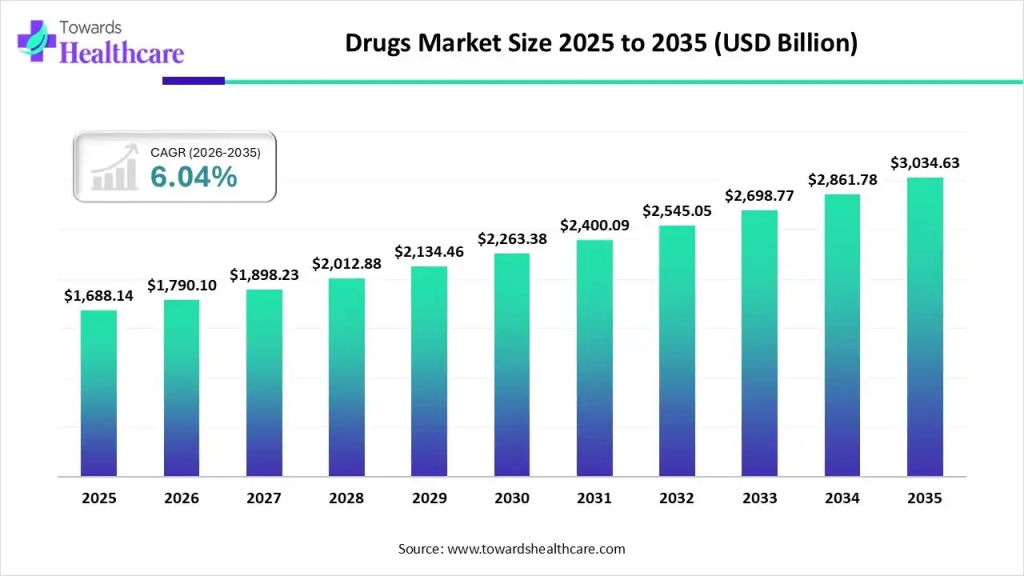

The global drugs market is entering a new growth cycle, supported by rising chronic disease prevalence, an aging population, expanding biologics adoption, and continuous innovation in oncology, immunology, metabolic disorders, and rare diseases. The market is projected to grow from USD 1,790.05 billion in 2026 to USD 3,034.63 billion by 2035, registering a CAGR of 6.04%.

The pharmaceutical industry is also witnessing unprecedented investments in GLP-1 therapies, antibody-drug conjugates (ADCs), gene therapies, biosimilars, and AI-enabled drug discovery. Pharmaceutical manufacturers continue expanding manufacturing facilities, licensing innovative molecules, and strengthening global supply chains to address increasing healthcare demand.

Looking for data that supports your next business decision? Get a FREE sample tailored to your strategic priorities: https://www.towardshealthcare.com/download-sample/5713

North America Dominates While Asia Pacific Emerges as the Fastest Growing Market

North America remained the largest regional market in 2025, accounting for an estimated 42-45% of global pharmaceutical revenue due to its advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement systems, and strong presence of multinational drug manufacturers.

Europe represented approximately 23-25% of global market revenue, supported by robust pharmaceutical R&D, biosimilar adoption, and government-backed healthcare programs.

Asia Pacific contributed nearly 22-24% of global sales and is forecast to record the fastest CAGR through 2035. China and India continue expanding pharmaceutical manufacturing capacity, while Japan and South Korea remain leaders in innovative drug development.

Latin America and the Middle East & Africa together account for approximately 10-12% of global pharmaceutical demand, driven by increasing healthcare investments and greater access to generic medicines.

Prescription Medicines Continue to Generate the Largest Revenue

Prescription medicines accounted for 60% of the global drugs market in 2025, while over-the-counter (OTC) medicines represented 40%.

Among therapeutic segments:

- Oncology remained the largest therapeutic area with an estimated 18-20% market share, driven by rising global cancer incidence and continued demand for immunotherapies and targeted treatments.

- Cardiovascular therapies contributed approximately 14-16% of pharmaceutical revenues.

- Diabetes therapies accounted for nearly 10-12%, supported by expanding GLP-1 adoption.

- Immunology is expected to register the fastest growth during the forecast period owing to increasing biologic approvals for autoimmune diseases.

Drug-type analysis shows:

- Branded drugs: 40%

- Specialty drugs: 30%

- Generic drugs: 10%

- Small molecule drugs: 10%

- Biologics: 5%

- Biosimilars: 5%

Oral medicines continued to dominate administration routes, while injectable formulations are projected to experience the fastest growth due to increasing biologics, monoclonal antibodies, cell therapies, and GLP-1 products.

Retail pharmacies remained the leading distribution channel, whereas online pharmacies continue recording the highest growth because of digital healthcare adoption and expanding telemedicine.

Leading Pharmaceutical Companies Continue Multi-Billion Dollar Growth

The competitive landscape remains highly consolidated, with the world’s largest pharmaceutical companies investing aggressively in innovative therapies.

According to recent industry rankings:

- Johnson & Johnson generated approximately USD 88.8 billion in pharmaceutical revenue.

- Roche reported approximately USD 65.3 billion.

- Merck & Co. generated approximately USD 64.2 billion, largely supported by Keytruda.

- Pfizer reported USD 63.6 billion.

- AbbVie generated USD 56.3 billion.

- AstraZeneca reached approximately USD 54.1 billion.

- Novartis generated approximately USD 50.3 billion.

- Novo Nordisk reported approximately USD 42.1 billion, driven primarily by GLP-1 therapies.

Collectively, the top ten pharmaceutical manufacturers account for well over 45% of global innovative drug revenues, highlighting the industry’s strong market concentration.

Blockbuster Drugs Continue Driving Global Pharmaceutical Sales

The world’s highest-selling medicines continue reshaping therapeutic priorities.

Leading products include:

- Keytruda (Merck) generated approximately USD 30 billion in 2024 sales, remaining the world’s best-selling prescription medicine.

- Eli Lilly’s Mounjaro and Zepbound together generated approximately USD 36.5 billion in 2025, making tirzepatide one of the fastest-growing drug franchises globally.

- Novo Nordisk’s Ozempic, Wegovy, and Rybelsus collectively delivered over USD 36 billion in annual sales, reflecting continued demand for obesity and diabetes therapies.

- Other blockbuster medicines include Dupixent, Skyrizi, Darzalex, Eliquis, Biktarvy, Ocrevus, and Gardasil, each generating multi-billion-dollar annual revenues.

Checkout the Market Report Now at: https://www.towardshealthcare.com/checkout/5713

Recent Industry Developments Strengthen Long-Term Market Outlook

Major pharmaceutical companies continue expanding through acquisitions, licensing agreements, manufacturing investments, and new product launches.

Recent developments include:

- AstraZeneca signed a USD 1.5 billion licensing agreement with China’s Dizal Pharmaceutical for the lung cancer therapy Zegfrovy, strengthening its oncology portfolio.

- Johnson & Johnson reported pharmaceutical sales exceeding USD 16 billion in a single quarter, with psoriasis therapy Tremfya growing nearly 73% year-over-year, highlighting strong demand for immunology medicines.

- Sun Pharma received regulatory approval in South Africa for a generic version of semaglutide, expanding affordable GLP-1 access beyond India.

- Regulatory agencies and pharmaceutical companies continue integrating artificial intelligence into drug discovery, clinical trial optimization, and regulatory review, significantly reducing development timelines and improving R&D productivity.

With oncology, GLP-1 therapies, immunology, biologics, precision medicine, and AI-driven drug development becoming core growth pillars, the global drugs market is expected to remain one of the fastest-growing and highest-value sectors within the healthcare industry over the coming decade.

Access our exclusive, data-rich dashboard dedicated to the therapeutics area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

About Us

Healthcare WebWire is a part of Towards Healthcare Research and Consulting delivers strategic intelligence and market expertise for the global drugs market. We work with pharmaceutical companies, manufacturers, and healthcare stakeholders to analyze industry trends, competitive landscapes, and evolving treatment demands. Our insights help businesses strengthen product development, identify growth opportunities, and adapt to the rapidly changing pharmaceutical environment.

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium