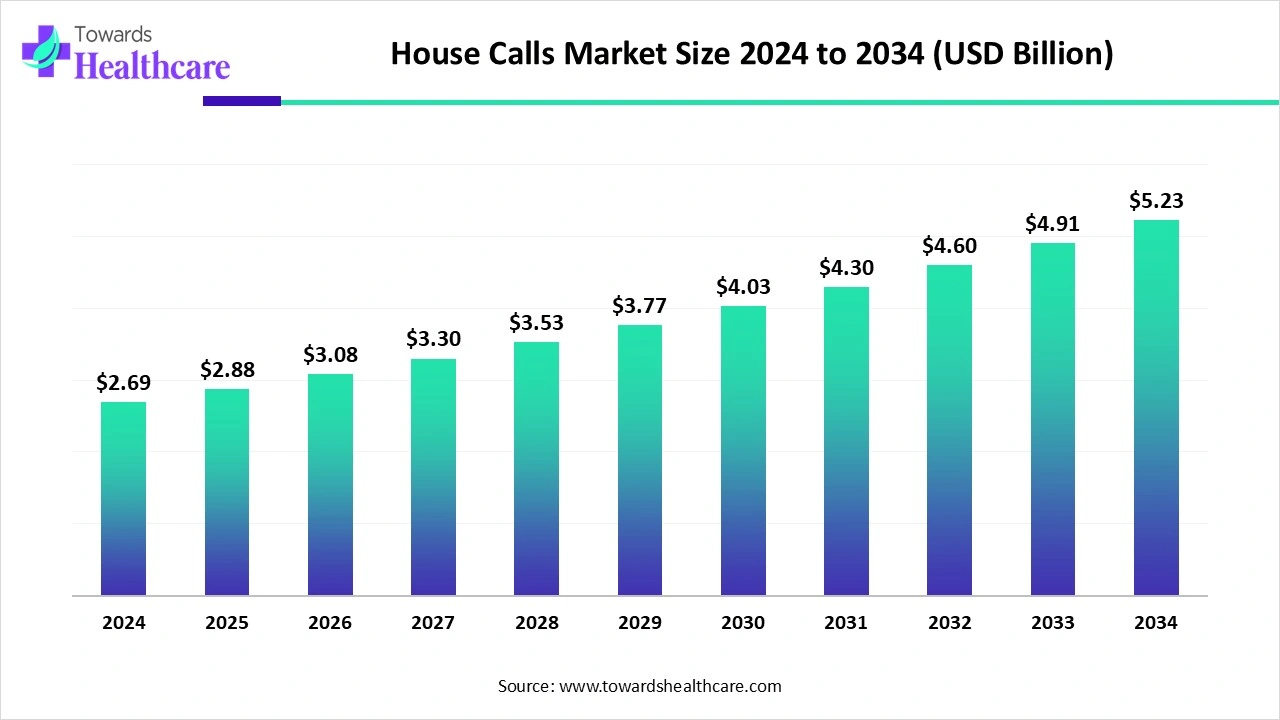

The global house calls market was US$ 2.69B in 2024, is US$ 2.88B in 2025, and is projected to reach US$ 5.23B by 2034 (CAGR 6.89%, 2025–2034), led by North America with Asia Pacific growing fastest.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6214

Market size

●Baseline & near-term: 2024 size US$ 2.69B → US$ 2.88B in 2025 (+7.1% YoY), reflecting post-pandemic normalization plus sticky demand for at-home care.

●Long-term projection: US$ 5.23B by 2034 at 6.89% CAGR (2025–2034), implying ~1.8× expansion over the period.

●Volume drivers embedded in size: aging population, chronic disease load, payer coverage expansion (private > public initially), and capacity shifts from hospitals to community/home.

●Mix effects shaping revenue realization: higher visit acuity under physician-led models (2024 leader) and rising telehealth-supported visits (fastest growth) increase revenue density per patient cohort.

●Utilization anchors: primary care visits held the largest 2024 share; chronic disease management is the fastest-growing throughput contributor.

●Setting & access: individual homes dominated revenue in 2024; assisted living facilities add incremental growth via scheduled rounds and integrated diagnostics.

●Payer contribution: private insurance led 2024 share; public insurance/government programs accelerate growth via pilot reimbursement and equity initiatives.

●Provider landscape: home healthcare agencies held the largest 2024 share; telemedicine providers are the fastest scalers via hybrid models and platform integration.

Market trends

Networked partnerships scale access: Providers align with insurers, senior living, and pharmacies to extend last-mile coverage and streamline claims.

●Insurance-backed home health expansion: Star Health (Jul 2024) launched Home Health Care across 50+ Indian cities with partners (Care24, Portea, CallHealth, Athulya), enabling cashless doorstep care and multi-disciplinary services.

●Government pilots mainstream the home as a care node: U.S. FDA (Apr 2024) “Home as a Health Care Hub” promotes equity and integration of home-based models into the wider system.

●At-scale in-home assessments: Optum HouseCalls (2024) delivered ~16M home visits, demonstrating operational feasibility and readmission reduction.

●Remote patient monitoring (RPM) maturation: HRS (Jan 2024) expanded RPM using wearables for continuous vitals and timely intervention.

●Consumer-grade diagnostics move in-home: Abbott (Jun 2024) OTC CGMs (Lingo, Libre Rio) widen metabolic monitoring use at home.

●Hybrid care becomes default: Telehealth triage + targeted in-person visits optimize clinician time and travel economics.

●Portable point-of-care (POC) tech proliferation: Mobile labs, imaging, and e-prescribing compress turnaround time at the bedside.

●Payment innovation: Private plans lead with faster approvals; public programs unlock growth via pilots for vulnerable/rural groups.

●Safety & preference effects: Avoidance of hospital-acquired infections plus continuity of care strengthens household adoption.

10 ways AI impacts the house calls market

●Predictive risk stratification: ML flags decompensation (e.g., heart failure flare) from RPM streams, scheduling pre-emptive home visits to avoid ER utilization.

●Dynamic routing & capacity orchestration: AI optimizes clinician travel routes, cluster scheduling by acuity/geography, and reallocates visits in real time after cancellations.

●Personalized care plans: Recommenders synthesize EHR + wearable data to tailor medication titration, diet, and rehab goals, updated continuously from home data.

●Virtual copilot during visits: On-device LLMs draft SOAP notes, surface guideline nudges, check drug–drug interactions offline, and generate after-visit summaries for patients.

●Automated triage & escalation: AI chat/intake classifies symptoms, captures PROs, and triggers urgent in-person dispatch or tele-consults, compressing time-to-care.

●Computer-vision vitals & wound analytics: CV estimates respiratory rate, edema trends, and wound healing from images, standardizing remote follow-up decisions.

●Adherence & behavior coaching: Nudging models time reminders to patient routines; anomaly detection flags missed meds or device non-use for outreach.

●Revenue cycle uplift: NLP pre-codes visits, maps documentation to payer policies, and predicts denial risk to tailor documentation in the visit itself.

●Population health targeting: Geospatial AI identifies underserved blocks with high chronic disease density to place mobile units and community partners.

●Quality assurance & training: AI audits visit recordings (where permitted) for guideline adherence, teaches micro-skills, and reduces variability across mobile teams.

Regional insights

North America (2024 leader)

●Adoption drivers: High private insurance penetration; strong provider–tech partnerships; consumer preference to avoid HAIs.

●Integration pilots: Public/private programs embedding preventive and chronic care into house calls raise baseline volumes.

●Operational maturity: Agencies standardize protocols, enabling scale (example: multi-million-visit programs).

●Constraints & responses: Staff shortages → hybrid telehealth + RPM to expand panel sizes without proportional headcount.

United States

●Demand themes: Continuity with known clinicians, preventive checkups at home, and trust in hybrid models.

●Channel expansion: Startups + pharmacies + senior living communities co-market bundles, improving uptake and logistics.

Canada

●Growth vectors: Chronic disease management and preventive home checkups; RPM + telehealth + mobile diagnostics elevate care quality in urban and rural routes.

●System fit: Universal coverage settings pilot targeted home-visit reimbursements for high-risk cohorts.

Asia Pacific (fastest CAGR)

●Demand formation: Rising awareness, disposable incomes, and a tech-savvy population adopt app-based booking and monitoring.

●Supply enablement: Expanding private networks and government initiatives to improve rural access; investments in digital health and connected devices.

●India spotlight: Insurer-led home health launches (cashless, multi-service) normalize the model beyond metros.

●Scalability note: Hybrid visit models reduce clinician travel friction across dense urban clusters.

Europe

●Adoption posture: Established community care frameworks; emphasis on chronic and senior care continuity at home.

●Policy tailwinds: National health services explore targeted reimbursement and post-acute pathways to reduce hospital load.

Latin America & MEA

●Emerging adoption: Urban pilots focus on urgent/primary visits plus RPM; public–private partnerships help bridge affordability and workforce gaps.

●Infrastructure focus: Connectivity and logistics investments are prerequisites; once in place, tele-supported models scale quickly.

Market dynamics

Driver — Convenience & continuity at home: Busy lifestyles and mobility limits push demand for scheduled in-home care; Optum’s ~16M visits (2024) illustrate improved satisfaction and fewer admissions.

Driver — Chronic disease & aging: Frequent monitoring, vaccination, and medication support make primary care visits the 2024 share leader and chronic management the fastest grower.

Driver — Tech enablement: Telehealth + RPM + mobile diagnostics shrink time-to-intervention; HRS (Jan 2024) and Abbott OTC CGMs (Jun 2024) widen home data flows.

Restraint — Operational costs: Vehicles, kits, portable devices, and travel time raise per-visit costs; uneven reimbursements challenge rural viability.

Opportunity — Telehealth & RPM scale: Hybrid care unlocks remote/underserved demand; FDA’s (Apr 2024) home-hub framing and insurer launches (e.g., Star Health, Jul 2024) expand covered use cases.

Structural shift — Care models: Physician-led models capture complex acuity today; telehealth-supported models outgrow on efficiency and reach.

Payer evolution: Private insurance led 2024 revenue; public programs accelerating via pilots for equity and early intervention.

Setting transition: Individual homes dominate; assisted living accelerates via scheduled rounds + on-site POC diagnostics.

Top 10 companies

DispatchHealth

Products/Services: On-demand urgent & advanced care at home; mobile teams; diagnostics and treatments on site.

Overview: U.S. footprint delivering ER-level interventions at home with payer partnerships.

Strengths: Rapid response logistics; payer integration; breadth from acute to post-acute episodes.

Teladoc Health (hybrid telehealth + home care expansion)

Products/Services: Virtual primary/urgent care, chronic care management; integrating in-home touchpoints.

Overview: Global telehealth leader extending into hybrid models for continuity.

Strengths: Massive member base; data/analytics stack; cross-payer relationships.

Visiting Physicians Association (VPA, U.S. Medical Management)

Products/Services: Physician-led primary and chronic care visits for homebound seniors.

Overview: Long-standing U.S. provider specializing in geriatric/complex patients.

Strengths: Physician density; Medicare experience; care coordination depth.

Housecall Providers (CareOregon)

Products/Services: In-home primary care, palliative care, and hospice services.

Overview: Nonprofit model integrated with Medicaid/Medicare populations.

Strengths: Value-based care expertise; integration with health plans; palliative capabilities.

Heal

Products/Services: App-based scheduled primary care visits; telehealth adjunct.

Overview: Tech-enabled U.S. provider targeting family medicine at home.

Strengths: User experience; digital scheduling; continuity with assigned PCPs.

AT HOME DOCTORS

Products/Services: Physician home visits (primary/urgent); diagnostics coordination.

Overview: Multi-city in-home medical service brand (home visit core).

Strengths: Physician-led acuity; personalized continuity; flexible visit windows.

House Call Doctor

Products/Services: After-hours urgent GP visits; home triage and treatment.

Overview: Focus on off-peak, home-based urgent primary care.

Strengths: Night/weekend coverage; fast response; patient convenience niche.

SOS Doctors

Products/Services: 24/7 physician house calls; urgent and routine care.

Overview: Rapid-response medical house calls with on-site treatments.

Strengths: Round-the-clock availability; multilingual teams in some markets; tourist/expat coverage.

My Doctor Medical Group

Products/Services: Concierge internal medicine; house calls for complex/chronic care.

Overview: High-touch model with integrated behavioral and preventive services.

Strengths: Concierge revenue mix; complex-case management; continuity.

TruDoc HealthCare

Products/Services: Telemedicine, remote monitoring, and coordinated in-home care.

Overview: Hybrid care platform for enterprise and consumer segments.

Strengths: Corporate/payer partnerships; scalable digital front door; RPM integration.

Latest announcements

Star Health & Allied Insurance (Jul 2024): Launched Home Health Care in 50+ Indian cities; cashless access via app/toll-free; partners include Care24, Portea, CallHealth, Athulya; services span nursing, elderly care, physio, diagnostics, and pharmacy—lowering total cost and widening access.

U.S. FDA (Apr 2024): Home as a Health Care Hub program to systemically integrate home-based care and promote equity for underserved populations, aligning devices, data, and workflows for in-home use.

Recent developments

Abhay HealthTech (Jul 2025): Expanded portfolio toward consumer-controlled preventive care—rapid diagnostic kits, telehealth, OTC wellness, hygiene; Assure/ActFast brands target home device accuracy and hypertension monitoring.

Abbott (Jun 2024): FDA clearance for OTC CGMs (Lingo, Libre Rio), leveraging FreeStyle Libre heritage to broaden at-home metabolic tracking and support hybrid home-care pathways.

Optum Health (2024): ~16M HouseCalls home visits delivered—evidence of scale feasibility, patient satisfaction, and admissions reduction.

HRS (Jan 2024): Expanded RPM with wearables (HR, SpO₂, etc.), enabling timely interventions and fewer hospital visits.

Segments covered

Top 5 FAQs

1) What is the current size and growth outlook?

The market was US$ 2.69B in 2024, US$ 2.88B in 2025, and is projected to reach US$ 5.23B by 2034 at a 6.89% CAGR (2025–2034).

2) Which regions lead and which grow fastest?

North America led revenue in 2024; Asia Pacific is expected to post the fastest CAGR through 2034.

3) Which service types and care models are most important?

Primary care visits led 2024 share; chronic disease management grows fastest. Physician-led house calls led 2024 revenue; telehealth-supported home visits grow fastest.

4) Who pays for house calls today vs. tomorrow?

Private insurance dominated 2024; public insurance/government programs are accelerating via pilots and equity initiatives, driving future growth.

5) Who are notable companies?

Key players include AT HOME DOCTORS, DispatchHealth, Heal, Heally, HealWell24, Home Doctor 24h, House Call Doctor, Housecall Providers, Med2U Inc., MedHouseCall, My Doctor Medical Group, SOS Doctors, Teladoc Health, TruDoc HealthCare, and Visiting Physicians Association.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6214

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest