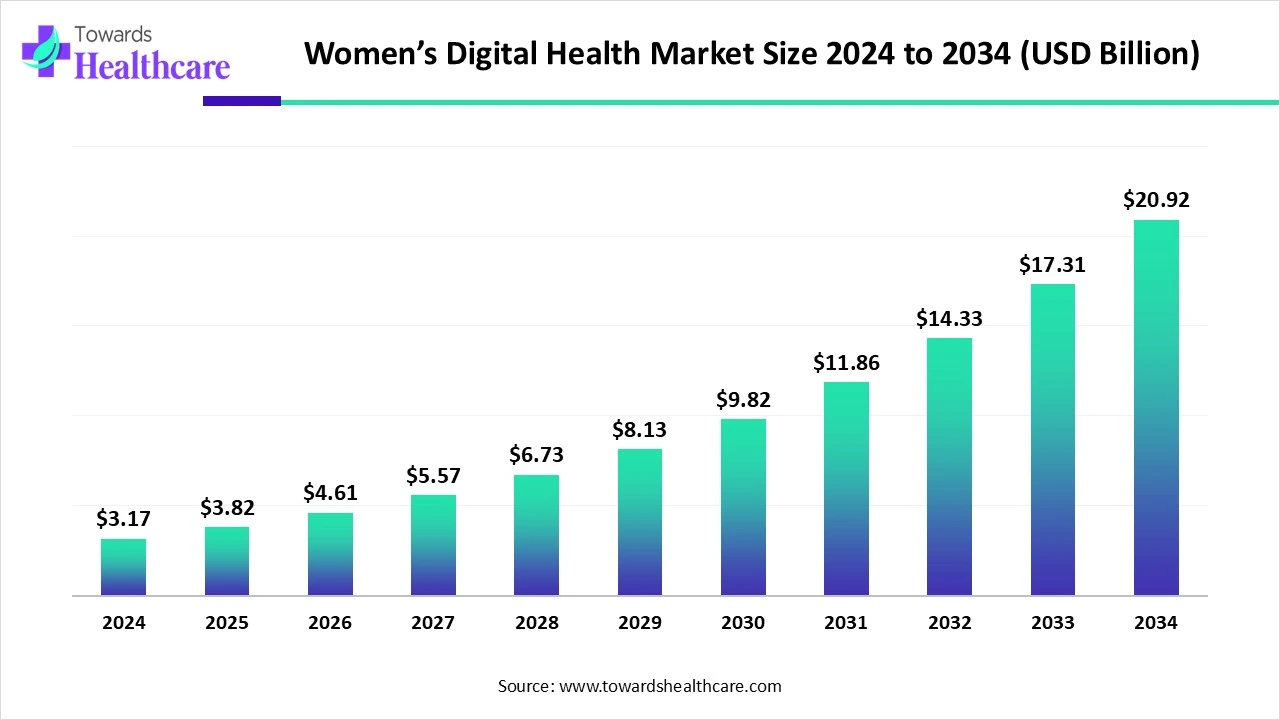

The global womens digital health market was valued at USD 3.17 billion in 2024, rose to USD 3.82 billion in 2025, and is forecast to reach USD 20.92 billion by 2034 (CAGR 20.54% between 2025–2034), driven by mobile apps, wearables, rising investment and expanding adoption across North America, Europe and APAC.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5617

Market Size

Global baseline (2024): USD 3.17 Bn (reported market value in 2024).

Near-term (2025): USD 3.82 Bn (growth versus 2024, reflecting accelerating adoption).

Long-term (2034 forecast): USD 20.92 Bn (projected market value by 2034).

Compound annual growth (2025–2034): 20.54% CAGR (the central growth assumption used in forecasts).

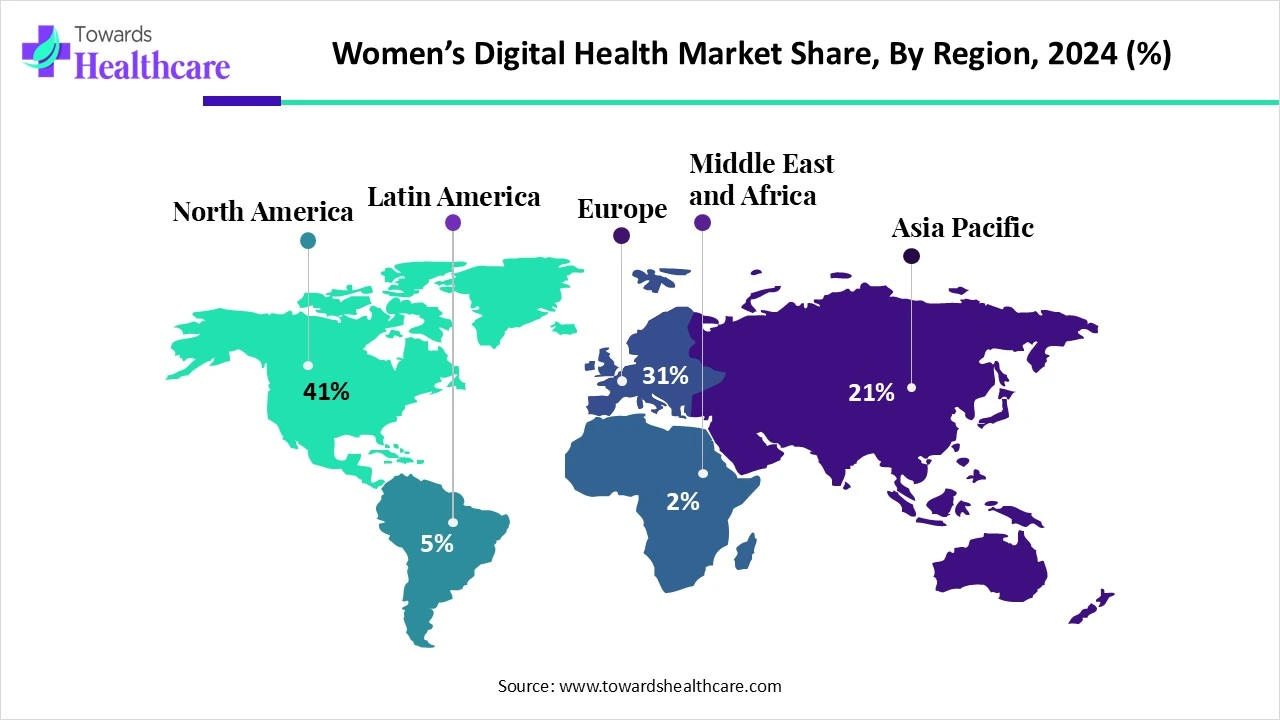

Regional share (2024): North America — 41% of the market (largest regional contributor).

Europe (2024 → 2034): USD 1.03 Bn (2024) → USD 6.69 Bn (2034) at ~20.24% CAGR.

Asia-Pacific (2024 → 2025 → 2034): USD 724.17 M (2024) → USD 889.14 M (2025) → USD 5,691.42 M (2034) (APAC is the fastest growing region; ~22.74% CAGR from 2025–2034).

Segment concentration (2024): by type, mobile apps held the largest share in 2024; wearables are forecast to grow the fastest over the period.

Application leadership (2024): Reproductive health led in 2024; pregnancy & nursing care has the fastest projected CAGR among application groups.

Market Trends

Record VC / investment momentum (2024–2025): Investors poured record capital into women’s health — 2024 saw a notable jump (reportedly $2.6B in one referenced metric and a broader $10.7B figure when including linked disorders), signalling investor confidence and an expanding funding pipeline for femtech startups.

New entrants & platform launches (2025 examples): Startups like Trellis Health emerged (stealth → public) offering networks connecting tens of thousands of practitioners and promising more proactive, personalized women’s care.

AI adoption accelerating product functionality: AI is being integrated to improve detection, decision support, personalization and operational efficiency across platforms (see detailed AI section below).

Wearables move from consumer to clinical-grade: Wearables are evolving from simple trackers to devices aiming for non-invasive monitoring (fertility, glucose, pregnancy metrics) with predictive and real-time recommendations.

Mobile apps remain dominant distribution channel: Apps continue to hold the largest share — convenient, low-friction, and highly scalable for reproductive and prenatal health content, tracking, and teleconsultation.

Regionally differentiated adoption curves: North America leads now due to infrastructure and funding; Europe shows policy-driven digital strategies; APAC shows the fastest uptake because of smartphone penetration and scale.

Maternal & reproductive care digitization: Pregnancy & nursing care and reproductive health are central — digital tools are reducing barriers, offering remote monitoring and remote consultations, and lowering stigma for sensitive issues.

Policy and government programs supporting digital adoption: National digitization strategies (e.g., hospital digital maturity initiatives) and women’s health strategies (investments into maternal/neonatal staff) are enabling market growth.

Data security and privacy concerns shaping adoption: persistent consumer concerns about data breaches and legacy provider reluctance remain a headwind and influence product design and go-to-market tactics.

Market consolidation & corporate participation: With rising funding and higher valuations, expect M&A and strategic partnerships between femtech startups, device makers and established health systems.

AI will (and already is) impacting this market

(Using the report’s framing on AI; deep, pointwise roles and implications.)

Personalized clinical decision support for hormone and reproductive care

AI models synthesize longitudinal menstrual, hormonal, wearable and symptom data to offer individualized care pathways (e.g., tailoring contraceptive choices, flagging abnormal patterns).

Impact: reduces one-size-fits-all recommendations and enables clinician-supported personalization at scale.

Predictive fertility and pregnancy risk modeling

ML algorithms combine cycle, biomarker and wearable signals to predict fertile windows, early pregnancy complications, or preterm birth risk.

Impact: earlier interventions, fewer emergency events, better pregnancy outcomes.

Enhanced screening and detection (imaging + pattern recognition)

AI applied to cervical images, breast ultrasound/mammography metadata, or smartphone-captured images can assist early detection workflows.

Impact: improved triage, faster specialist referral, potential downshift of costs.

Symptom triage and virtual triage bots

AI chatbots pre-screen symptoms, recommend next steps and route patients to telehealth or in-person care based on risk scoring.

Impact: reduces clinician load, improves access and lowers time-to-care.

Operational automation and clinician workflow optimization

NLP and automation reduce administrative burden (charting, summarization, billing prep), letting clinicians spend more time on patient care.

Impact: better clinician retention and capacity.

Multimodal fusion from wearables, apps and labs

AI merges continuous wearable streams, app-reported data and discrete lab results for richer health state estimation (e.g., combining sleep, HRV, temperature and symptom logs).

Impact: more accurate diagnostics and personalized lifestyle interventions.

Bias reduction and inclusive model training (if done responsibly)

When trained on diverse datasets, AI can surface subgroup-specific risk profiles (e.g., by age, ethnicity, BMI), correcting historical under-representation.

Impact: more equitable care — but requires care to avoid perpetuating biases.

Real-time behavior nudges and adherence support

AI-driven micro-interventions (timed reminders, adaptive coaching) to improve medication adherence, prenatal supplement compliance, or lifestyle changes.

Impact: improved outcomes through sustained behavior change.

Clinical trial recruitment and virtual trial management

AI identifies eligible participants from app populations and optimizes decentralized trial workflows (eConsent, remote monitoring).

Impact: faster trials, more representative cohorts, lower trial costs.

Regulatory and privacy-aware ML frameworks

AI systems are being developed with privacy-preserving techniques (federated learning, differential privacy) so models learn without centralizing sensitive data.

Impact: enables model improvement while addressing the key restraint of data security.

Regional insights

North America (dominant; 41% share in 2024)

Market drivers: deep venture capital ecosystem, established digital health infrastructure, high smartphone + broadband penetration, large employer and payer interest.

Clinical integration: health systems and large payer programs pilot femtech integrations; clinical validation is prioritized.

Policy & reimbursement: regulatory clarity and reimbursement pathways (telehealth parity, digital therapeutic reimbursement pilots) accelerate scale.

Strengths: access to capital, large early-adopter populations, strong clinical research networks (e.g., large studies such as WHI referenced).

Challenges: high expectations for clinical evidence, stringent privacy/consent frameworks, and high customer acquisition costs.

Europe (rapidly expanding; example growth to USD 6.69 Bn by 2034)

Policy-led adoption: national digitization strategies and government funding accelerate hospital and maternal care digitization (e.g., DigitalRadar, targeted investments).

Fragmented markets: country-by-country regulation/health system differences mean go-to-market must be localized (language, clinical guidelines, reimbursement).

Trust & public systems: public health systems can enable scaled rollouts if products align with national standards — but procurement cycles are longer.

Strengths: strong regulatory frameworks, high baseline trust in system-level digital health programs.

Asia-Pacific (fastest CAGR 22.74% from 2025–2034)

Scale & mobile-first adoption: smartphone proliferation and rising internet access drive rapid consumer uptake of mobile health solutions.

Affordability & accessibility demand: digital tools reduce access gaps in peri-urban and rural settings — high potential to leapfrog traditional infrastructure.

Local innovation & partnerships: private-public collaborations and NGOs deliver sexual and reproductive health education via digital platforms.

Country highlights: China — increasing use of digital sexual health education among youth; India — conferences and policy forums (e.g., “WHI 2025”) catalyzing stakeholder collaboration.

Challenges: variations in regulation, payment ability, digital literacy, and data protection laws across countries.

Latin America, MEA (emerging opportunities)

Drivers: unmet needs in maternal/reproductive care, increasing NGO and donor programs, growing local startups.

Barriers: infrastructure, affordability and regulatory maturity vary; however, targeted solutions (SMS, low-bandwidth apps) can scale quickly.

Market dynamics

Driver — Rising awareness among women

Explanation: Educational campaigns, media coverage and NGO initiatives (e.g., breast cancer awareness month) are expanding knowledge of maternal, reproductive and chronic female-specific conditions. This increases demand for accessible digital tools — reflected in the jump from USD 3.17 Bn (2024) to USD 3.82 Bn (2025).

Restraint — Data security & privacy concerns

Explanation: Concerns about breaches and misuse of highly personal reproductive and sexual health data reduce adoption intent and can stall product uptake. Legacy provider mindsets and brand reputation damage after breaches are cited as material headwinds.

Opportunity — Rising investments & commercialization activity

Explanation: Fresh funding rounds, record VC capital and strategic public grants enable startups to scale, validate products, and lower unit prices—broadening market reach. The cited surge in investment (large sector-wide totals in 2024) fuels product innovation and commercialization.

Structural drivers & enablers

Technology maturation (AI, wearables): enabling new device-grade features and predictive capabilities.

Government & policy support: national digital strategies and dedicated women’s health programs (e.g., UK Women’s Health Strategy investments, Germany’s DigitalRadar targets).

Consumer behavior changes: growing comfort with telehealth, self-monitoring, and app-based guidance.

Structural restraints

Clinical evidence requirements: payers and providers demand well-validated clinical outcomes, which slows commercialization for early-stage entrants.

Heterogeneous regulation: multi-jurisdictional compliance increases cost/time to scale internationally.

Top 10 companies

HeraMED

Product: Clinical-grade remote maternal/obstetrics monitoring solutions (home-use devices + platform).

Overview: Focuses on remote monitoring to enable prenatal care at home.

Strengths: Device + platform integration, focus on maternal monitoring, potential to reduce in-clinic visits.

iSono Health

Product: Handheld ultrasound / imaging solutions for point-of-care female health screening.

Overview: Works on portable imaging to expand screening outside hospitals.

Strengths: Portability, enabling early detection in low-resource settings.

Clue (by BioWink)

Product: Menstrual cycle and reproductive health tracking app.

Overview: Consumer-facing app for cycle tracking, fertility insights and symptom logging.

Strengths: Large user base, strong data signals for cycle intelligence and research partnerships.

Chiaro Technology Ltd.

Product: (Femtech diagnostics / software tools) — platform-oriented approaches for women’s health monitoring.

Overview: Focused on creating clinically relevant digital tools for women.

Strengths: Niche product focus, potential clinical partnerships.

Natural Cycles

Product: FDA-marked fertility awareness app used for contraception and family planning.

Overview: Algorithm-based fertility and contraception alternative.

Strengths: Evidence-based positioning, regulatory approvals in some markets.

Ava Science, Inc.

Product: Wearable fertility sensor (wristband) + app to detect fertile windows.

Overview: Combines physiological signals for fertility prediction.

Strengths: Wearable + algorithmic fusion, consumer convenience.

NURX Inc.

Product: Telehealth services for reproductive health (e.g., contraception, STI care).

Overview: On-demand prescriptions and telemedicine for sexual and reproductive health.

Strengths: Convenience, tele-prescription integration, strong consumer access model.

Prima-Temp, Inc.

Product: Fertility/temperature-based tracking products and platforms.

Overview: Focus on basal body temperature and cycle analytics.

Strengths: Simple, clinical signal-based product; good for specific user segments.

Glow

Product: Fertility and pregnancy tracking app with community and coaching features.

Overview: End-to-end reproductive consumer platform (tracking, community, care coordination).

Strengths: Holistic user journey support, community/education features.

MobileODT Ltd.

Product: Mobile devices and imaging platforms for cervical screening (visual inspection + telemedicine).

Overview: Tools aimed at early detection of cervical disease in low-resource settings.

Strengths: Low-cost diagnostics, enabling screening scale in under-served regions.

Latest announcements

Melinda French Gates pledge (October 2024)

Announcement: Melinda French Gates committed an additional $1 billion over two years to women’s empowerment initiatives. Part of this commitment is a $250 million global open call called “Action for Women’s Health.”

Implication: This large philanthropic commitment is expected to catalyze funding, partnerships and scaling opportunities for women’s health innovators — increasing grant and non-dilutive capital available to femtech ventures and programs that target underserved populations.

Expected downstream effects: more pilots, evidence generation projects, and public-private initiatives that can de-risk markets for investors.

Allara Health Series B round (Jan 2025)

Announcement: Allara Health raised $38.5 million (after prior $26M Series B), to expand its virtual women’s healthcare platform focused on hormonal health in the U.S.

Implication: Significant growth capital supports platform scaling, clinician network expansion and product development for hormone-related care, reflecting investor appetite for chronic and hormonal care solutions.

Arva Health pre-seed (Mar 2025)

Announcement: Arva Health raised $1 million in pre-seed to lower costs, increase access and reduce stigma around reproductive healthcare in India.

Implication: Seed-stage funding for region-specific players shows investor interest in APAC-localized solutions and the potential for low-cost, high-impact reproductive health services.

Trellis Health emergence (Apr 2025)

Announcement: Trellis Health launched publicly from stealth — a digital platform connecting women to a network of >50,000 healthcare practitioners nationally (per the content).

Implication: Large practitioner networks indicate a strategy to solve access and care coordination; such platforms can rapidly increase patient reach and referral opportunities.

Sector VC trends (2024–2025)

Announcement/Trend: 2024 recorded an acceleration in venture investments into women’s health — figures referenced include $2.6B and a broader $10.7B accounting for linked disorders — signaling historically high funding levels.

Implication: Amplified capital flows will sustain product innovation, trials, marketing and M&A activity.

Recent developments

Surge in sector funding (2024–2025)

What happened: 2024 marked a funding high point for women’s health, with large totals cited and 2025 continuing momentum via substantial Series and pre-seed rounds.

Why it matters: Capital unlocks R&D, regulatory studies, clinical validation, and go-to-market scale. Well-funded startups can hire clinical teams, collect real-world evidence, and pursue partnerships with payers and health systems.

New platform entrants connecting care networks (Trellis Health)

What happened: Platforms connecting large numbers of practitioners surfaced; these act as aggregator/marketplace models for women’s care.

Why it matters: Aggregated practitioner networks reduce fragmentation and can accelerate virtual care adoption, create standardized care pathways and enable data collection at scale.

Regional funding for India & APAC (Arva Health)

What happened: Localized funding supports region-specific reproductive health solutions, addressing cultural, affordability and access barriers.

Why it matters: Local startups can adapt UX, language, payment models and device choices for regional needs — increasing real adoption versus one-size-fits-all western products.

Clinical-scale rollouts & product expansions (Allara Health)

What happened: Established telehealth players raised substantial rounds to scale hormonal care platforms.

Why it matters: Scaling validated telehealth models helps move digital care from pilots to reimbursable services and long-term chronic care models.

Philanthropic catalytic funding (Melinda French Gates)

What happened: Large philanthropic commitments target systemic barriers and provide de-risking grants for scalable innovations.

Why it matters: Grants allow startups to pursue high-impact projects that are not immediately revenue-generating (e.g., rural pilots), helping evidence generation.

Segments covered

By Type — (what the technology is)

Mobile Apps

What: Smartphone apps for cycle tracking, pregnancy education, teleconsultation, symptom logging and self-triage.

Role: Primary distribution channel and data capture point; lowest friction for users; dominant share in 2024.

Wearable Devices

What: Wristbands, patches, rings and other biosensors measuring temperature, heart rate variability, sleep and other biomarkers.

Role: Fastest growth segment — provides continuous objective signals that can feed AI models and predictive care.

Diagnostic Tools

What: Portable imaging, point-of-care tests, at-home diagnostics and device-assisted screening (e.g., for cervical or breast screening).

Role: Moves digital health into clinical-grade diagnostics; enables prevention and early detection outside traditional clinics.

Others

What: Telehealth platforms, remote monitoring platforms, analytics dashboards, clinical decision support, enterprise solutions for health systems.

Role: Back-end infrastructure enabling scale, clinician workflows, and data interoperability.

By Application — (what problem is being solved)

Reproductive Health

Subpoints: Fertility tracking, contraception alternatives, menstrual health, STI management.

Role: The largest application in 2024 — high demand for accessible, stigma-reducing tools.

Pregnancy & Nursing Care

Subpoints: Prenatal monitoring, tele-OB visits, lactation support, postpartum mental health.

Role: Fastest CAGR — digital prenatal & postnatal care reduce clinic burdens and improve outcomes.

Pelvic Care

Subpoints: Pelvic pain management, pelvic floor therapy, incontinence monitoring.

Role: Growing visibility and consumer willingness to seek solutions.

General Healthcare & Wellness

Subpoints: Chronic disease management (e.g., osteoporosis), mental health, nutrition, lifestyle coaching.

Role: Expands TAM (total addressable market) by pairing general wellness with women-specific health contexts.

By Region — (where services are deployed)

North America / Europe / Asia-Pacific / Latin America / MEA — each region contains country-level markets with distinct regulatory, payer and cultural landscapes. APAC shows the fastest growth; North America the largest share as of 2024.

Top 5 FAQs

Q — What is the current size and growth trajectory of the women’s digital health market?

A — The market was USD 3.17 Bn in 2024, grew to USD 3.82 Bn in 2025, and is forecast to reach ~USD 20.92 Bn by 2034, implying a 20.54% CAGR between 2025–2034.

Q — Which region leads the market and which is growing fastest?

A — North America led the market in 2024 with ~41% share. Asia-Pacific is the fastest-growing region (APAC projected to grow from USD 724.17 M in 2024 to USD 5,691.42 M by 2034 at ~22.74% CAGR).

Q — Which product types and applications are most important today?

A — Mobile apps held the largest share in 2024, while wearable devices are projected to grow the fastest. By application, reproductive health led in 2024; pregnancy & nursing care is projected for the fastest CAGR.

Q — What are the key barriers to adoption?

A — Data security and privacy concerns are the principal restraint — fears around data breaches and misuse can slow adoption. Clinical evidence requirements and fragmented regulation across regions are additional barriers.

Q — What is driving investor interest in the sector?

A — Rising awareness of women’s health needs, demonstrable market demand, government and philanthropic support (e.g., large grants), and a record level of venture funding in 2024 (with large capital flows continuing into 2025) are catalyzing investment.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5617

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest