive opinions for 10 new medicines, 8 biosimilars, plus 4 generics and multiple new indications—pipeline acceleration.

EASYGEN (Aug-2025): €8M EU-backed hospital-based automated platform for personalized cell therapies (Fresenius-led).

European Commission (Jul-2025): Long-term life sciences strategy; proposed EU Biotech Act—policy momentum for CGT scale-up.

Recent Developments

●Consolidation and capacity build: Minaris Advanced Therapies creation; SK pharmteco LVV 200L run in Paris ecosystem.

●Capital rounds energizing pipelines: SpliceBio (US$135M), HAYA (US$65M), Laverock (>£20M).

●Oncology lead use-case: CHMP opinions + CAR-T popularity sustain oncology dominance (~48% 2024).

●Sustainability shift: EU Green Deal catalyzes closed-loop, low-energy CGT manufacturing adoption.

●AI integration: Workflow automation from construct design → PV improving cycle times and QA.

Segments Covered

Therapy Type

Cell Therapy (58% share, 2024)

Modalities & use-cases

●Immune cell therapies: CAR-T (hematologic cancers), TCR-T (solid/viral antigens), NK cells (off-the-shelf potential).

●Stem/progenitor cells: MSCs for immunomodulation; HSCs for ex-vivo gene correction; iPSCs for scalable allogeneic banks.

Why it leads today

●Clinically validated paths: Multiple EMA-approved CAR-T lines; clearer CMC and hospital workflows.

●Predictable outcomes in oncology: Rapid measurable responses; defined endpoints (ORR, MRD negativity, PFS).

Manufacturing & logistics

●Autologous dominance (see below): Apheresis → engineering → release; vein-to-vein orchestration is critical.

●Key bottlenecks: Viral vector supply, QC release time, fresh vs cryo chain reliability.

Cost & quality levers

●Closed systems, automated cell selection/activation, real-time analytics to cut batch failures and COGS.

Near-term evolution

●Scaleout to more centers; allogeneic NK/iPSC-derived cells to reduce lead times and cost per dose.

Gene Therapy (fastest growth 2025–2034)

Modalities

●Gene augmentation: Functional copy delivery for monogenic disease.

●Gene editing: CRISPR/TALENs/ZFNs for precise correction or knockout.

●RNA-based: mRNA for transient protein expression; siRNA/ASO for gene silencing.

Why it accelerates

●Curative intent in rare disorders; maturing vector platforms; expanding payer experience with outcomes-linked models.

CMC focus

●Vector productivity (capsid design, promoter strength), purity (empty/full capsid ratios), robust analytics (potency, biodistribution).

Clinical design trends

●Basket trials by genotype; long-term follow-up plans for durability and late AEs.

Therapeutic Area

Oncology (48% in 2024)

Scope

●Hematologic (ALL, DLBCL, MM), pediatrics, and increasingly solid tumors (gating antigen selection, TME modulation).

Why it dominates

●Clear surrogate endpoints; hospital infrastructure for apheresis/infusion; strong clinician familiarity.

What’s next

●Multiplex edits (armor, knock-outs), logic-gated CARs, combination with checkpoint inhibitors.

Rare Genetic Disorders (fastest CAGR)

Scope

●Hematology (hemophilia, hemoglobinopathies), neuromuscular, ophthalmology, metabolic diseases.

Growth drivers

●Single-gene targets, registries enabling rapid identification, advocacy-led trial recruitment.

Market access

●Outcomes-based contracts, newborn screening linkages, long-term evidence capture via national registries.

Others (Neuro, Cardio, Ophthalmology, Metabolic/Endocrine, Infectious)

Neuro: AAV to CNS (intrathecal/intraparenchymal); challenge = immune responses, dosing windows.

Cardio: Regenerative cell therapy for ischemia/heart failure; endpoints require longer follow-up.

Ophthalmology: Local delivery, immune privilege, sensitive functional endpoints (BCVA, FST).

Metabolic/Endocrine: Liver-tropic AAV/LNP; lifelong durability and re-dosing strategies are key.

Infectious: Engineered immune cells/antibodies for refractory infections; hospital stewardship pathways matter.

Vector Type (Gene Therapy)

Viral Vectors (72% in 2024)

Families & fits

●AAV: Non-integrating, durable expression; favored for eye, liver, muscle.

●Lentivirus (LV): Integrating; gold standard for ex-vivo HSC/immune cell modification.

●Retrovirus/Adenovirus: Niche uses; adenovirus for high payload but immunogenic.

Why dominant

●High transduction efficiency, established QC frameworks, known toxicology.

Manufacturing priorities

●Upstream yield (HEK293/suspension), downstream purification (chromatography), accurate titering (ddPCR).

Risks to manage

●Immunogenicity (pre-existing NAbs), insertional mutagenesis (integrating vectors), dose-related toxicity.

Non-Viral Vectors (fastest growth)

Approaches

●LNPs: mRNA/siRNA delivery; scalable and re-dosable.

●Physical methods: Electroporation for ex-vivo cell engineering (CAR-T/NK).

Why they’re rising

●Lower immunotoxicity, simpler scale-up, reduced COGS, flexible payloads.

Challenges

●Tissue tropism, endosomal escape, durability—addressed through lipid chemistry and targeting ligands.

Cell Source (Cell Therapy)

Autologous (62% in 2024)

Strengths

●Minimal graft-versus-host, high response in hematologic cancers, well-trodden regulatory path.

Constraints

●Patient fitness, long lead times, batch-of-one economics, site-to-site variability.

Improvements

●Point-of-care automation, standardized release assays, cryo logistics optimization.

Allogeneic (fastest growth)

Value proposition

●Off-the-shelf inventory, immediate availability, lower per-dose cost potential, easier scale economics.

Technical keys

●Gene edits to evade host immunity (HLA, CD52), graft persistence, reduced rejection.

Use-cases

●First in NK/iPSC-derived products; expansion toward T-cell therapies and regenerative indications.

Manufacturing Scale

Clinical-Scale (67% in 2024)

Characteristics

●Small-to-mid bioreactor volumes; semi-manual steps; extended QC turnaround; site-specific SOPs.

Pain points

●Batch variability, high labor burden, tech-transfer friction between sites, lengthy vein-to-vein times.

What’s changing

●Adoption of closed systems, electronic batch records, and automated analytics to raise right-first-time.

Commercial-Scale (fastest growth)

Defining features

●Standardized, automated, high-containment suites; platform processes; global release testing networks.

Benefits

●Lower COGS, higher throughput, reproducible CQAs, improved access for larger patient cohorts.

Readiness factors

●Robust comparability packages, global supply chain resilience, sustainability metrics (energy/water).

End User

Biopharma & Biotech (52% in 2024)

Roles

●Discovery, vector engineering, IND/MAA ownership, CMC platforming, market access execution.

Needs

●Reliable vector and plasmid supply, rapid process development, partnerable CDMO capacity.

Metrics

●Probability of technical/regulatory success, time-to-first-in-human, COGS/dose, lot release cycle time.

Hospitals & Specialty Clinics (fastest growth)

Why growing

●Expansion of certified infusion/manufacturing centers; near-patient production pilots; integrated care pathways.

Operational focus

●Apheresis scheduling, cell handling SOPs, AE management, long-term follow-up.

Key enablers

●Point-of-care platforms, reimbursement frameworks, digital orchestration of vein-to-vein.

Academia & Research Institutes; CMOs/CROs

Academia/Institutes

●Early discovery, preclinical models, first-in-human trials, translational know-how.

CMOs/CROs

●Capacity bridging, tech-transfer, global QC/release, regulatory documentation support.

Strategic value

●Flex capacity during surges; specialized analytics; faster scale transitions.

Region (Europe)

Germany (≈28% share, 2024)

Why leader

●National GCT strategy; dense clinical networks; strong vector and device ecosystems.

Focus areas

●Oncology and rare diseases; expansion of GMP vector volumes (e.g., 200L LVV clinical batches).

System strengths

●Reimbursement pilots for ATMPs, high-quality registries, engineering talent base.

United Kingdom

Industrial base

●Oxford–London–Cambridge triangle with Oxford Biomedica, Orchard, Autolus, Adaptimmune, GSK, AstraZeneca.

Translational assets

●Catapult centers, strong tech-transfer culture, hospital manufacturing initiatives.

Access

●Rapid setup for first-in-human; EU access via partnerships and aligned standards.

France

Players

Sanofi, Cellectis, GenSight; strengths in editing and ophthalmology.

Infrastructure

●Public funding, Paris hospital networks, academic-clinical consortia.

Trajectory

●Allogeneic editing and ophthalmic AAV scale-up.

Italy

Legacy competency

●Longstanding hospital-linked manufacturing (e.g., ex-MolMed lineage).

Focus

●Oncology, rare disease; increasing CDMO partnerships.

Enablers

●Competence centers streamlining ATMP approvals and trials.

Spain

Momentum

●Ophthalmology and hematology AAV trials rising; cost-competitive GMP operations.

Network

●University-hospital consortia; upgrades to closed systems for consistency.

Opportunity

●Regional hubs for Southern Europe distribution.

Nordics (Sweden, Denmark, Norway)

Unique assets

●Population registries for longitudinal outcomes; strong clean-tech alignment.

Focus

●Precision medicine pilots, early access for rare disease programs.

Scale

●Boutique but high-quality manufacturing and data infrastructure.

Netherlands

Anchor

●uniQure AAV heritage; experienced in commercial pathways.

Logistics

●Central EU distribution, port access, efficient customs for cold chain.

R&D

●University-industry patenting and rapid clinical onboarding.

Top 5 FAQs (using given data)

-

What is the market size now and where is it heading?

US$2.74B (2024) → US$7.17B (2025) → US$48.96B (2034) at 23.90% CAGR (2025–2034). -

Which therapy type leads today?

Cell therapy (58% share, 2024); gene therapy is the fastest-growing through 2034. -

Which therapeutic area is largest?

Oncology (48% 2024); rare genetic disorders expected to grow fastest. -

What vectors and cell sources dominate?

Viral vectors (72% 2024) and autologous cells (62% 2024); non-viral and allogeneic are fastest-growing. -

Which region leads in Europe?

Germany (28% share, 2024) on strong R&D, policy, and manufacturing initiatives.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6295

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest