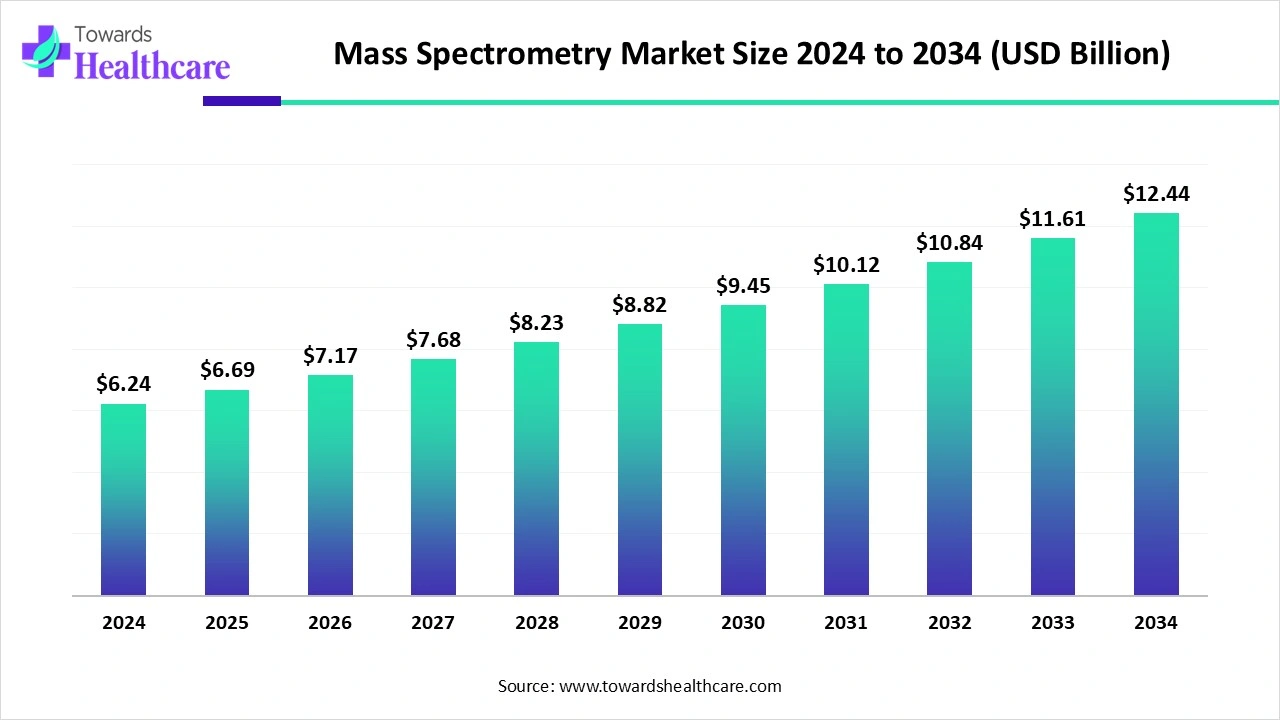

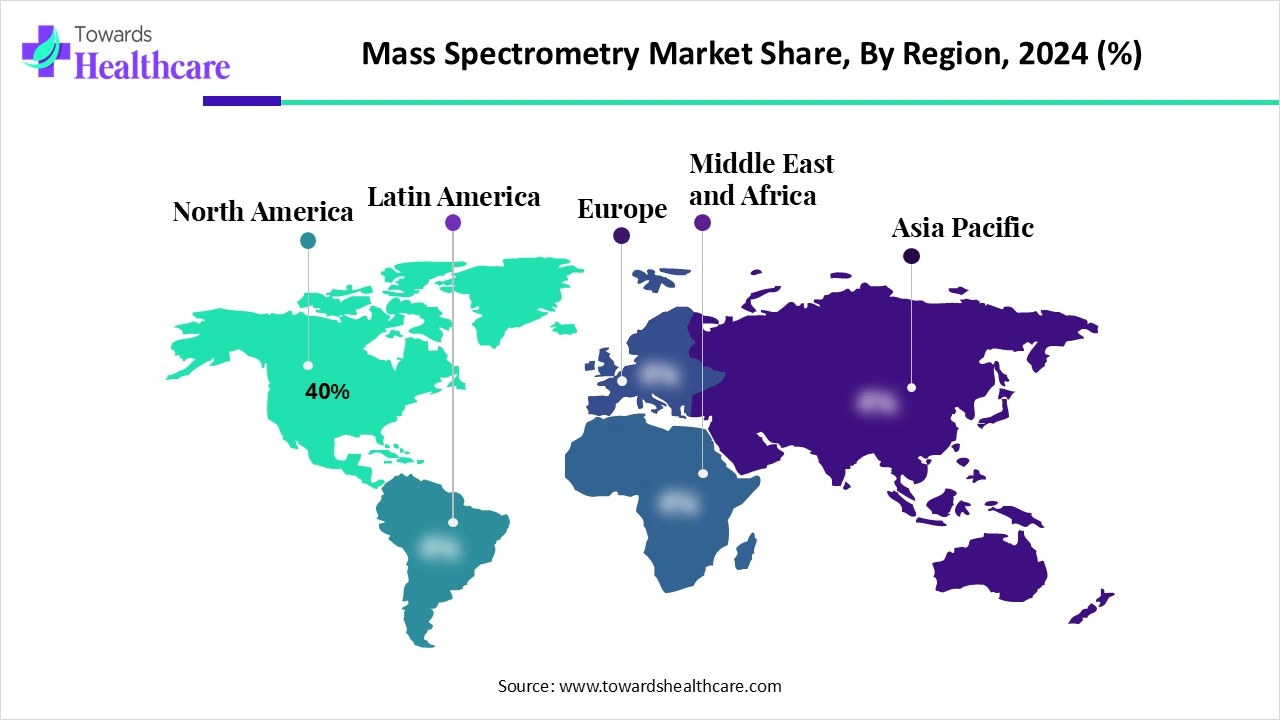

The global mass spectrometry market was US$ 6.24 billion in 2024, is set to reach US$ 6.69 billion in 2025, and is projected to hit US$ 12.44 billion by 2034 at a 7.14% CAGR (2025–2034), with North America holding ~40% share in 2024 and Asia-Pacific poised for the fastest expansion.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6152

Market size

Baseline & runway

➤2024: US$ 6.24 B (market reset year with strong replacement cycle and informatics add-ons).

➤2025: US$ 6.69 B (+US$ 0.45 B YoY), reflecting early impact of miniaturized/benchtop systems.

➤2034: US$ 12.44 B (incremental US$ 6.20 B over 2024).

➤CAGR math anchor (2025–2034): 7.14% implies market doubles in ~10 years, consistent with the 6.69→12.44 trajectory.

By product/instrument type (share anchors, 2024)

➤LC-MS/LC-MS/MS: 38% (largest revenue pool; triple-quad for targeted quant + Orbitrap/TOF for discovery).

➤Benchtop & portable MS: fastest CAGR lane through 2034 (fieldable GC/ambient-ionization units, compact LC-MS).

By ionization/detection tech (share anchors, 2024)

➤ESI: 50% (dominant for large/polar analytes; LC-compatible).

➤Ambient/novel ionization: fastest growth (DESI, DART, ASAP for direct analysis).

By service/deployment (2024)

➤Instrument sales & capital purchases: largest revenue contributor.

➤Software & informatics subscriptions: fastest CAGR (AI/ML pipelines, cloud libraries).

By customer (2024)

➤Pharma & biotech companies: 40% share (largest procurement budgets).

➤Clinical/diagnostic labs: fastest growth into 2034 (lab-developed tests, TDM).

Regional footprint (2024)

➤North America: 40% share (R&D intensity, regulatory demand).

➤Asia-Pacific: fastest expansion (China/India/Japan scale-up).

Market trends

➤Instrumentation advances: Higher sensitivity, dynamic range, and duty cycle; better ion optics and detectors; streamlined workflows showcased at ASMS 2025.

➤Ion-source innovation: Next-gen sources (e.g., optimized ESI/APCI; ambient DESI/DART) reduce sample prep and enable on-surface assays.

➤Miniaturization & portability: Growth of benchtop/portable LC-MS/GC-MS enabling on-site clinical, environmental, and forensic testing.

➤4D separations & ion mobility: TIMS/FAIMS layers add CCS-based identification, improving confidence in metabolomics/lipidomics.

➤Hybrid/high-resolution systems: Expanded use of Orbitrap/TOF for discovery; triple-quads dominate regulated quant.

➤Library & standards expansion: Larger spectral libraries (incl. designer drugs) speed up unknown identification.

➤Software-first workflows: Cloud LIMS, subscription analytics, and automated pipelines shorten time-to-answer.

➤Clinical adoption curve: MALDI-TOF for microbial ID and targeted LC-MS panels scale across hospital labs.

➤Regulatory pull: FDA/EPA/EMA/EFSA expectations drive method robustness, traceability, and data integrity features.

➤Total-workflow integration: Vendors bundle chromatography, MS, consumables, and informatics for end-to-end solutions.

10 AI roles/impacts in mass spectrometry

Peak detection & deconvolution: ML denoises complex spectra, resolves co-eluting peaks, and adapts thresholds to matrix effects, lifting LoDs without hardware changes.

Feature annotation & ID: Graph neural nets and probabilistic matching integrate m/z, isotopic patterns, fragmentation trees, RT/CCS predictions to boost ID confidence.

Spectral library growth via synthesis: Generative models simulate MS/MS spectra for rare/novel compounds, closing coverage gaps and improving search hit rates.

Retention time (RT) & CCS prediction: AI models predict RT/CCS across columns/instruments, enabling orthogonal matching and fewer false positives in untargeted omics.

Quantitation automation: Adaptive calibration, drift correction, and internal-standard optimization reduce analyst time and inter-lab variability in regulated assays.

Outlier & anomaly detection: Real-time QC flags carryover, source fouling, and column degradation; recommender systems suggest maintenance before failure.

Method development acceleration: Bayesian optimization tunes collision energies, dwell times, and gradients to hit sensitivity and throughput targets faster.

Cohort-scale multiomics: Weak-signal extraction across thousands of runs (batch effect correction, missing value imputation) improves biomarker discovery power.

Edge AI for portable MS: On-device inference enables field triage (forensics, food safety) with minimal connectivity; results sync to cloud when available.

Decision support & compliance: AI auto-generates audit trails, validation reports (IQ/OQ/PQ), and assists with 21 CFR Part 11/GxP documentation, reducing compliance burden.

Regional insights

North America (40% in 2024; leadership)

Why dominant: Dense pharma/biotech base, NIH-backed R&D, stringent FDA/EPA standards enforcing high-spec quant.

Where growth comes from: Clinical LC-MS panels, PFAS/environmental testing, and toxicology forensic workloads.

Constraints: Staffing shortages for advanced MS methods and rising total cost of ownership (TCO).

United States (NA core)

Drivers: World-class academia-industry consortia; early uptake of HRMS + ion mobility; hospital networks scaling MALDI-TOF and targeted LC-MS.

Use cases: Impurity profiling, nitrosamines control, PFAS trace analytics, TDM in specialty centers.

Canada (fastest in NA)

Catalysts: Federal/provincial funding for environmental monitoring and life-sciences innovation; expanding bioclusters (Toronto, Vancouver, Montreal).

Focus: Food authenticity, clinical adoption in provincial health labs, and sustainability analytics.

Asia-Pacific (fastest global growth)

China: Capacity build-out across CRO/CMO, environmental surveillance, and food safety; strong public investment.

India: Biopharma R&D scale-up; new experience/innovation centers integrating chromatography-MS-informatics; price-sensitive demand for benchtop and service models.

Japan: Early adopters of high-end HRMS and TIMS in metabolomics/proteomics; quality culture sustains premium segment.

Europe

Strengths: EMA/EFSA frameworks, advanced proteomics hubs; sustainability rules driving non-target screening via HRMS.

Adoption: Broad public lab networks; consistent demand for regulated quant and untargeted screening.

Latin America

Emergence: Food export compliance and environmental mandates; growing private diagnostics.

Barriers: FX volatility and capex cycles slow HRMS penetration; service/outsourcing fills gaps.

Middle East & Africa

Niche demand: Petrochemical/industrial analytics, emerging clinical reference labs in GCC.

Needs: Training, service coverage, and scalable financing (leasing/MS-as-a-service).

Market dynamics

Drivers

Forensics & toxicology adoption: MS sensitivity/specificity for NPS and metabolites; new GC-MS facilities improving casework throughput.

Clinical & personalized medicine: Targeted LC-MS assays and MALDI-TOF speed ID and TAT in hospitals.

Technology push: ASMS-showcased advances (sources, ion optics, detectors) lift performance without sacrificing robustness.

Restraints

Operational complexity: Skilled analysts required; method transfer and validation are time-intensive.

Regulatory burden: Lengthy approvals, extensive documentation; slows clinical menu expansion.

TCO pressures: Capex + service contracts + standards/consumables inflate lifecycle costs.

Opportunities

R&D & public-private hubs: Integrated chromatography-MS-informatics centers (training, regulatory-ready R&D).

Software subscriptions: Fastest-growing revenue stream (AI analytics, cloud libraries, LIMS integration).

Portable MS: Field deployments in environmental, food, and forensics; new usage and buyer personas.

Top 10 companies

Thermo Fisher Scientific

Products: Orbitrap HRMS, triple-quad LC-MS/MS, GC-MS, MALDI, Dionex LC, consumables & cloud informatics.

Overview: Broadest portfolio from sample prep to software; strong clinical and biopharma presence.

Strengths: Orbitrap ecosystem leadership; global service; end-to-end workflow bundling.

Agilent Technologies

Products: LC-MS/Q-TOF, triple-quad LC-MS, GC-MS, OpenLab/LIMS, columns/standards.

Overview: Chromatography-first integration with MS; expanding biopharma application centers.

Strengths: Seamless LC-GC-MS stack; usability; strong installed base in QA/QC.

Waters Corporation

Products: UPLC, TQ/TOF MS (e.g., Xevo), ion mobility options, UNIFI/Informatics.

Overview: Pioneer in UPLC; strong regulated lab footprint.

Strengths: Method robustness, compliance tooling, consumables ecosystem.

SCIEX

Products: Triple-quads, QTOF (ZenoTOF), OptiFlow microflow, Analyst/SCIEX OS.

Overview: Benchmark in quantitative LC-MS/MS for regulated bioanalysis.

Strengths: Sensitivity in TQ; rugged hardware; bioanalytical application depth.

Bruker Corporation

Products: timsTOF/TIMS ion-mobility HRMS, MALDI-TOF/TOF, 4D-omics platforms.

Overview: Leader in ion-mobility HRMS and MALDI; strong metabolomics/proteomics.

Strengths: 4D separations (TIMS+CCS); high-confidence annotation.

Shimadzu Corporation

Products: LC-MS/MS (triple-quads), GC-MS/MS, MALDI, Nexera LC, LabSolutions.

Overview: High value-for-performance and reliability; strong in APAC.

Strengths: Ruggedness, ease of maintenance, competitive TCO.

PerkinElmer

Products: GC-MS/LC-MS solutions, elemental ICP-MS, sample prep & informatics.

Overview: Notable in applied markets (environmental/food) and elemental analysis.

Strengths: Breadth in ICP-MS; government/agency relationships.

JEOL Ltd.

Products: GC-TOFMS/HRMS, MALDI, electron optics heritage.

Overview: Precision Japanese engineering; niche HRMS and imaging ties.

Strengths: High-resolution detection; integration with microscopy workflows.

LECO Corporation

Products: GCxGC-TOFMS, HR-TOFMS for complex mixtures.

Overview: Specialist in comprehensive two-dimensional GC for petro/food/env.

Strengths: Peak capacity; strong deconvolution in complex matrices.

Analytik Jena (Analytik Jena Group)

Products: Elemental/MS solutions, sample prep, automation; ties to life-science instruments.

Overview: Focus on applied/elemental analytics with growing MS footprint.

Strengths: Value-oriented systems; integration with sample handling.

Latest announcements

SCIEX (June 2025): ZenoTOF 8600 announced with up to 10× sensitivity vs. predecessor, enabled by OptiFlow Pro, enhanced DJet/QJet ion guides, and a new optical detector supporting higher ion currents—materially improving low-abundance peptide detection and DDA/DIA coverage.

Bruker (May 2025): timsMetabo launched for 4D-Metabolomics/Lipidomics with TIMS “MoRE” scan-mode; leverages CCS at scale for higher qual-quant confidence and superior small-molecule separation power.

Thermo Fisher (June 2025): Next-gen MS systems and software unveiled at ASMS 2025 (Baltimore), targeting biopharma multi-omics, food safety, and environmental research with step-change analytical performance and workflow automation.

Recent developments

Forensics/toxicology infrastructure: A new GC-MS facility went live in Shillong, India (Aug 2025), enabling precise blood alcohol/poison analysis and boosting regional case throughput.

Spectral libraries: Wiley 2025 Mass Spectra of Designer Drugs added ~1,260 spectra/780 unique compounds, accelerating NPS identification.

R&D capacity building: Agilent Biopharma Experience Centre (Hyderabad, 2025) integrates chromatography, mass spectrometry, and informatics for regulatory-ready R&D, training, and method development.

Segments covered

Product / Instrument Type

LC-MS / LC-MS/MS (dominant 38% 2024)

➤Core use-cases: Regulated quant for ADME/TDM, nitrosamines/impurities, peptide/MAb characterization (HRMS).

➤Performance levers: Sensitivity at low pg–ng/mL, linear dynamic range ≥4–5 orders, fast polarity switching for multiplex panels.

➤Buying drivers: Compliance-ready software, method transfer kits, validated libraries; service SLAs that guarantee uptime in QC.

GC-MS / GC-MS/MS

➤Core use-cases: VOCs/semi-volatiles in environmental and food matrices; petrochemical fingerprinting.

➤Performance levers: Hard EI spectra with rich libraries; triple-quad MRM for residue labs; backflushing and inert flow paths for sticky analytes.

➤Buying drivers: Library coverage, rugged inlets/columns, automation for high-throughput residue screening.

MALDI-TOF / TOF-TOF

➤Core use-cases: Rapid microbial ID from colonies; intact mass confirmation for biotherapeutics.

➤Performance levers: Minutes-level time-to-answer, minimal prep, expanding microbe libraries.

➤Buying drivers: Accreditation support, low consumables cost per ID, easy onboarding for clinical labs.

ICP-MS / ICP-MS/MS

➤Core use-cases: Trace metals in water/food/pharma (elemental impurities), semiconductor ultrapure chemicals.

➤Performance levers: KED/CRC cells to mitigate interferences; ultralow detection limits (ppt).

➤Buying drivers: Method templates for ICH Q3D/USP <232>/<233>, autosamplers, contamination-control accessories.

Ion-mobility-coupled MS (IMS-MS)

➤Core use-cases: Separating isomers/isobars; CCS-anchored IDs in metabolomics/lipidomics and proteoforms.

➤Performance levers: Added 4th dimension (CCS) increases ID confidence and reduces false positives.

➤Buying drivers: CCS libraries, seamless integration with LC-HRMS workflows, DIA compatibility.

Benchtop & portable MS (fastest-growing)

➤Core use-cases: On-site forensics, hazardous materials triage, food fraud screening, plant-floor QA.

➤Performance levers: Battery operation, ambient ionization, edge analytics for instant calls.

➤Buying drivers: Portability/TCO, validated field methods, secure sync to cloud LIMS when online.

Consumables & accessories

➤Core use-cases: Columns, sources, kits, calibration standards to keep methods reproducible.

➤Performance levers: Batch-to-batch consistency, matrix-tolerant chemistries, deactivated hardware.

➤Buying drivers: Vendor loyalty programs, method-matched kits, guaranteed retention time windows.

Software & informatics

➤Core use-cases: Acquisition, peak picking, library search, DIA deconvolution, cloud analytics, LIMS.

➤Performance levers: AI-assisted ID/quant, RT/CCS prediction, automated QC flags, audit-ready logs.

➤Buying drivers: Subscription upgrades, zero-downtime updates, multi-site license management.

Services & outsourced testing

➤Core use-cases: GLP/GMP bioanalysis, method dev/validation, regulated batch release, instrument qualification.

➤Performance levers: Turnaround time, cross-site reproducibility, documentation packs.

➤Buying drivers: Capacity buffering for spikes, cost avoidance on capex, access to niche expertise.

Ionization / Detection Technology

➤ESI (dominant 50% 2024)

➤Strengths: Soft ionization for polar/thermolabile biomolecules; LC compatibility; ideal for proteomics/metabolomics.

➤Limits: Ion suppression in dirty matrices; benefits from cleanup/orthogonal separation.

➤Adoption hooks: Broad assay menus, nano/microflow options to boost sensitivity.

APCI / EI

➤APCI: Better for less-polar analytes; complements ESI in small-molecule panels.

➤EI (GC): Reproducible fragmentation; unmatched library matching for confident IDs.

➤Adoption hooks: Mixed-mode labs leverage both to maximize coverage.

MALDI

➤Strengths: Minimal prep, very high throughput for microbe ID and intact mass.

➤Limits: Less suited to complex small-molecule quant.

➤Adoption hooks: Expanding libraries and quality controls for clinical accreditation.

ICP

➤Strengths: Elemental specificity and ppt-level sensitivity; regulatory compliance driver.

➤Limits: Spectral interferences without CRC/KED.

➤Adoption hooks: Ready-to-run templates for pharmacopeial methods.

Ambient/novel ionization (fastest growth)

➤Strengths: DESI/DART/ASAP enable direct-from-surface, near-real-time screening.

➤Limits: Typically qualitative/semiquant without careful calibration.

➤Adoption hooks: Field ops and at-line QA where speed > exhaustive prep.

Service Type / Deployment Model

Instrument sales & capital purchases (largest 2024)

➤Why chosen: Full method control, data ownership, and predictable availability in QA/QC.

➤What matters: Uptime guarantees, validation toolkits, upgrade paths (source/detector).

Consumables & reagents

➤Why chosen: Locks in method reproducibility and accreditation continuity.

➤What matters: Lot continuity, supply assurance, and cost-per-sample transparency.

Software & informatics subscriptions (fastest)

➤Why chosen: Continuous AI/feature updates, scalable compute, and shared libraries.

What matters: Data integrity (21 CFR Part 11), SSO, audit trails, and API/LIMS hooks.

MS-as-a-Service / CROs

➤Why chosen: Avoid capex; burst capacity for studies and validations.

➤What matters: Turnaround time, regulatory documentation, and IP/data security.

Maintenance, calibration & qualification

➤Why chosen: Keeps systems audit-ready (IQ/OQ/PQ), maximizes uptime.

➤What matters: Preventive maintenance schedules, certified standards, remote diagnostics.

End User / Customer

Pharma & biotech (largest 40% 2024)

➤Workflows: Impurity profiling, release/stability testing, bioanalysis, biologics characterization.

➤Priorities: Data integrity, validated methods, global service coverage.

Clinical & diagnostic labs (fastest growth)

➤Workflows: LDT panels (steroids, vitamins), TDM, infectious disease ID via MALDI-TOF.

➤Priorities: Turnaround time, reimbursement-friendly reporting, middleware integration.

Academic/government institutes

➤Workflows: Method innovation, multi-omics, surveillance (PFAS, pollutants).

➤Priorities: Grant-driven flexibility, open data formats, training support.

Environmental/food & forensics/industrial

➤Workflows: Residue limits, authenticity, NPS/drug screens, process QA.

➤Priorities: Rugged methods, portable options, cost per result, chain-of-custody.

Regions

North America (leader 40% 2024)

➤Growth engines: FDA/EPA compliance, hospital LC-MS panels, PFAS and tox workloads.

➤Challenges: Skilled-operator scarcity; TCO pressure drives interest in automation and subscriptions.

Asia-Pacific (fastest)

➤Growth engines: Pharma/biotech build-out, government programs, vendor partnerships/centers.

➤Focus areas: Cost-effective benchtop units, contract testing, rapid clinical adoption in tier-1 cities.

Europe / LatAm / MEA

➤Europe: Strong EU compliance and non-target HRMS screening; stable upgrade cycles.

➤LatAm: Food/export compliance and private diagnostics rising; FX limits HRMS capex → service models.

➤MEA: Niche petro/industrial testing; GCC clinical reference labs emerging; training and financing key.

Top 5 FAQs (with embedded data)

-

What is the market size today and outlook?

➤2024: US$ 6.24 B → 2025: US$ 6.69 B → 2034: ~US$ 12.44 B, 7.14% CAGR (2025–2034). -

Which region leads, and which grows fastest?

➤North America 40% (2024) leads; Asia-Pacific grows fastest through 2034. -

Which instrument type dominates?

➤LC-MS/LC-MS/MS with 38% (2024); benchtop/portable MS grows fastest. -

Which ionization tech dominates?

➤ESI 50% (2024); ambient/novel ionization posts the fastest growth. -

Where is the quickest demand uptick by customer?

➤Clinical & diagnostic labs (fastest growth) while pharma & biotech remains largest (40% 2024).

Access our exclusive, data-rich dashboard dedicated to the laboratory equipment – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6152

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest